FIRE—Financial Independence, Retire Early—often sounds unrealistic in one of the world’s most expensive cities. But for Singaporeans willing to rethink retirement, redefine success, and invest strategically, FIRE may be more achievable than it seems.

Singaporeans are raised on a familiar financial script: study hard, build a stable career, buy a home, raise a family, work until your 60s, then finally retire. It’s a path that prioritises security and stability. However, many young professionals are increasingly questioning whether it’s the only option.

With rising living costs, longer working hours, and growing awareness of burnout, the idea of waiting until 65 to enjoy life feels outdated. This is where FIRE enters the conversation.

Yet FIRE in Singapore often sounds like a contradiction. How do you retire early in a city with expensive housing, inflation pressures, and high opportunity costs? Is FIRE only for tech founders and high-income expats, or can regular salaried Singaporeans realistically pursue financial independence?

The reality sits somewhere in between. FIRE is possible in Singapore—but probably not quite from retiring at 35. Instead, it’s about building enough financial resilience to gain freedom, flexibility, and choice earlier in life. And with the right investment strategy, that goal is more attainable than you may think.

Table of Contents

- What Is FIRE?

- What Does Financial Independence Really Mean?

- Why the FIRE Movement Resonates in Singapore

- The Different Types of FIRE

- How Much Do You Need to Retire in Singapore?

- Is FIRE in Singapore Actually Feasible?

- How to Fast-Track Your Retirement

- How to Invest to Retire Early

- Ways to Invest for FIRE with Syfe

- Final Thoughts: Redefining Retirement on Your Own Terms

What Is FIRE, Really?

At its core, FIRE stands for Financial Independence, Retire Early. But the term “retire” is often misunderstood.

FIRE does not necessarily mean never working again. Instead, it means reaching a point where your investments generate enough income to cover your living expenses, so paid employment becomes optional rather than compulsory.

This distinction is especially important in Singapore, where many people enjoy working but want relief from:

- High-pressure roles

- Long working hours

- Financial stress

- The fear of job insecurity

FIRE shifts the focus from accumulating wealth for its own sake to using money as a tool to buy back your time. Whether that time is spent with family, on passion projects, or in lower-stress work is entirely up to you.

Financial Independence in a Singapore Context

Financial independence means different things to different people, depending on lifestyle expectations and personal circumstances.

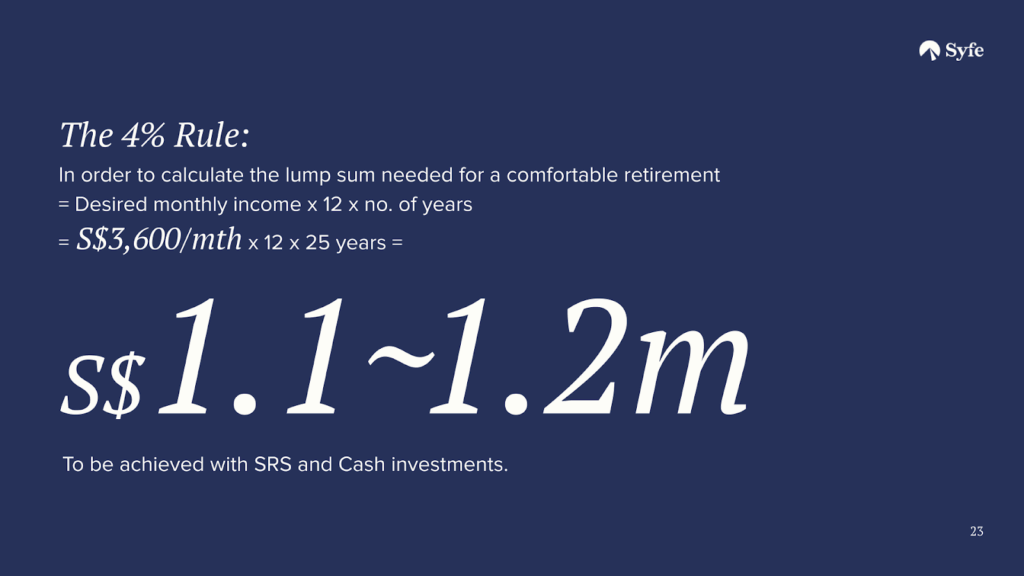

A commonly referenced guideline in FIRE discussions is the 4% rule, which suggests that if you withdraw 4% of your investment portfolio annually, your money has a high probability of lasting for 30 years or more. For example, if you need S$60,000 a year to live comfortably, you would aim for a portfolio of about S$1.5 million.

