Singapore’s office REITs are benefiting from tight supply, resilient demand, and the return-to-office trend. Here’s why prime assets continue to shine in 2025 and how investors can gain exposure.

Singapore’s Office Real Estate Investment Trusts (REITs) form a vital part of the local and regional investment landscape. As one of the most developed and liquid REIT markets in Asia, Singapore’s S-REIT sector has a total market capitalisation of over S$86 billion, with office-focused REITs commanding multi-billion-dollar portfolios of premium commercial properties.

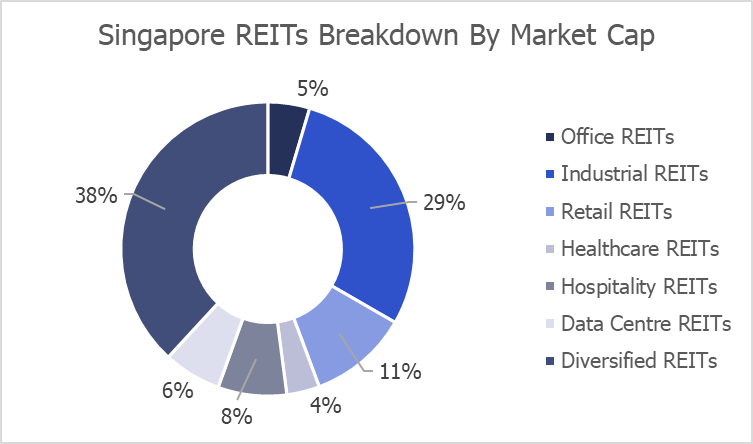

Although office REITs account for about 5% of the total S-REIT sector by market cap, many diversified REITs also own sizeable office assets within integrated developments, retail-office complexes, or overseas portfolios. In fact, more than 90% of Singapore-listed REITs hold assets beyond Singapore, offering investors exposure to both domestic and international property markets.

Against this backdrop, Singapore office REITs remain a core asset class for investors seeking long-term stability, consistent yields, and exposure to high-quality, income-generating properties.

The Evolution of Singapore’s Office REIT Sector

The growth story of Singapore office REITs has moved well beyond simple expansion. Today, REIT managers are increasingly focused on quality, strategic asset enhancement initiatives (AEIs), and capital recycling to future-proof their portfolios.

Tenants are prioritising premium, sustainable, and well-located office environments that form part of “live-work-play” precincts, designed to attract and retain top talent. As a result, REITs are upgrading older properties and recycling capital into modern, Grade A buildings that deliver long-term value.

This qualitative focus is paying off. Grade A offices in Singapore’s central business district (CBD) continue to outperform older stock, supported by both limited new supply and resilient demand from multinational corporations.

| Company | Ticker | Market Cap SGD (bn) |

| Keppel REIT | K71U | 3.10 |

| Suntec REIT | T82U | 3.30 |

| OUE REIT | TSOU | 1.71 |

| CapitaLand Integrated Commercial Trust | C38U | 15.30 |

| MapleTree Pan Asia Commercial Trust | N2IU | 7.10 |

| Prime US REIT | OXMU | 0.29 |

| Keppel Pacific Oak | CMOU | 0.27 |

| Manulife US REIT | BTOU | 0.16 |

| Elite UK REIT | MXNU | 0.37 |

| Lendlease Global REIT | JYEU | 1.40 |

Key Drivers of Performance for Singapore Office REITs

Tight Supply and Sustainable Demand Support Rental Growth

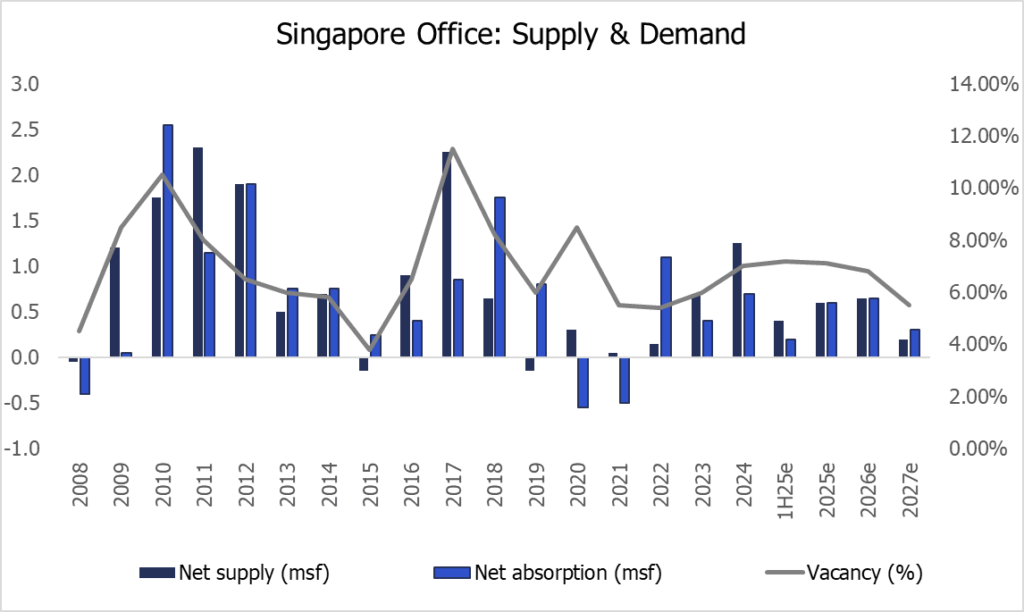

The supply pipeline of Grade A CBD office space remains constrained. No new CBD Grade A completions are expected in the second half of 2025, and from 2025 to 2027, annual new supply will average just 0.58 million sq ft—about 55% lower than the historical 10-year average.

