The latest rebalance exercise enhances Core portfolios with broader global diversification, improved factor balance, and greater resilience across asset classes for long-term, sustainable growth.

Markets are entering a new phase. After years of US market dominance, led by mega-cap technology giants, global leadership is beginning to broaden. Syfe’s latest Core Portfolio rebalance reflects this shift, reaffirming its commitment to global diversification, factor-based investing, and disciplined portfolio management.

We have optimised the Syfe Core portfolios across regions, factors, and asset classes to ensure the portfolios continue to capture long-term growth opportunities as global leadership evolves. These updates strengthen portfolio resilience while positioning investors to capture long-term opportunities in a changing global landscape.

Key Highlights

- Broadened equity exposures from US to International markets: Increased international exposure through developed markets, whilst maintaining emerging markets positions, to capture opportunity and reduce US concentration risk.

- Enhanced US equity factor strength: Refined US exposures and added further profitability exposure (via Dimensional) to complement our existing exposures and strengthen overall factor performance.

- Improved multi-asset resilience: Adjusted fixed income and gold allocations to manage interest-rate sensitivity and balance after gold’s recent rally.

Broadening Beyond the US: Capturing Global Growth

The US market has delivered exceptional performance in recent years, led by a small group of large technology companies. However, its valuations are now elevated, and growth leadership may start to rotate. With the dollar softening and growth prospects improving in regions like Europe and Japan, diversification beyond the US is increasingly important.

- Developed markets: We have increased exposure to developed markets outside the US to reduce concentration risk and capture opportunities in regions such as Europe and Japan that may benefit from improving global growth and a softer dollar.

- Emerging markets: Maintained emerging market exposure around 14%, including our long-term conviction in China (rallied over 35% YTD in USD), which remains underrepresented in global benchmarks, and broadening exposure across developing economies through diversified holdings.

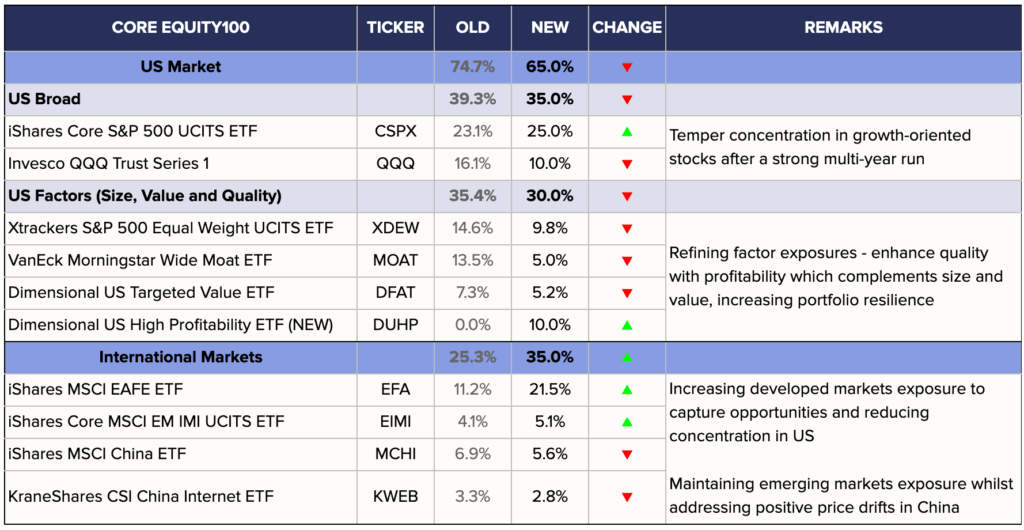

Following this rebalance, Syfe’s Core Equity100 portfolio—a pure equity allocation—now reflects the following regional composition:

- US: ~65%

- Developed ex-US: ~21%

- Emerging Markets: ~14%

This mirrors the global opportunity set represented by the MSCI ACWI while reducing concentration risk in any single region. The increased emphasis on profitability and global diversification ensures that the portfolios are positioned for both growth and resilience, regardless of where market leadership shifts next.

Enhancing US Factor Balance: A Focus on Profitability

Within the US, we’ve refined both our broad market and factor exposures to enhance diversification and balance.

- Market (Beta): We have tempered concentration in growth-oriented stocks after a strong multi-year run by trimming Invesco QQQ (QQQ) which focuses heavily on mega-cap tech combined with a modest increase to iShares Core S&P 500 (CSPX)

- Quality / Profitability: We have strengthened our exposure to high-quality, profitable US companies by introducing Dimensional US High Profitability ETF (DUHP). DUHP focuses on large and mid-cap firms with consistently high returns on capital, providing a systematic and broad-based way to invest in quality companies. It complements our existing VanEck Morningstar Wide Moat ETF (MOAT), and together, these exposures enhance our overall factor balance—combining analyst-assessed quality with data-driven profitability to capture complementary drivers of return.

- Value & Size: Xtrackers S&P 500 Equal Weight (XDEW) and Dimensional US Targeted Value (DFAT) have seen small trims as part of our broader rebalancing across the factor sleeve.

Academic research shows that highly profitable companies tend to perform well even when other factors, like value or size, lag. Incorporating this exposure helps balance the portfolio’s factor mix and supports resilience through varying market cycles.

