Investing is one of the most powerful ways to build wealth over the long term. At its heart sits a simple idea: your money can make more money over time, through a concept known as compounding. The earlier you understand it, the more it can work in your favour.

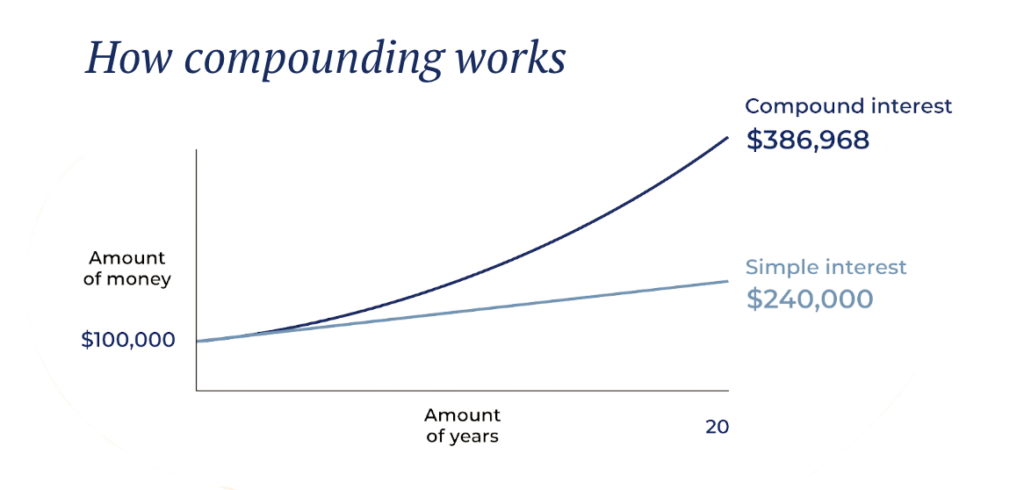

Here is the idea in one example. Suppose you invest S$100,000 today and it grows at a steady 7% a year. Twenty years later, it would have more than tripled to roughly S$386,968 — without you adding another cent. By contrast, if you withdrew the gains each year instead of leaving them to grow, you would collect about S$7,000 a year, or S$140,000 over the same period. The difference — close to S$247,000 — is compounding at work.

What is compound interest (and how it differs from simple interest)

Compound interest is interest earned on top of interest you have already earned. Each time your returns are added to your balance, the next round of returns is calculated on that larger base. Over time this creates a snowball effect: growth builds on growth.

Simple interest, by contrast, is paid only on your original capital. The contrast is easiest to see side by side:

| Feature | Simple interest | Compound interest |

|---|---|---|

| What earns interest | Only your original capital | Your capital plus all interest already earned |

| Growth shape | Straight line | Accelerating curve (a snowball) |

| S$10,000 at 5% for 20 years* | S$20,000 | About S$26,533 |

*Illustrative, assuming interest is added once a year and no withdrawals. Figures are rounded.

How compounding is calculated — the formula and the Rule of 72

The textbook formula is A = P (1 + r/n)^(n×t): your final amount (A) depends on your starting capital (P), the annual rate (r), how many times a year interest is added (n) and the number of years (t). You do not need to crunch this by hand.

A faster shortcut for a rough sense of speed is the Rule of 72: divide 72 by your expected annual return to estimate how many years it takes to double your money. At 6% a year, that is about 12 years (72 ÷ 6); at 8%, about nine. It is an approximation, not a guarantee, but it makes the power of a higher rate — and a longer runway — easy to feel. You can test different assumptions with Syfe’s compound interest calculator.

Why time is your biggest advantage

To get the most from compounding, time is your best friend. The earlier you start, the longer your returns have to earn returns of their own.