However, many Singaporeans prefer to be more conservative. Given Singapore’s long life expectancy, rising healthcare costs, and market volatility, some aim for a 3–3.5% withdrawal rate, particularly if they plan to retire early and need their money to last 40 to 50 years.

Financial independence, then, isn’t about hitting a single magic number. It’s about ensuring that your investments can sustainably support your chosen lifestyle without forcing you to work longer than you want to.

Why the FIRE Movement Resonates in Singapore

FIRE has gained traction locally not because Singaporeans dislike work, but because the traditional model of retirement feels increasingly misaligned with modern realities.

First, the cost of living continues to rise. Housing, education, and healthcare expenses place long-term pressure on household finances, making early and intentional planning essential.

Second, career burnout is real. Many professionals reach their 30s or 40s feeling financially successful on paper but mentally exhausted. FIRE offers a way to reduce dependency on a single income stream.

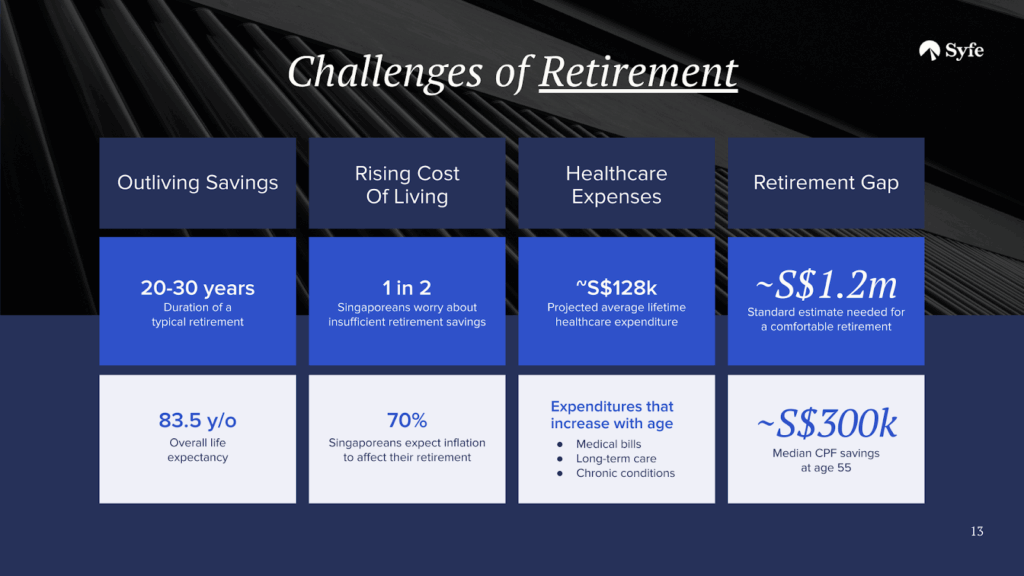

Third, Singaporeans are living longer. A longer lifespan means retirement could last 25 to 30 years or more. Waiting until your mid-60s to think seriously about financial independence may no longer be sufficient.

Finally, FIRE aligns with a growing desire for life flexibility. More people want the freedom to travel, care for family members, start businesses, or pursue meaningful work without being constrained by monthly bills.

The Different Types of FIRE (And What Works in Singapore)

Not all FIRE journeys look the same, especially in a high-cost city like Singapore.

Lean FIRE focuses on extreme frugality and low expenses. While possible, it often requires significant lifestyle trade-offs that may not be appealing or sustainable for many Singaporeans.

Fat FIRE aims for early retirement with a higher standard of living. This typically requires a very high income or business success and may be out of reach for the average professional.

More realistic for most are Coast FIRE and Barista FIRE.

Coast FIRE involves building a substantial investment portfolio early, then letting compounding do the heavy lifting while you continue working to cover day-to-day expenses.

Barista FIRE—particularly popular in Singapore—means having enough investments to cover a portion of your expenses, allowing you to work part-time, freelance, or take on lower-stress roles without financial anxiety.