Only three major projects—Shaw Tower, Solitaire on Cecil, and Newport Tower—are scheduled for completion through 2027. With net absorption expected to exceed net supply, demand-supply dynamics look highly favourable for landlords.

Demand is also resilient across industries. In the most recent quarter, new leases were led by finance and insurance (35%), technology (20%), and law and consultancy (18%), reflecting a diverse tenant base.

Return-to-Office (RTO) and Flight-to-Quality

The pandemic sparked a wave of remote work, but Singapore has emerged as one of the markets leading the return-to-office (RTO) trend. Occupancy data from Q2 2025 shows average weekly office usage at 77%–78%, reflecting the widespread adoption of hybrid models anchored around in-office collaboration.

This RTO momentum is fueling a flight-to-quality trend. Corporates are consolidating or relocating into modern, Grade A developments that offer sustainability credentials, advanced amenities, and prime locations. Since 2020, prime office rents have risen 11.8%, compared to just 4.8% for older assets.

Success stories include IOI Central Boulevard Towers and Keppel South Central, which have attracted marquee tenants such as Amazon and Manulife. With limited new supply in the pipeline, best-in-class assets are set to maintain their rental and capital value growth.

Capital Recycling and Portfolio Optimisation

Singapore office REITs are increasingly active in capital recycling, ensuring that portfolios remain resilient and competitive.

- CapitaLand Integrated Commercial Trust (CICT) recently acquired the remaining 55% stake in CapitaSpring for S$1.0 billion, giving it full ownership of the Grade A integrated development in Raffles Place.

- Mapletree Pan Asia Commercial Trust (MPACT) divested two Japanese office properties for JPY 8.73 billion, sharpening its portfolio focus.

- City Developments sold its 50.1% stake in South Beach to IOI Properties, freeing up capital and lowering leverage.

With interest rates declining, the pace of recycling is expected to increase, creating opportunities for REITs to enhance earnings and distributions.

Singapore’s Stability as a Global Business Hub

Singapore’s political stability, transparent governance, and strong rule of law make it one of the world’s most attractive destinations for multinational corporations. The tenant mix across major office REITs is highly diversified, spanning banking, insurance, asset management, IT, and consulting. This structural strength underpins consistent demand and enhances the resilience of the sector across economic cycles.

Why Investors Should Consider Singapore Office REITs

1. Distribution Per Unit (DPU) Upside from Lower Borrowing Costs

With benchmark rates easing, many office REITs are seeing a decline in financing costs. REITs with higher floating-rate debt, such as Keppel REIT and Suntec REIT, stand to enjoy meaningful near-term upside in DPU.

2. Positive Outlook for CBD Grade A Offices

The combination of limited new supply, resilient tenant demand, and a favourable interest rate environment supports a positive outlook for prime office rents over the next few years.

3. Flight-to-Quality Sustains Rental Reversions

Occupancy rates remain high, with Core CBD Grade A vacancy at just 5.3% in Q2 2025. Premium properties continue to attract tenants from diverse industries, enabling landlords to achieve positive rental reversions.

4. Superior Asset Quality and Operational Performance

REITs such as Keppel REIT, Suntec REIT, and CICT own landmark properties including Marina Bay Financial Centre and One Raffles Quay, which enjoy above-market occupancy and strong tenant demand.

5. Attractive Yields Backed by Hard Assets

Singapore office REITs offer stable distributions, supported by tangible, income-producing properties in a land-scarce environment. This enhances long-term value while offering investors yield spreads above risk-free assets.

How Investors Can Gain Exposure: Syfe’s REIT+ Portfolio

For investors seeking diversified exposure to Singapore’s REIT market without having to pick individual names, a simple option is to consider Syfe’s REIT+ portfolio.

The REIT+ portfolio comprises the top 20 Singapore-listed REITs, tracking the iEdge S-REIT Leaders Index, which is widely regarded as the benchmark for Singapore’s REIT sector. This provides:

- Broad exposure across office, retail, industrial, and diversified REITs.

- High-quality assets including Marina Bay Financial Centre, One Raffles Quay and Mapletree Business City.

- Stable distributions backed by Singapore’s most established property trusts.

By investing through a managed portfolio like REIT+, investors can gain convenient access to Singapore’s REIT ecosystem, including the office REIT sub-sector, while benefiting from professional management and regular rebalancing.

Conclusion: A Strong Case for Singapore Office REITs

Singapore office REITs are entering a favourable phase in 2025. Limited supply, resilient tenant demand, and the accelerating return-to-office trend are underpinning rental growth for Grade A assets. Coupled with falling interest rates, capital recycling, and Singapore’s status as a global business hub, the investment case for office REITs looks compelling.

For income-focused investors, office REITs remain an attractive source of yield backed by tangible assets in one of the world’s most stable and dynamic economies. Whether accessed through individual REITs or diversified portfolios like Syfe’s REIT+, Singapore office REITs deserve a close look as a long-term allocation within a balanced investment strategy.

Read More:

Why S-REITs Could Be Poised for a Bounceback in 2025

What’s Driving the Growth in Singapore Retail REITs in 2025

How to Pick Resilient REITs in Singapore’s Property Market Recovery

You must be logged in to post a comment.