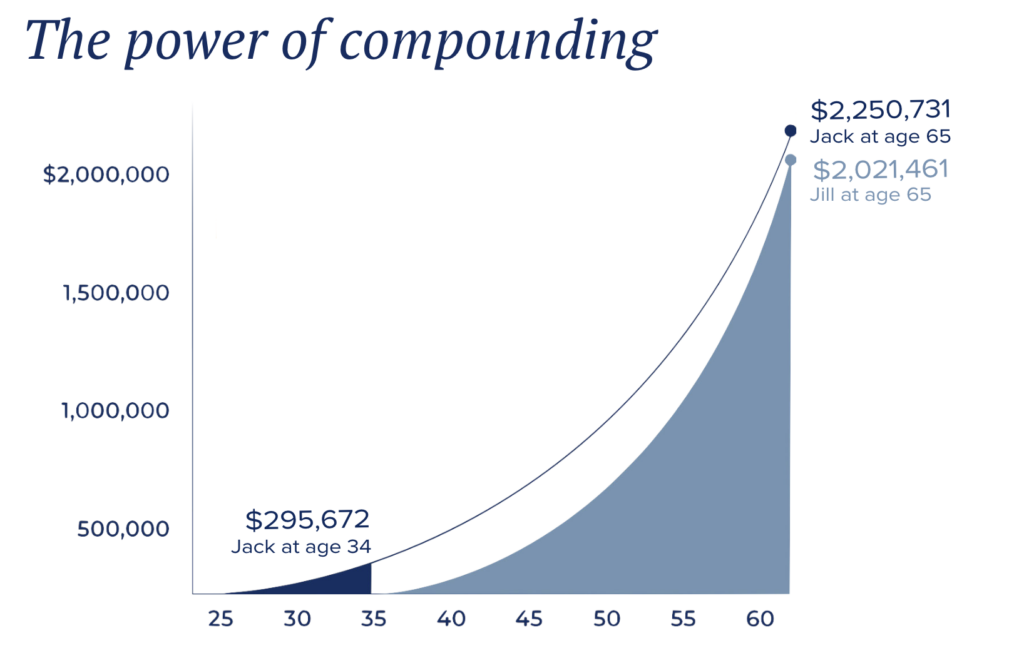

Consider two friends. Jack starts investing at age 25, putting in S$20,000 a year for 10 years, then stops and leaves the money untouched. Jill starts at 35 and invests the same S$20,000 a year for 30 years. Even though Jill contributes S$400,000 more in total, Jack ends up with more, because his money had a decade’s extra head start to compound. Starting early matters more than starting big.

Why compounding frequency also matters

How often interest is added also affects growth. The same rate compounded monthly produces a little more than compounded annually, because each new slice of interest starts earning sooner. The effect is modest over short periods but adds up over decades. Savings products may compound monthly or even daily, while many dividend-paying investments effectively compound when payouts are reinvested as they arrive.

The power of regular investing

A common misconception is that you need a large sum to begin. You do not. Investing a smaller amount consistently still builds wealth through compounding — and it brings its own advantages.

This habit of investing a fixed sum on a regular schedule is known as dollar-cost averaging (DCA). By buying steadily through ups and downs, you pick up more units when prices are low and fewer when prices are high, smoothing out your average cost. It also removes emotion from the decision: instead of trying to time the market, you simply keep going, which helps you avoid panic-selling at the bottom.

Syfe’s auto-invest via eGIRO feature allows you to make recurring contributions to your preferred portfolios, ETFs, or stocks regularly so that you can build your portfolio consistently without breaking a sweat.

Let your earnings be reinvested

It can be tempting to take dividends out and spend them. But reinvesting them is one of the simplest ways to boost compounding: each reinvested payout buys more units, which grow your base, which in turn generates larger future returns.

Doing this manually every quarter is easy to forget. A managed portfolio such as Syfe’s Core Equity100 automatically reinvests your dividends at no extra charge, so your money keeps compounding without you lifting a finger. Pairing automatic reinvestment with scheduled contributions makes the whole process effortless.

