With core inflation in Singapore projected at 3.5% to 4.5% in 2023, consumers are looking for better places to park their cash. Products such as fixed deposits, T-Bills and Singapore Savings Bonds (SSBs) have risen in popularity over the past year as investors look to protect the value of their money as these instruments offer high impressive yields in today’s rising rate environment. But are they truly the best investment you can get for your money? In this article, we unpack the differences between T-Bills, SSBs, fixed deposits and Income+.

Understanding Bonds and Fixed Income Instruments

Fixed-income securities typically include bonds, notes and other debt instruments issued by governments, corporations and other entities.

In Singapore, the most popular bonds are issued by the government, namely as Singapore Savings Bonds (SSBs) and Treasury Bills (T-Bills).

SSBs pay an interest every 6 months at a fixed rate (pre-determined by the government before subscription) which steps up every year for up to 10 years. It is a safe option for those looking for a long term and steady option.

T-bills however, offer a different value proposition, where it is sold at a discount, but upon maturity given back to the investor with a full face value of the bill. The investment duration is 6 months or 1 year. The rate is determined at an auction, the bill is also tradeable.

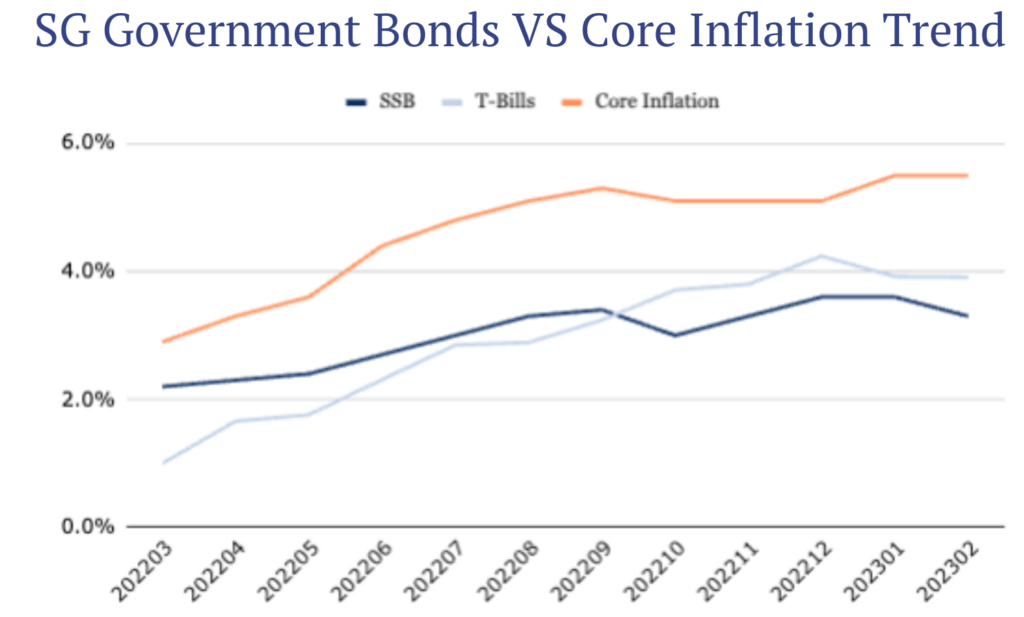

As investors seek to mitigate risks associated with market fluctuations, many Singaporeans have invested in SSBs and T-Bills as they are deemed to be safer and less volatile investments. While the yields for T-Bills and SSBs look attractive, if they are your only investments, you may want to relook your strategy as the rates paid are unlikely to keep pace with rising inflation in the long run.

The current interest rates offered by SSBs (2 March 2023 cut-off yield at 3.98%), T-Bills (1 April 2023 10-year effective interest rate offered at 3.15% per annum), and fixed deposits (offer between 3.20% to 4.10% for 12-month deposit in March 2023) do not match the current high core inflation rate. Since inflation is averaging at 5% currently, given the stark difference, these instruments may not be adequate to cover inflation in the long run. Additionally, the returns from both of these instruments have been steadily declining since December 2022 (refer to both charts below). As such, you may want to explore other fixed-income securities that can provide stable income with better returns.

SSBs interest rates are taken based on 10-year maturity. T-Bill yields are based on 1-year tenor and taken from the last day of the month.

Understanding Fixed Deposits

Fixed or time deposit is an extremely low-risk way to grow your money without losing capital. You commit to depositing your money to a bank upon agreed amount and tenor while getting a fixed rate of interest in return. Available rates are as high as 4.0% (as of April 2023), but they are often capped and/or tied to specific promotions, duration, and minimum deposit requirements. Investors can compare the latest Fixed Deposit Rates in Singapore before deciding which option best suits their needs. While the advertised rate looks attractive, one must keep in mind T&Cs and disadvantages of having your money locked in to qualify for a higher interest rate.

