If you have decided to allocate a portion of your portfolio to bonds, the next thing to consider is how you would want to invest in bonds. Bond investors in Singapore have the option of adding bonds to their portfolio through:

- Individual bonds

- Bond ETFs

- Actively managed bond funds

Investing in Individual Bonds

Singapore Government Bonds

Bonds are typically issued by governments and corporations. In Singapore, the government issues Treasury bills (T-bills) and Singapore Savings Bonds (SSBs). An investor may commit a minimum of S$1,000 to purchase T-bills and a minimum of S$500 to invest in SSBs. These securities are regarded as very safe, as they are issued by the Singapore government, it is very likely that you will receive your coupon payments and principal in a timely manner with a very low risk of default.

Corporate Bonds

Purchasing individual corporate bonds requires a significantly higher initial investment amount. Normally one lot is sold for a minimum of S$250,000. This can take up a large chunk of your portfolio and cause concentration risk. Let’s say if the bond defaults, it can have a severe impact on your overall portfolio.

Doing it Yourself with Bonds And the Potential Downsides

1. Upfront cost of time and effort

Buying individual bonds also entails you to be responsible for researching and monitoring the financial stability of the issuer to see whether the entity can fulfil payments. If you invest in a corporate bond, it is important to keep track of the company’s performance because there is a chance you may lose money if the company goes bankrupt. For government bonds, you will have to keep an eye on the country’s economy and how its central bank manages interest rates. You need to have a good understanding of the mechanics of the key factors – credit rating, interest rates and structure – that affect the bond price. Aside from determining the fair price of the bond, you will also need to consider other factors such as whether to keep the bond until maturity, sell it before maturity, or buy bonds from the secondary market.

2. Lack of diversification

Unlike equities, retail investors may not be able to access a range of bonds due to higher minimum investment requirements for some individual bonds, the minimum investment can be up to $250,000 or $1,000,000. Many retail investors do not have access to large sums of capital, which limits the opportunity to take advantage of diversification within the fixed income asset class.

As you can see, managing a portfolio of individual bonds can be quite complex, costly and time consuming for an investor. Another option an investor can gain exposure to bonds is either by investing in actively managed bond funds or purchasing bond ETFs. Not only do they provide bond exposure without the need for extensive capital or time investment, but they also offer the potential for greater diversification, liquidity and higher returns to your portfolio.

What about a bond unit trust / mutual fund or ETFs?

Both bond funds and bond ETFs offer a diverse range of benefits to investors. As both these hold a basket of individual bonds, they provide a means of reducing concentration risk in your portfolio. Their basket typically contains different bond types such as sovereign debt, corporate debt, agency debt, and asset-backed securities, which can help spread your risk across various holdings.

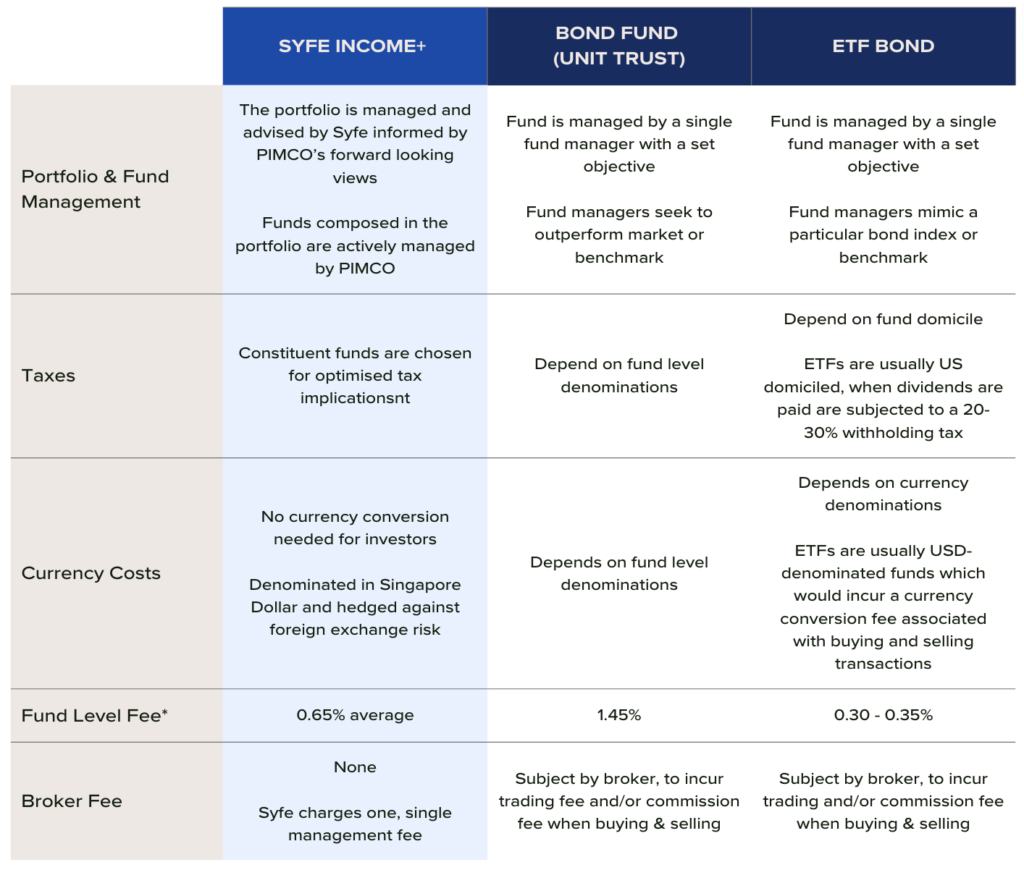

Why can actively managed bond funds be better than bond ETFs?

