US stocks have whipsawed this year amid concerns around rate hikes, recession, inflation, and geopolitical tensions.

If you’ve remained committed to your long-term investment strategy so far, every dip in your portfolio balance can feel like a knife to the heart. You might even be wondering if you should take your hard-earned money out of the market.

We know this period hasn’t been easy, but history tells us that long-term investors will prevail.

Pullbacks are normal

Stocks always move up or down, sometimes due to news headlines or economic developments. Over the long-term however, a company’s fundamentals and business model is what ultimately determines its share price performance.

Investment firm Guggenheim Funds looked at corrections of the S&P 500 since 1946 and found that market declines of 5% to 10% happen about 1.2 times a year. The average time it takes for the S&P 500 to recover from such a dip is one month. Of course, deeper declines do happen too. A drop of 10% to 20% happens about once every 2.5 years, and it takes four months on average to recover.

For long-term investors, the key takeaway is that while declines in the market happen from time to time, these declines occur far less frequently as compared to advances. Additionally, market advances are not only more frequent but also outsized. In other words, the bad days are few, there are more good days, and the good days can be excellent.

It pays to stay invested

With markets so choppy, you may think that pulling out of the market is a “safe” choice. But doing that means you not only realise your losses but also risk missing out on the recovery that follows.

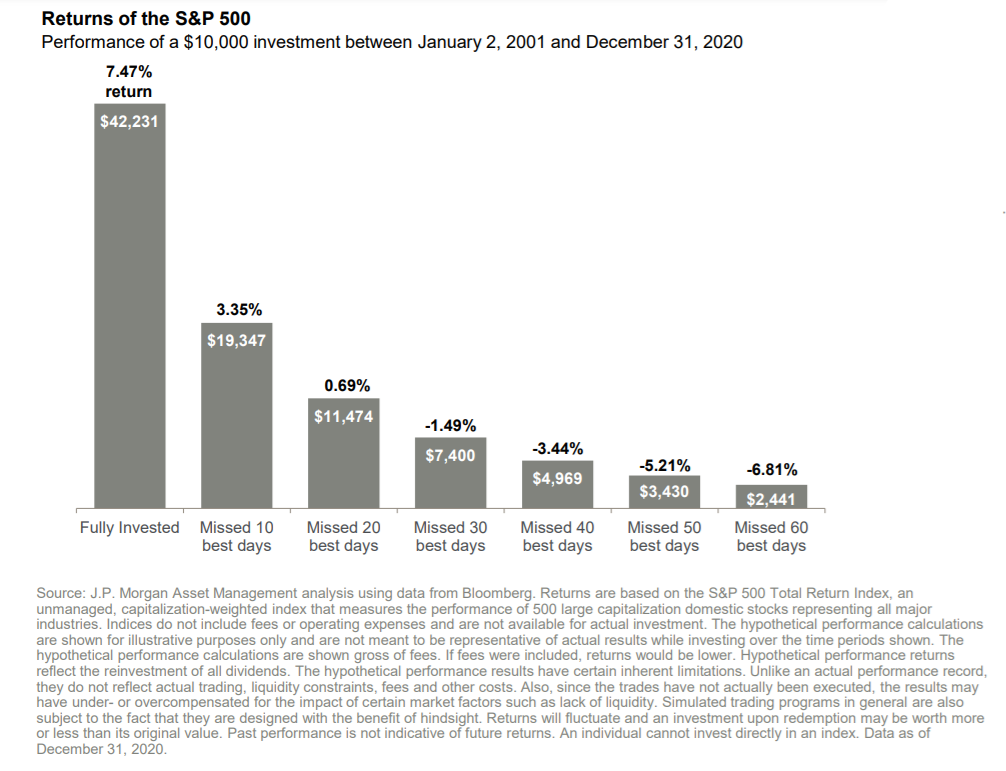

According to research by J.P. Morgan Asset Management, missing just 10 of the stock market’s best days can cut your overall return by more than 50%.

Their analysis also found that seven of the best 10 days occurred within two weeks of the 10 worst days. Case in point: On March 13, 2020, the S&P 500 rose more than 9%, making that Friday the index’s best day since 2008 (as of 13 March 2020). Underscoring just how difficult it is to time the market, the second worst day of 2020 happened to be March 12, 2020.

