As we celebrate the Chinese New Year, symbolised by the energetic “fire horse” in the Chinese zodiac, we identify the key themes that could keep the Chinese stock market racing ahead – and potentially fire up your portfolio this year.

Why China, Why Now? From “Uninvestable” to a “Very Chinese Time”

Chinese equities have turned a corner. From being “uninvestable” in the eyes of bearish foreign investors, to one of the best-performing markets last year (MSCI China was up more than 30%), China’s stock market has rallied on policy support and breakthroughs in artificial intelligence. Authorities and analysts are talking about a “slow bull” market that could last several years.

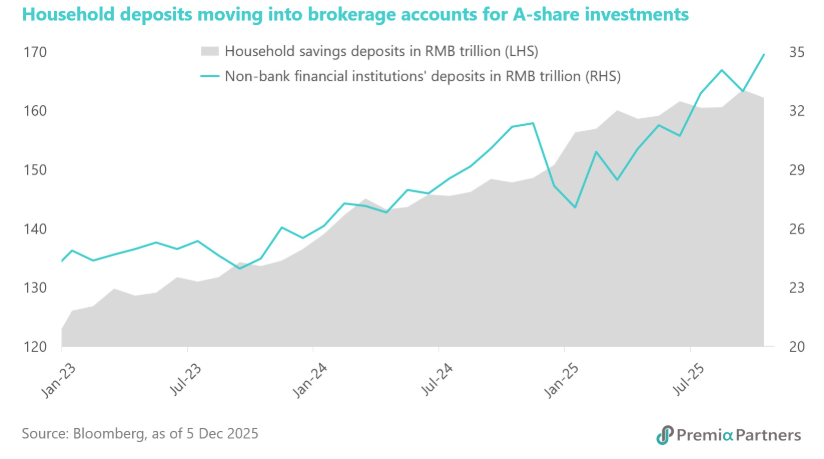

There are signs that cash-rich Chinese households are mobilising more of their capital into the stock market, helped by interest rate cuts making deposits less attractive. Money supply data is reaffirming this trend (with narrowing M1-M2 growth) and pointing to recovering confidence among domestic investors.

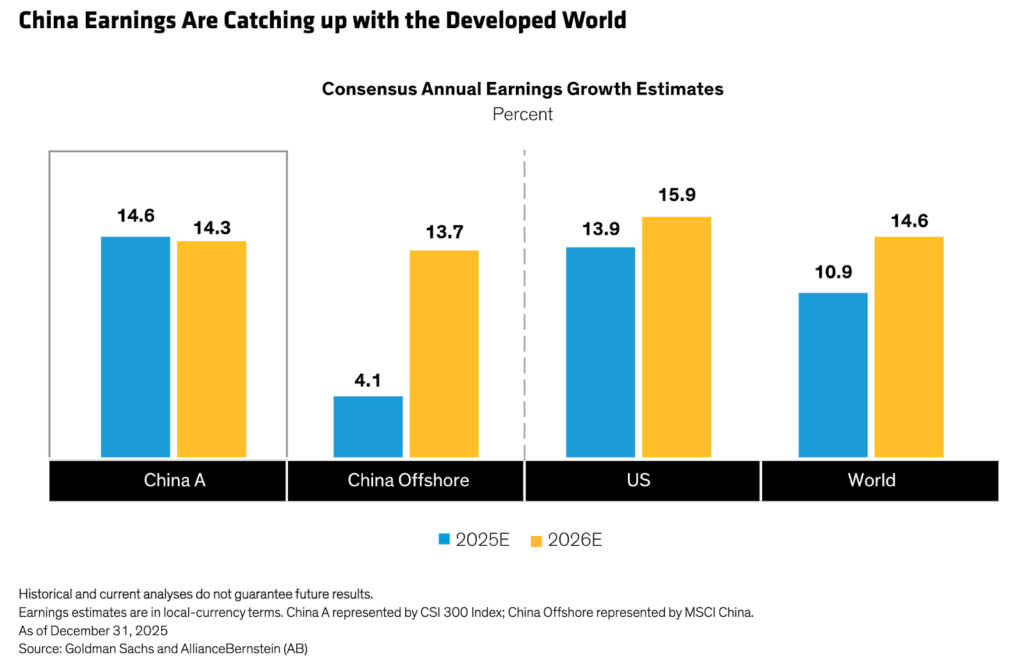

Policy support will continue to feature. State funds have bought shares to support the market during periods of weakness. Earnings momentum has picked up as the growth outlook improves, setting up China on course to catch up with other major markets.

In our Core Portfolios at Syfe, we have been “overweight” on China, meaning we put more money in Chinese stocks than our benchmarks recommend, which has contributed to performance over the past few years. Syfe users can also access some of the themes below through the China Growth Portfolio (powered by KraneShares, iShares, and Global X).