Actively managed bond funds are managed by professional fund managers who make investment decisions with a goal of outperforming a particular benchmark or achieving a specific investment objective while bond ETFs seek to passively follow an index. The benefits of having active fund management for bonds is frequent optimisation towards a set objective whether that’s yield maximisation or capital protection. Unlike equity markets, there is a considerably much lower availability of bond ETFs in the market. Since bond instruments are built with income as an objective, currency denominations, fund domicile needs to be taken into consideration. Actively managed funds in this case may offer better currency hedges as well as tax savings for dividend payouts.

Income+ vs Bond Fund, Bond ETF

Source: Syfe’s Research as of 30th April, 2023

Why Income+ might be a good option for those building a bond portfolio

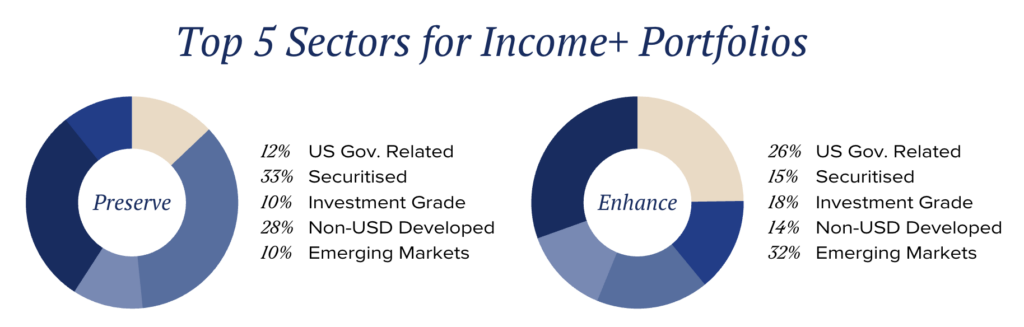

- Highly diversified fixed income assets

Updated as of 30 April, 2023

Income+ uses PIMCO funds that are actively managed and are able to utilise a broad range of fixed income securities that seek to produce an attractive level of income while maintaining a relatively low risk profile. The portfolio consists of fixed income assets such treasury, investment grade, high yield across developed and emerging markets making it very well diversified. See portfolio composition.

- Managed and hassle free investing

Syfe offers ongoing recommendations on portfolio optimisation on a semi-annual basis. These recommendations will be informed by PIMCO’s forward looking views on the market based on credit spreads, yields, and economics forums to identify the most attractive investments.

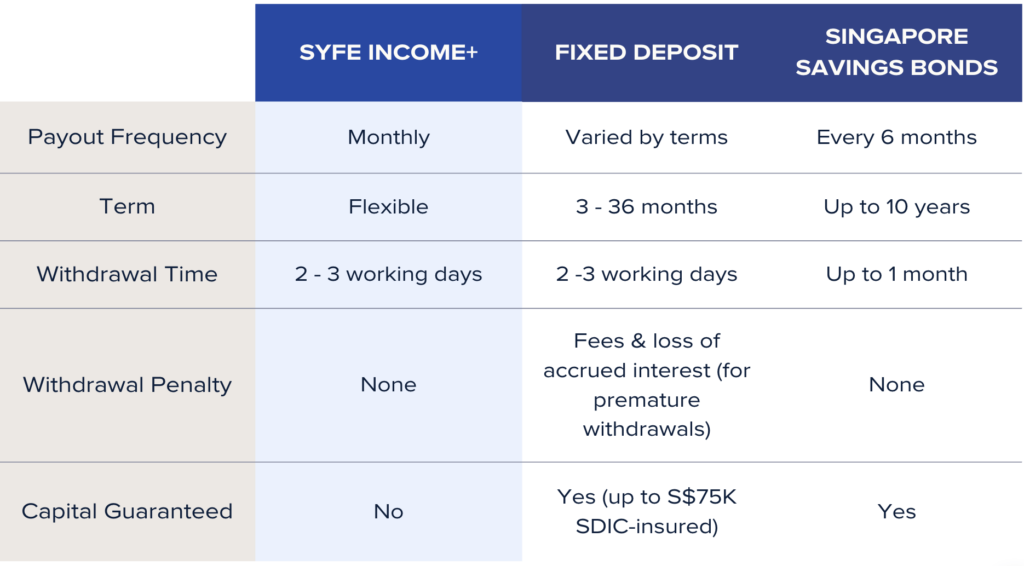

- Attractive yields with high liquidity

As with all Syfe portfolios, Income+ offers no lock-ins, free unlimited portfolio transfers and zero withdrawal fees to provide you with the flexibility and agility you need as you build wealth for the long-term.

Read more about how we construct Income+ here.

In conclusion, adding an actively managed bond fund to a diversified portfolio can be a valuable investment strategy. To maximize the potential returns, it’s recommended to choose a bond fund that is actively managed by a world-class fixed-income asset manager such as PIMCO. With their extensive expertise and experience, they are better equipped to navigate the complex and often unpredictable fixed-income markets, especially during volatile times. Incorporating Syfe Income+ into your portfolio can help you achieve your investment goals and increase the overall stability of your investment portfolio.

Create an Income+ portfolio now and grow your money to its fullest potential with Syfe.

This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

You must be logged in to post a comment.