Pullbacks can be opportunities

You’ve often heard that the ideal way to invest is to buy low and sell high. Market pullbacks and corrections can be a chance to invest in high-quality stocks at more attractive prices.

But what if the market falls further, you might ask. The truth is, nobody knows what is going to happen next. The market may rally from this point on, or it may not.

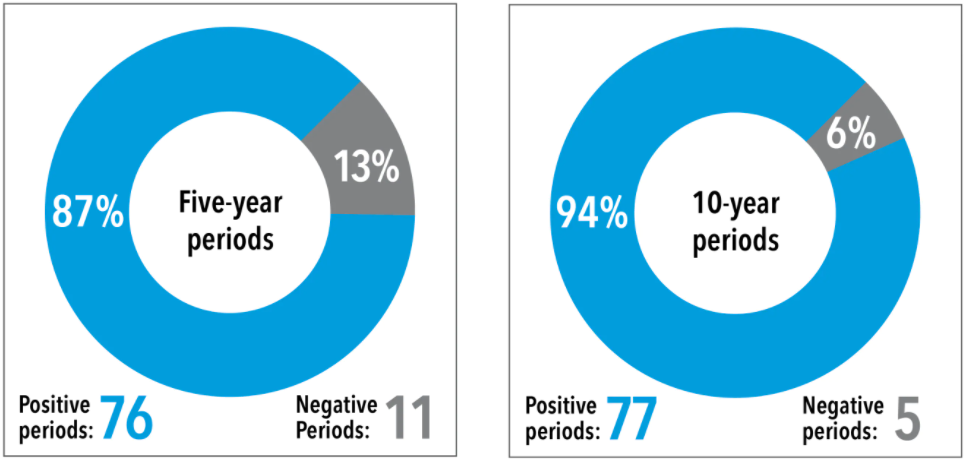

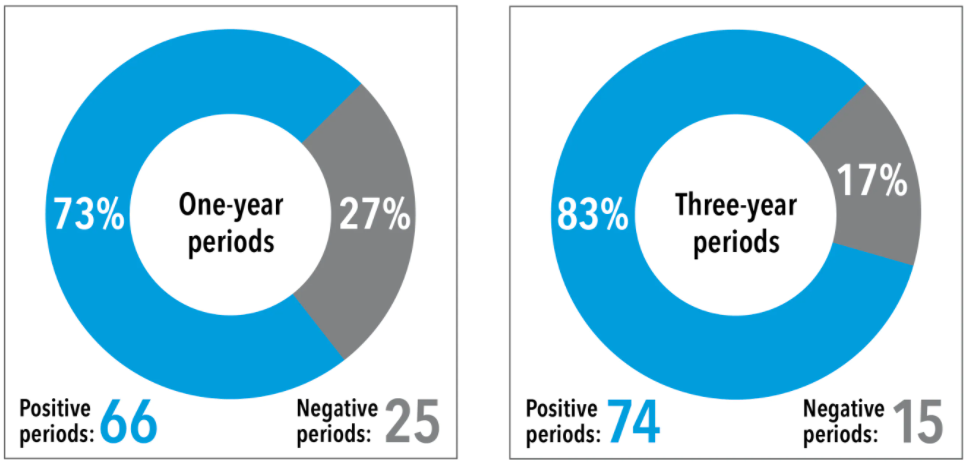

What we do know is that, the longer you stay invested, the better your return prospects are. According to research done by Capital Group, the 10-year returns for the S&P 500 have been negative just 6% of the time since 1929.

Though past performance is not a guide to the future, the longer you stay invested, the greater your chances of a positive outcome. In fact, if you can hold your investments for a 20-year period, you would have historically come out ahead.

Try dollar cost averaging

Stocks don’t go up forever. Smart investors know that market ups and downs are just part and parcel of investing.

That’s why it may make sense to adopt a strategy known as dollar cost averaging. By investing a certain sum of money at regular intervals – say $1,000 each month – you average out the cost of all your investments while eliminating some of the risky guesswork involved in trying to time the market.

Dollar cost averaging may also be ideal for investors who are uncomfortable with the thought of investing a large amount of money when they are not sure which direction the market may be heading. The strategy helps you capitalise on lower prices now while avoiding the risk of buying all at once ahead of another market drop.

You must be logged in to post a comment.