Many global investors, while still “underweight”, could move in our direction as they seek to diversify from concentrated markets this year. Perhaps, just like the recent Gen Z trend romanticising Chinese culture, they, too, are about to enter “very Chinese time” in their portfolio.

Theme 1: “Anti-Involution” Revolution

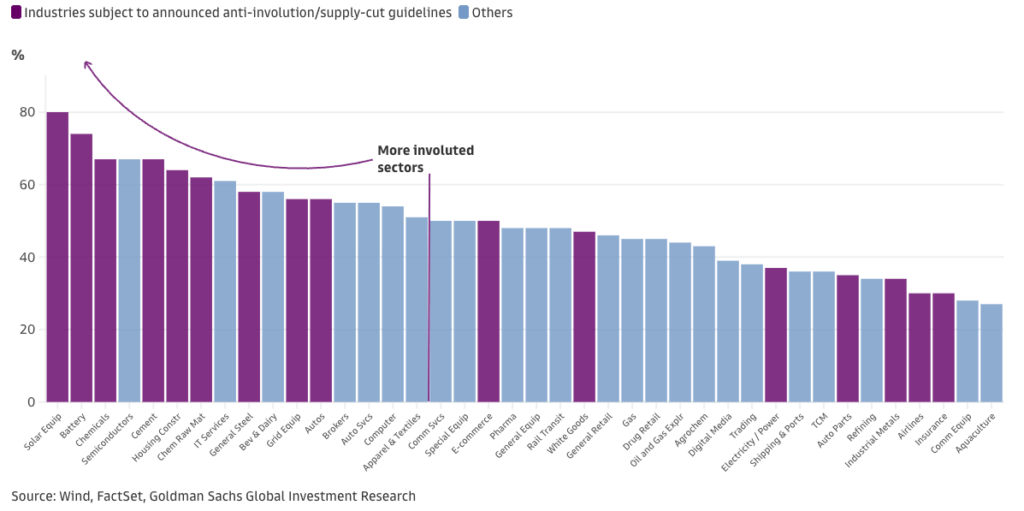

One long-standing challenge in China is excessive capacity. Simply put, Chinese companies produced too much for the market to consume. What followed was a “race to the bottom” with ever-lower prices, contributing to deflation. This combination, coined “involution”, has put pressure on corporate earnings in recent years, which have grown slower than nominal GDP, according to research by Goldman Sachs.

Policymakers have made it a priority to put a stop to it, aware of the dangers deflation poses (they needn’t look far, with Japan only recently recovering from it). Pivoting away from “growth at all costs”, companies are encouraged to cull supply and focus on returns on investment, especially in sectors with years of oversupply, such as solar energy and batteries. Several cyclical sectors – cement, solar, and chemicals – where policymakers are focusing their “anti-involution” efforts, are still considered cheap by analysts at Goldman Sachs.

Theme 2: The “Basket of Tomorrow”

Amid trade restrictions on sensitive technology, China has ramped up efforts to make its economy self-reliant. This shift has put technology companies at the centrestage of the country’s economic blueprint (the “15th Five-Year Plan”). This has implications beyond China.

Chinese tech is going global. Tech companies in China have opted for the “open source” model, which shares its underlying code to hasten development, which differs from the more controlled and polished “closed source” approach by the likes of OpenAI and Google.

Chinese firms are powering 30% of all “open source” AI usage, according to research by OpenRouter, an AI model aggregator, and venture capital firm Andreessen Horowitz. The report noted that “China has emerged as a major force, not only through domestic consumption but also by producing globally competitive models.”

The country is not just producing new models, but a new cohort of listed companies. AI-related businesses have dominated listings in Hong Kong, producing the busiest January ever for IPOs on the exchange there. Companies that went public came from across the AI value chain, from modelling and training to robotics and intelligent security.