The table below summarises the updated allocation within our all-equity portfolio, Equity100, following this rebalance.

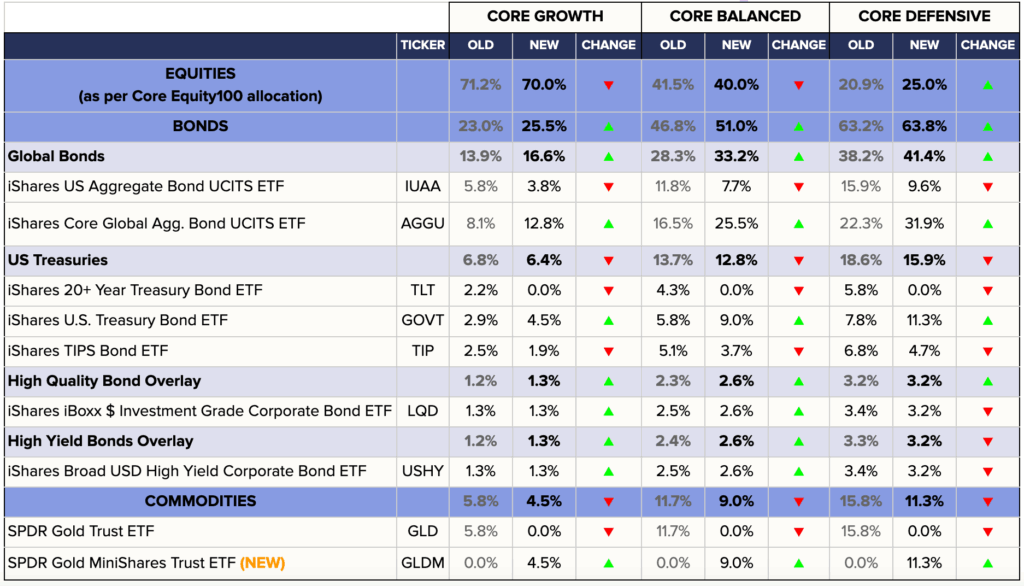

Multi-Asset Portfolios: Refined Fixed Income allocation and reduced Gold expense ratio

In our multi-asset Core portfolios, we’ve made refinements to the fixed income and gold allocations to enhance portfolio balance and resilience.

Fixed income: Balancing and reducing interest-rate sensitivity

The bond component now reflects:

- Reduced US concentration, improving balance across global issuers.

- Shorter duration, lowering sensitivity to interest rate movements while maintaining quality exposure to government and corporate bonds.

These changes enhance fixed income’s role as a stabilizer within the portfolio, providing steady income and downside protection in volatile markets. The updated allocations remain consistent with global benchmarks, ensuring no compromise on diversification or credit quality.

Gold: Locking in gains and improving cost efficiency

Gold’s strong performance this year led to an overweight drift in portfolios. Syfe has trimmed gold exposure slightly, locking in gains while maintaining its strategic role as a diversifier and store of value.

At the same time, gold holdings have been switched to the SPDR Gold MiniShares ETF (GLDM), a lower-cost vehicle that offers the same exposure with 30 basis points (75%) saving. This reflects Syfe’s continued focus on cost efficiency and disciplined rebalancing.

The updated fixed income and gold allocations are shown below, reflecting our efforts to reduce interest-rate sensitivity and enhance portfolio balance.

Year-to-Date Performance: Solid Returns Amid Market Rotation

In 2025, global markets have been shaped by easing inflation, steady economic growth, and moderating interest rates. While the MSCI ACWI has been driven largely by a handful of US tech names, Syfe’s diversified approach has delivered strong and steady results.

- Equity100 has returned +17.69% year-to-date, capturing robust equity market gains.

- The multi-asset Core portfolios have gained +13.67% to +16.08%, reflecting balanced exposure across equities, bonds, and gold.

These results highlight the benefits of broad diversification and systematic factor investing, which together help mitigate concentration risk and support consistent long-term growth.

Staying True to a Disciplined, Factor-Based Philosophy

Every refinement in this rebalance is guided by Syfe’s factor-based investment process—a data-driven, research-backed framework that emphasises diversification, efficiency, and exposure to proven return drivers such as value, size, and quality/profitability.

This disciplined approach ensures that portfolio updates are grounded in long-term evidence, not short-term market sentiment. As global dynamics evolve, Syfe continues to evaluate new data, ETFs, and tools to deliver the best implementation for investors.

Our investment philosophy remains unchanged: to build globally diversified, cost-efficient portfolios designed for sustainable, long-term growth.

Syfe Core Portfolios: Built for the Future

With this latest rebalance, Core portfolios are more balanced, globally diversified, and factor-intelligent than ever. By expanding beyond US concentration and increasing emphasis on profitability and global diversification, we ensure that our portfolios are positioned for both growth and resilience, regardless of where market leadership shifts next.

To hear more about the latest rebalancing exercise, sign up for our upcoming webinar on 18 Nov 2025, where we’ll explain these changes in detail and answer your questions.

Invest smarter with Syfe Core portfolios—globally diversified, factor-driven, and built for long-term success.

You must be logged in to post a comment.