In your 40s but find yourself with barely any retirement savings? Unsure if you can even afford to retire comfortably after paying off your mortgage, funding your children’s education and caring for your aged parents? You’re not alone. According to the recent Syfe Retirement Readiness Index (SRRI), respondents aged 45 to 54 are the least prepared for retirement, with a median SRRI score of 72 (scores below 100 indicate low levels of retirement readiness).

Your future retirement may seem bleak but here’s how to bring the sparkle back to your golden years.

Know your numbers

Imagine you’re currently retired – what expenses are you likely to have? What sort of lifestyle do you envision?

A study by the Lee Kuan Yew School of Public Policy found that a single elderly person living alone would need at least $1,379 each month just to meet basic needs. Depending on how you want your retirement to look like, this figure may or may not be enough to cover your personal retirement expenses.

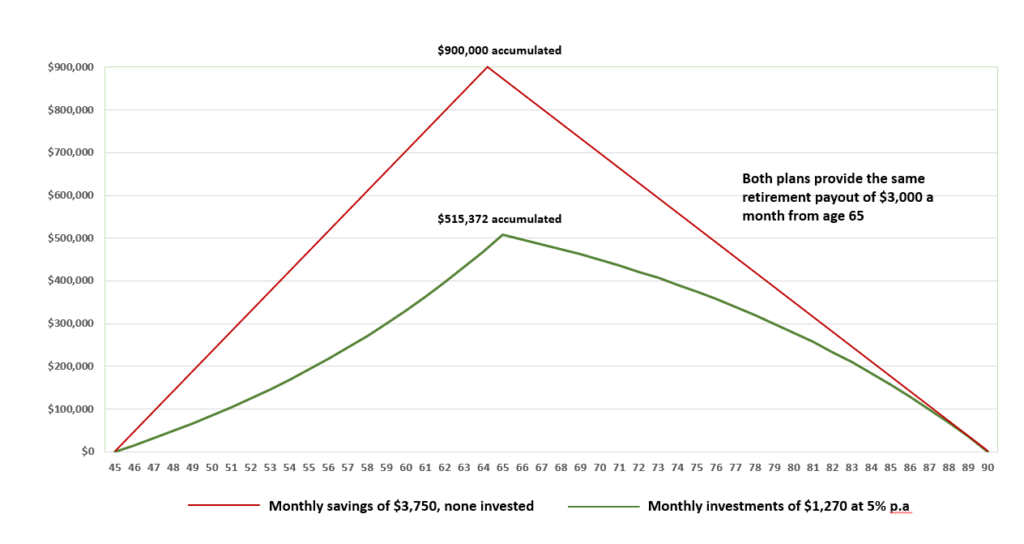

Let’s assume you’re 45 years old and plan to retire at 65. You decide that you want a comfortable retirement with income of $3,000 per month, a reasonable figure given rising medical costs and living expenses. Considering that life expectancy in Singapore is now 84.8 years, you wish to ensure that your retirement nest egg can last you for 25 years so you don’t outlive your savings.

To simplify the example, let’s ignore the effects of inflation and the monthly CPF LIFE payouts you’ll receive from age 65 onwards (CPF payouts for those who meet the Basic Retirement Sum in their CPF Retirement Account currently range from $730 to $790). To achieve your goal of having monthly retirement income of $3,000 for 25 years, you will need a nest egg of $900,000 by the time you retire.

Tip: Check out our financial planning calculators to help you determine the amount you need to retire, calculate how much you need to invest, and see if you're on track to meet your financial goals.

The magic of compound interest

With just 20 years to save $900,000, you need to set aside $3,750 each month if you’re keeping that money in a basic savings account. But if you leverage the compounding returns from investing, the monthly amount you need to put away decreases.

In fact, you only need to invest $1,270 monthly, and stay invested during retirement. This means that you’ll contribute $1,270 every month to your investment account, and at age 65, keep your accumulated savings of $515,372 invested instead of withdrawing all of it. While you will no longer be contributing to your nest egg during your retirement years, your money is still growing thanks to compound interest. This allows your retirement fund to sustain a monthly draw-down of $3,000 for 25 years.

This example assumes that your funds will be invested at an average return rate of 5%. A 5% return is fairly conservative and realistic. For comparison, money in the CPF Special Account currently earns 4% per annum.

