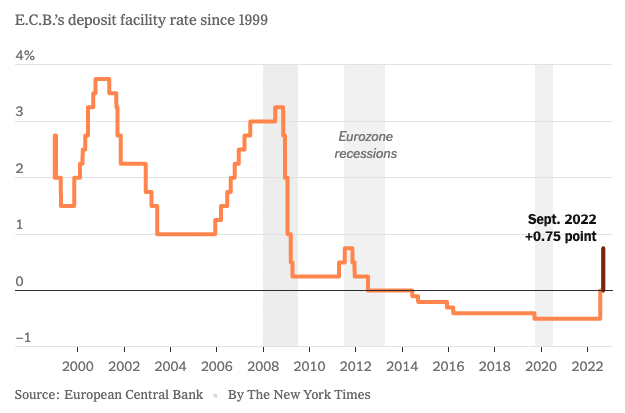

Forcefully

The ECB raised interest rates by 0.75% this week, the biggest move since 1999. Similar to the Fed, policymakers in Europe are trying to bring down record high inflation (9.1%), at the expense of economic growth. Further increases are expected and future decisions remain “data-dependent”.

Across the pond, Chair Powell took on a hawkish tone in his last public comments before the FOMC meeting later this month. This did not come as a surprise and S&P 500 ended the week almost 2% higher.

Notable quotes: “History cautions strongly against prematurely loosening policy” and “Restoring price stability will take some time and requires using [the] tools forcefully to bring demand and supply into better balance”.

Market expectations point to another 0.75% increase for the upcoming FOMC meeting, putting the fed funds rate at 3.0-3.25%.

Locking In

Singaporeans stood in line to lock in the highest promotional deposit rates in 24 years – that’s a whole generation! We explore locking funds in a fixed deposit vs. cash management solutions that move along with rate hikes here.

Taking Profit

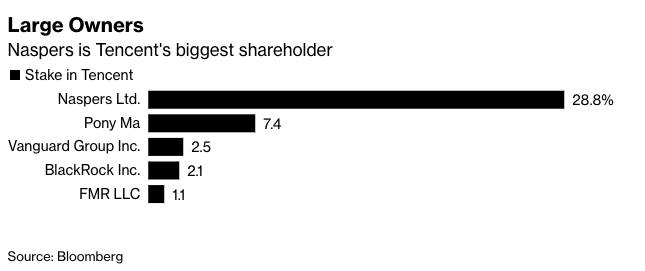

Prosus NV (Naspers Ltd), Tencent’s largest shareholder, continues on its path to sell $7.6bn worth of Tencent Holdings Ltd. stock in order to fund their own share buyback scheme. This follows in SoftBank’s footsteps to offload Alibaba and Warren Buffett’s move to take some profit on BYD, China’s largest EV maker.

Stake reductions are generally seen as negative – since the announcement in June, Tencent’s share price fell before recovering in August.

We will be watching the Chinese Communist Party congress set to take place next month where we could see significant reshuffles of the top economic positions. President Joe Biden is holding back on a decision to remove Trump-era tariffs that might shave 1% off CPI in a best case scenario, even though there is no consensus on how effective this would be. Making a decision before either US midterm elections and CCP congress carries a certain amount of political risk that President Biden is unlikely to take before November.

Early or late?

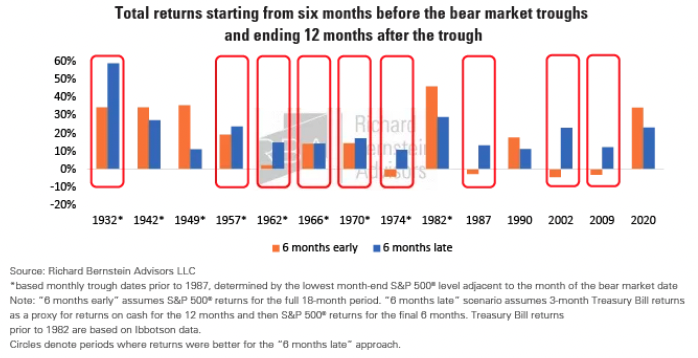

A few weeks ago, we wrote that it was too soon to tell if the rally we saw in July was going to be persistent. According to RBA Advisors, in seven of the last ten bear markets going back to the 1960s, it has been better to be late than early as this reduces downside potential and gives one more time to assess incoming fundamental data.

However, if we look at the bear markets where the Fed has been more involved (2009 and 2020), we get a mixed picture. Investors who were early in 2020 did better while investors who were early in 2009 did worse.

History tells us that markets do eventually recover and investors who adopt a dollar cost averaging (DCA) strategy do better over the long run.

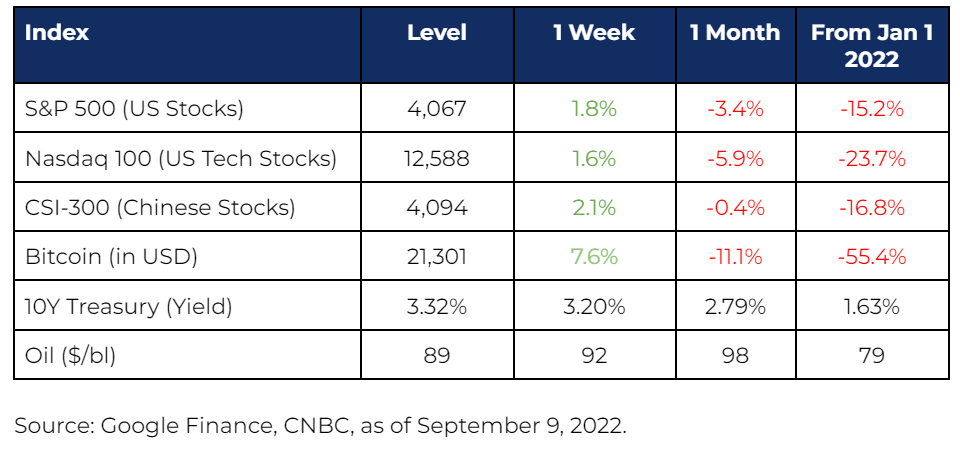

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.