These models recognise that FIRE doesn’t have to be all-or-nothing. Partial financial independence can still dramatically improve quality of life.

Read Also:

- Micro-Retirement in Singapore: How to Make It Work For You Financially

- Semi-Retirement: The Alternative Path to Financial Freedom

How Much Do You Need to Retire in Singapore?

There is no universal FIRE number, but a practical way to approach it is to start with your annual spending.

A modest but comfortable lifestyle for a couple might require S$50,000–S$70,000 annually, while families or those aiming for more flexibility may need S$80,000 or more.

Using a conservative 3.5% withdrawal rate:

- S$60,000 annual spending ≈ S$1.7 million portfolio

- S$80,000 annual spending ≈ S$2.3 million portfolio

These figures can seem intimidating, but they are built over decades, not overnight. CPF, rental income, side businesses, and part-time work can also supplement investment withdrawals.

Read Also: How Much Do You Need to Retire in Singapore?

Is FIRE in Singapore Actually Feasible?

The short answer: yes, but only with intentional planning and investing.

Singapore’s advantages often go overlooked in FIRE discussions. Political stability, strong market regulation, low capital gains taxes, and access to global markets make long-term investing more predictable than in many countries.

Additionally, CPF—when used strategically—can serve as a powerful retirement foundation, reducing the pressure on private investments later in life.

The key challenge isn’t feasibility. It’s starting early enough and investing consistently enough to harness the power of compounding.

Try Also: Syfe’s Compound Interest Calculator

How to Fast-Track Your Retirement

Achieving FIRE is more about aligning your wealth accumulation strategy to your goals than extreme deprivation.

Saving more matters, but investing wisely matters more. Cash alone rarely beats inflation over the long term. To retire early, your money must work harder than you do.

Increasing income, whether through career progression or side ventures, accelerates your FIRE timeline. But lifestyle inflation should be kept in check. Every dollar not spent is a dollar that can compound for decades.

Most importantly, having a clear investment strategy—rather than chasing trends or timing markets—keeps you disciplined through market cycles.

How to Invest to Retire Early

Early retirement depends on long-term, growth-oriented investing. That typically means:

- Diversified exposure to global equities

- A risk level aligned with your time horizon

- Automatic, consistent investing

Rather than picking individual stocks or trying to outsmart the market, many FIRE-focused investors prefer diversified portfolios that grow steadily over time.

This is where goal-based investing becomes powerful. Different portfolios can serve different purposes—long-term growth, income generation, or stability—depending on where you are in your FIRE journey.

Ways to Invest for FIRE with Syfe

For Singaporeans pursuing financial independence, Syfe’s portfolios are designed to match different FIRE stages.

Syfe Core is particularly well-suited for long-term FIRE goals. It offers globally diversified exposure across equities and bonds, automatically rebalanced to maintain your chosen risk level. For those in their 20s to 40s, Core provides a disciplined way to compound wealth over decades without constant monitoring.

As you approach partial or early retirement, Income+ can help generate more stable income through diversified fixed-income assets, while REIT+ offers exposure to real estate investment trusts for income potential and diversification.

Used together, these portfolios can support both growth during accumulation years and income generation during early retirement or Barista FIRE.

Redefining Retirement on Your Own Terms

FIRE in Singapore doesn’t mean just escaping the nine-to-six or living an ultra-frugal life. It means building enough financial independence to live life more intentionally and flexibly.

Whether your goal is early retirement, Barista FIRE, or simply peace of mind, the journey starts with investing early, staying consistent, and choosing strategies aligned with your long-term goals.

You may not retire at 35, but you might buy yourself freedom at 45. And that, for many Singaporeans, could just be FIRE enough.

Ready to take your first step toward financial independence?

Explore Syfe Core, alongside Income+ and REIT+, to build a diversified portfolio designed to support your journey toward early retirement—on your own terms.

Read More:

- How Much Do You Need to Retire in Singapore?

- Micro-Retirement in Singapore: How to Make It Work For You Financially

- Semi-Retirement: The Alternative Path to Financial Freedom

- CPF Changes in 2026: What They Mean for Your Retirement — and Why CPF Alone May Not Be Enough

- Top SRS Investment Options to Grow Your Retirement Savings

You must be logged in to post a comment.