Find out what’s behind the drop, where rates are headed, and smarter ways to earn higher income.

The 5 June 2025 T-bill auction closed with a cut-off yield of just 2.05%. That is not only a step down from the 2.20% achieved two weeks earlier, but also the lowest level recorded so far in 2025 and the sixth straight auction where yields have declined.

Source: MAS, as of 5 June 2025

What’s Driving the Slide in T-Bill Rates?

1. Persistent SGD Liquidity

The domestic banking system remains flush with Singapore-dollar deposits, keeping short-term funding costs subdued. The demand for high-rated papers like Singapore Government Securities (SGS) bonds is strong, compressing yields in spite of global macro uncertainty.

2. Global Policy Expectations

Even though the US Federal Reserve has held its policy rate steady all year, markets are pricing eventual cuts. Analysts expect the Fed to keep rates unchanged in June but are ready to ease later in 2025 if US data weakens. Anticipation of easing US policy is capping SGD yields, given the close link between Singapore and US money-market curves.

3. Portfolio Rebalancing Into Safe Assets

After a volatile first half for equities and credit, institutional investors have rotated toward shorter-duration, high-quality instruments. The increased demand for SGD fixed-income products is spilling over onto MAS bills, lowering cut-off yields even as the supply of government securities gradually rises.

4. Supply Dynamics

Even though the government can now issue more bonds, supply is being rolled out gradually. With each 6-month T-bill auction still capped around S$7.5 billion, yields remain low—not necessarily because demand is surging, but due to limited supply. Yield-seeking investors might thus look for alternatives to T-bills.

Outlook: Will Yields Rebound or Stay Low?

The outlook hinges on two-way risks:

- Fed timing. MAS bills usually follow US interest rate trends, but with a delay. If US jobs or inflation pick up, Fed rate cuts may be delayed, and T-bill yields could rise above the current rate. But if US data weakens, the Fed may cut rates by 50 to 75 basis points later this year, keeping Singapore rates below 2%.

- Domestic liquidity trends. Strong exports and weak loan demand have kept Singapore’s financial system abundant in cash. Unless there’s a sharp rise in borrowing or major currency intervention, overnight SORA is unlikely to spike.

- Government supply. Even though the government can issue more bonds, MAS is taking a cautious approach to doing so. A sudden increase in supply could nudge yields higher, but policy makers typically front-load issuance when demand is strong to keep markets stable.

Most strategists expect six-month T-bills to hover around 2.0–2.3% through the third quarter, with rallies capped by policy uncertainty and dips supported by cash-rich investors hunting for quality yield.

Alternatives to T-Bills

For investors discouraged by the falling yields on T-bills, there are several compelling alternatives that offer not just higher returns but also greater flexibility and accessibility.

Cash+ Flexi: Higher returns without locking up funds

Syfe Cash+ Flexi currently delivers projected returns of 2.9% p.a. with no lock-in period, making it a compelling option for those seeking liquidity and safety. Built with high-quality, short-duration fixed income assets, Cash+ Flexi allows you to withdraw your money anytime without penalties—unlike T-bills, which lock in your funds for six months.

This makes Cash+ Flexi a practical choice for both emergency savings and idle cash that you want to keep working for you.

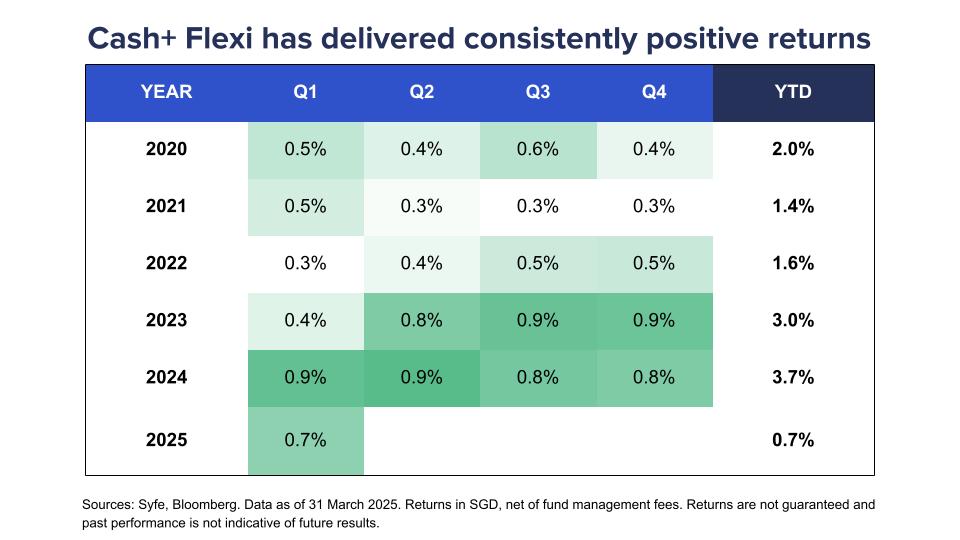

The portfolio has been delivering consistently positive returns over the years.

Earn Attractive Bond Income with Syfe Income+

For those with a slightly higher risk appetite, Syfe Income+ offers even more attractive income potential, with monthly payouts targeting 5–6% p.a. and the benefit of global diversification across bonds and credit instruments.

The actively managed portfolio focuses on high-quality global bonds—including government, investment-grade corporate, and securitised exposures—aiming to deliver consistent income with lower volatility than traditional bond funds.

While not capital-guaranteed, it provides professional management by PIMCO and can serve as a core income-generating component in a portfolio. These alternatives allow investors to diversify beyond T-bills while optimising yield, liquidity, and risk based on their financial goals.

- Target yield: 5–6% p.a. (paid monthly)

- Professional oversight: Curated by PIMCO, one of the world’s largest fixed-income managers

- Flexibility: No lock-in period; withdraw anytime without penalties

- Diversification: Spread across sectors, geographies, and maturities, reducing single-issuance risk

While six-month T-bills at 2.05% remain a safe parking spot for excess cash, Syfe Income+ offers the potential to more than double that yield. Plus, it pays you every month instead of twice a year. In a market climate where rates shift quickly, an actively managed, globally diversified bond solution can help you stay ahead.

T-Bills vs Cash+ Flexi vs Income+ At A Glance

| Feature | T-Bills | Cash+ Flexi | Income+ |

| Interest Rate / Payout | 2.05% | 2.90% | 5.0–6.0% |

| Payout Frequency | At maturity | N/A | Monthly |

| Minimum Investment | S$1,000 | None | S$5,000 (recommended) |

| Maximum Investment | None | None | None |

| Term | 6 months or 1 year | Flexible | Flexible |

| Redemption | No early redemption | Anytime | Anytime |

| Withdrawal Penalty | Can be sold (value not guaranteed) | None | None |

| Capital Guaranteed | Yes | No | No |

*Indicative June 2025 market levels. Yields may vary.

Ready to boost your passive income? Explore Syfe Income+ and start earning higher yields today.

Disclaimer: All yields quoted are forward-looking estimates and not guaranteed. Past performance is not indicative of future returns. Investments present risks, including possible loss of principal.

You must be logged in to post a comment.