Could we generate better returns with fixed-income securities?

Syfe Income+ portfolios can offer better yields and dividend payouts with two options available: (1) Income+ Preserve at 4.0-4.5% p.a. payout and (2) Income+ Enhance at 5.0-6.0% p.a. payout. Income+ portfolios invests in fixed income assets globally and is managed to optmise income return for investors. Read more about the portfolio here.

Unlike SSBs, T-bills and fixed-deposits, investors can expect monthly payouts at an attractive distribution yield of 4.0-6.0% p.a*. That’s because Syfe Income+ funds consist of bond funds invested globally, including bonds with higher yields and thus are expected to deliver high targeted returns to investors. Income+ is built with a unique portfolio construction process informed through PIMCO’s forward looking views and time tested investment approach, making it an institutional grade solution accessible by any investor.

Syfe Income+ is a more flexible option as there are no lock-in periods, and you can withdraw anytime with no fees.

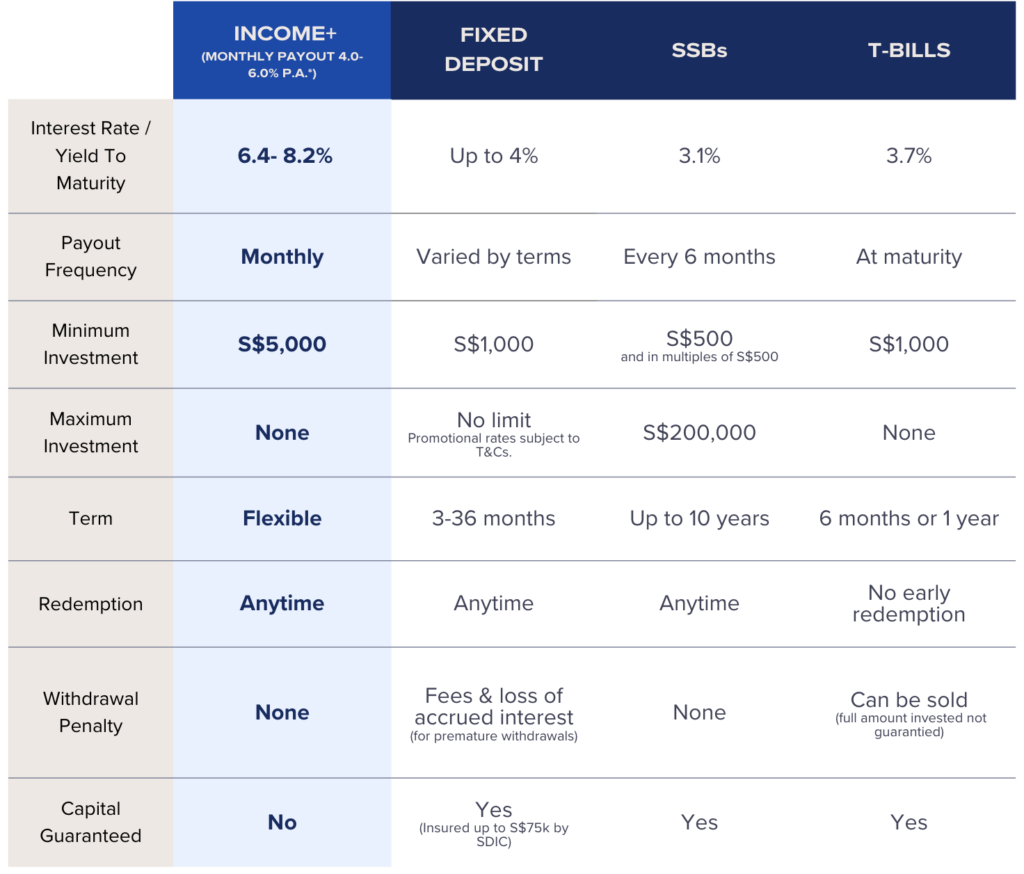

Income+ vs Fixed Deposits, SSBs, T-bills

Here’s a quick overview of a comparison of Syfe Income+ funds with fixed deposit, SSBs and T-Bills:

Source: Syfe’s Research as of 30 Apr, 2023

Why Income+ can be a good option

While different products offer different advantages, Income+ could be a better alternative for investors seeking competitive yield while maintaining control and flexibility over their money. Income+ offers a competitive yield with monthly payouts and no locked-in terms. Additionally, the portfolio pays out on a monthly basis so those looking for a supplementary passive income stream could benefit from this portfolio compared to a longer payout schedule of other bond or fixed deposit products.

Create an Income+ portfolio today and discover the benefits of a purpose-built portfolio for all your income needs.

More articles on Income+

- Income+ Investment Strategy & Portfolio Construction

- Constructing a Bond Portfolio with ETFs vs Unit Trusts

This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

You must be logged in to post a comment.