Consistent, long-term investing is an effective strategy to accumulate wealth. And the earlier you start investing, the more you benefit from compound interest. If you wait till you’re 48 years old to start investing, you need to invest about $1,625 at a 5% return just to achieve the same $515,372 necessary.

Invest better with ETFs

Now that you know how investing can help bridge your retirement savings gap, it’s time to figure out how and what to invest in.

One of the proven ways to build wealth without excessive effort and cost is through passive investing, a strategy that seeks to minimise investment fees while growing wealth steadily over the long term. Instead of trying to pick the “best” stocks or timing the market, you simply buy a fund that mimics the return of a certain benchmark index like the Standard & Poor’s 500 index (S&P 500). You earn similar returns to what the benchmark does, all while paying lower fees.

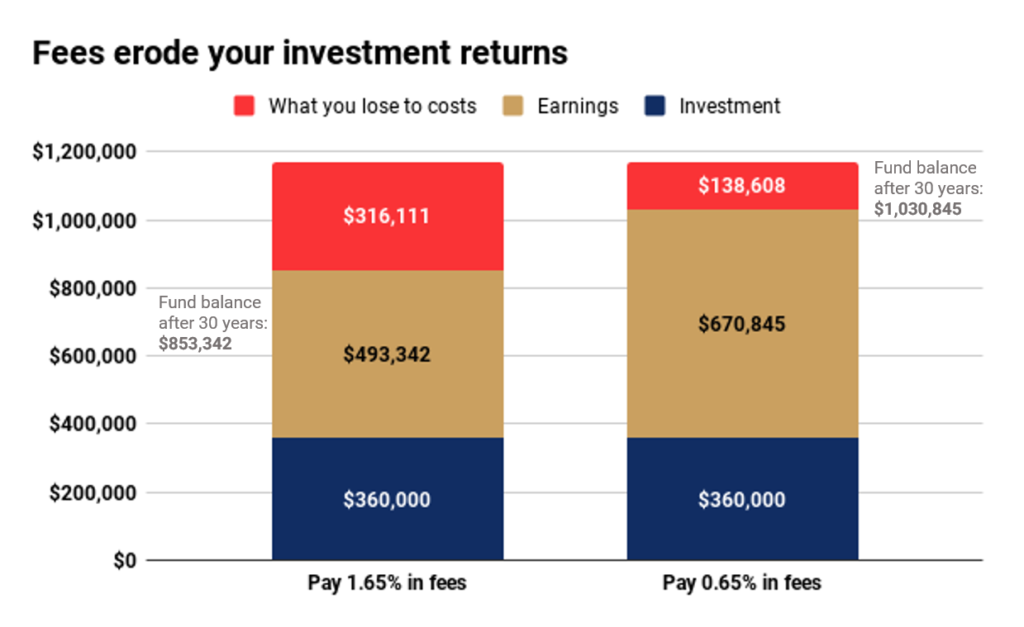

Investing in exchange-traded funds (ETFs) is one way of implementing a passive investing strategy. Firstly, ETF fees are significantly lower and more transparent than what actively managed investments like unit trusts charge. High fees can sink your retirement savings. That’s because fees get compounded along with your investment returns. Paying 2% or 3% in fees may not seem like much initially, but you are losing all the growth that money might have had for years into the future.

ETFs also help investors reduce single stock risks. An investor with only a few thousand dollars to invest will probably only purchase one stock, after accounting for transaction and brokerage costs. If the company runs into any issues, the stock price might get affected, and the investor’s portfolio will be at risk.

An ETF however holds many different stocks in one portfolio. This means that you are still investing in tens or even hundreds of different stocks when you buy an ETF, even if your investment is a small amount.

Determining your asset allocation

ETFs offer exposure to a wide variety of asset classes. You can invest in stocks, bonds, commodities, real estate and more through ETFs. Each asset class offers different risk-return characteristics, so ensure that your risks are spread by investing in a diversified portfolio covering multiple asset classes, sectors and geographies.

Another rule of thumb to remember is that the closer you get to leaving the workforce, the more conservative your investments should be. If most of your money is invested in stocks and the stock market crashes a few years before you are due to retire, your portfolio may not have time to sufficiently recover. This doesn’t mean you should avoid stocks entirely. Rather, figure out your ideal portfolio allocation – the proportion of stocks, bonds, and other assets your portfolio should consist of.