How compounding shows up in Singapore

Compounding is not an abstract idea. Singaporeans encounter it across several everyday vehicles:

- CPF. Interest credited to your CPF accounts compounds year after year. As of Q3 2026 (1 July to 30 September 2026), the Ordinary Account earns 2.5% p.a. and the Special, MediSave and Retirement Accounts earn 4% p.a. — a floor the government has extended to 31 December 2026 — with extra interest on the first tiers of your balances. CPF rates are reviewed quarterly and can change.

- Singapore Savings Bonds (SSBs). SSBs use a step-up structure where the rate rises the longer you hold, rewarding patience. The July 2026 issue offered about 1.46% in year one and a 10-year average of about 2.11% p.a. They are government-backed, start from S$500, and can be redeemed in any month. SSB rates are set monthly and move with government bond yields.

- SRS. Investments held in a Supplementary Retirement Scheme (SRS) account can compound while you also enjoy tax benefits on contributions — a useful upside for long-horizon money.

- Equities and S-REITs. Broad market exposure — for example through a globally diversified portfolio or Singapore REITs — lets reinvested dividends and long-term growth compound together. These carry market risk and can fall in value.

One reason compounding matters so much locally is inflation. Money left idle in a low-interest account can lose purchasing power over time; investments that compound above the inflation rate help your savings keep their real value.

When compounding works against you

Compounding is powerful in both directions. On debt — especially credit cards, which can charge high rates and compound on unpaid balances — the same math works against you, and balances can snowball quickly. Clearing high-interest debt before investing is usually the higher-return move, because avoiding a steep compounding cost is a guaranteed saving.

Putting compounding to work

Getting the most from compounding comes down to three habits: start early, invest regularly, and reinvest what you earn. Setting a clear goal helps you stay the course through inevitable market wobbles.

Investors who would rather have this handled for them — with automatic dividend reinvestment and scheduled contributions — often consider a globally diversified, managed portfolio. If a long-term target like building your first S$1 million is on your mind, the sooner you let compounding start working, the less heavy lifting you need to do later.

Conclusion

Albert Einstein once said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

In investing, compounding is the most effective way to let time do the heavy lifting. Understanding how it can work to your benefit can make your investing journey much easier. And with Syfe’s auto-invest feature, you can dollar-cost average your way to financial abundance in the long run.

Frequently asked questions

How is compound interest calculated?

Compound interest uses the formula A = P (1 + r/n)^(n×t), where P is your starting amount, r is the annual rate, n is how many times a year interest is added, and t is the number of years. In plain terms, each period’s interest is added to your balance, and the next period’s interest is calculated on that larger balance.

How long will it take to double my money?

A quick estimate is the Rule of 72: divide 72 by your expected annual return. At 6% a year, money roughly doubles in about 12 years (72 ÷ 6). It is an approximation, not a promise — real returns vary year to year.

Does CPF compound?

Yes. Interest credited to your CPF accounts is added to your balance and itself earns interest in following years. As of Q3 2026, the Ordinary Account earns 2.5% p.a. and the Special, MediSave and Retirement Accounts earn 4% p.a., with extra interest on the first tiers of your balances. CPF rates are reviewed quarterly and can change.

Is it better to invest a lump sum or contribute regularly?

Both can harness compounding. Regular contributions (dollar-cost averaging) suit most people because they build the habit, spread out your entry price, and keep emotion out of the decision. The most important factors are starting early and staying invested.

What is the easiest way to start compounding in Singapore?

Pick a vehicle that reinvests automatically and contributes on a schedule, so growth compounds without manual effort. Many investors use a globally diversified, managed portfolio that reinvests dividends for them. Past performance is not a guide to future returns, and capital is at risk.

Read More:

How Dollar-Cost Averaging Builds Wealth Over Time

How and Where to Invest Your First $100K in Singapore – Your Step-by-Step Guide

The Best Passive Income Investments in Singapore

How To Start Building Your First $1 Million

You must be logged in to post a comment.