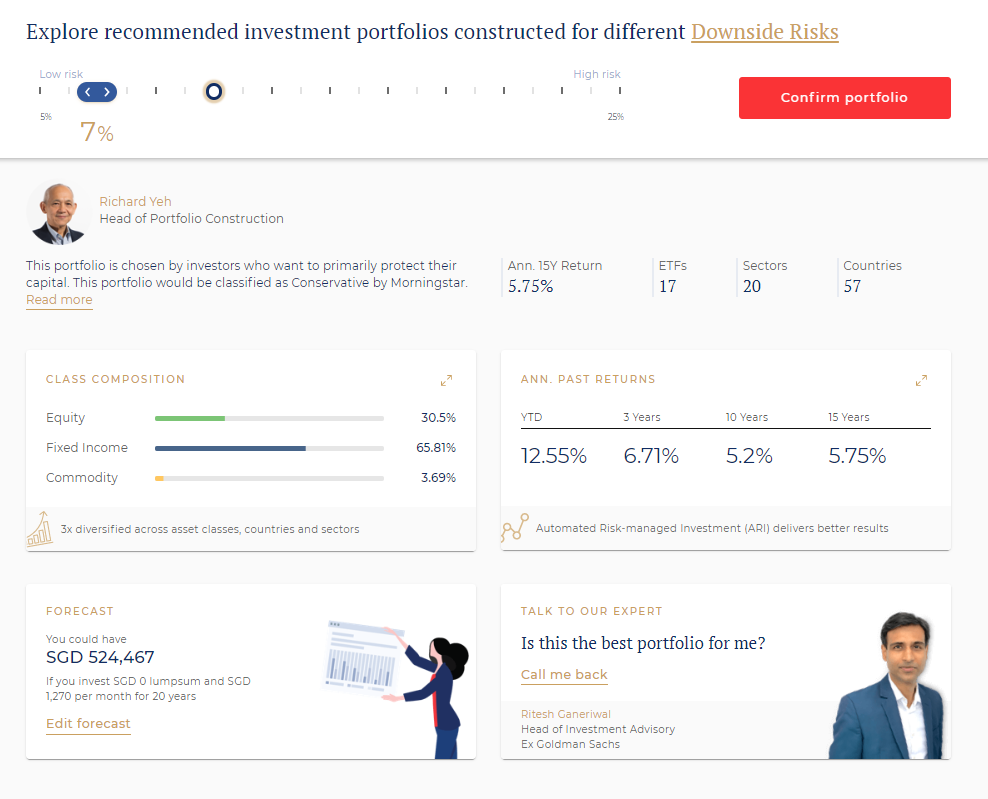

You can use Syfe’s risk assessment tool to find out what asset allocation best suits your risk profile, target retirement savings, and time horizon. For instance, a portfolio consisting of 30.5% stocks, 65.81% bonds and 3.69% commodities is what the risk assessment tool may recommend for an investor aiming to have about $515,372 in 20 years.

Making the numbers work

At this point, you’re probably wondering if you can afford to invest $1,270 each month to reach your retirement savings target. If you have paid off most loans except for your mortgage and have at least three months’ salary set aside as your emergency fund, then yes, you can and should start investing for retirement.

Financial experts usually recommend setting aside at least 20% of your salary for your financial goals. But there’s no reason why your salary should restrict you from reaching your retirement goals. It’s worth noting that making lifestyle choices that avoid major or unnecessary expenses is one of the most effective ways of saving more in the first place.

Examples include taking public transport instead of owning a car, having more meals at home instead of dining out, and spending only on items you need instead of want.

Don’t Delay Any Further

You may think that building a comfortable retirement nest egg is out of reach without any prior savings. But the truth is you still have 20 years to save and invest for your retirement.

Your 40s are also your peak earning years. Unlearn, relearn and upskill to enhance your earnings potential. Spend consciously and consider setting a budget to help you set your spending priorities each month. Start investing – it doesn’t have to be complex. You can start investing in Singapore with Syfe’s fully managed portfolios with MyInfo in just 3 minutes.

A good and comfortable retirement is still possible – if you start now. To find out where you currently stand on the Syfe Retirement Readiness spectrum, check your score here.

You must be logged in to post a comment.