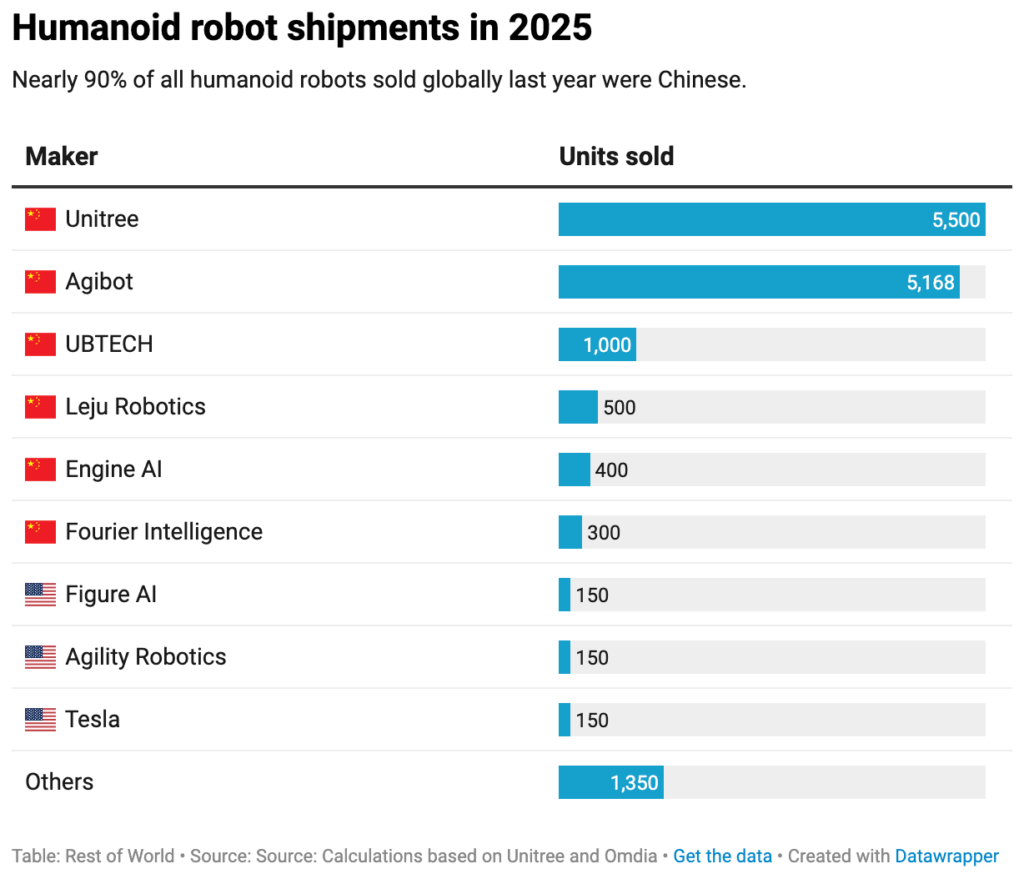

What’s clear is that China’s AI beneficiaries – what we’re calling the “basket of tomorrow” – have broadened meaningfully beyond chipmakers. Many are working on real-world applications made possible by AI, for example, in autonomous driving and humanoids.

It’s estimated that the Chinese embodied AI robot market size could reach US$77 billion in 2030. The sector is rapidly moving from concept to commercial reality. Unitree, perhaps the most recognised robotics name in China, is building a $124 million factory targeting over $140 million of annual revenues.

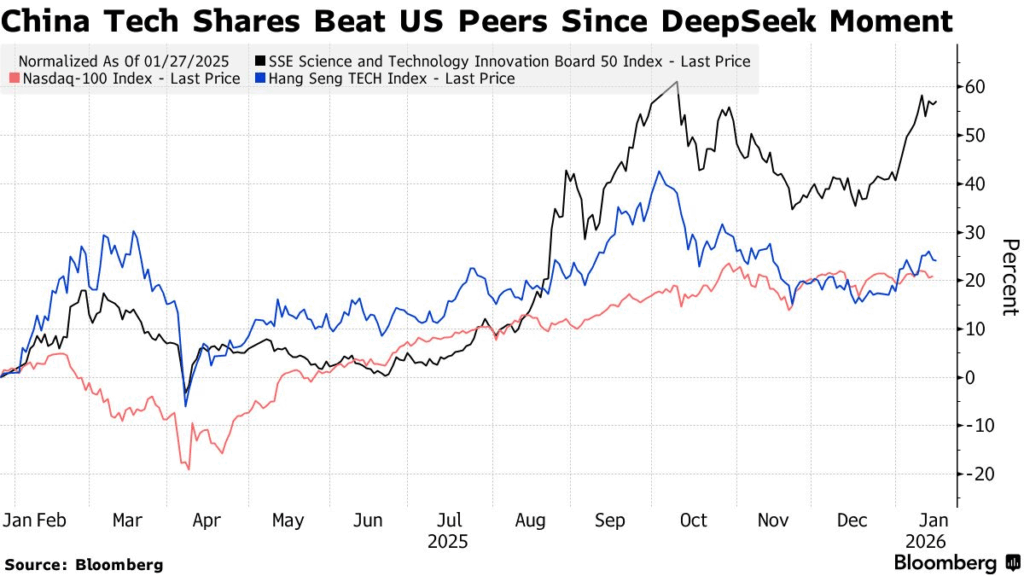

That also means investors will have to cast a wider net, however. The latest leg of the rally has not come from the “big tech” basket, the Hang Seng Tech Index, which has been weighed on by regulatory scrutiny. It has instead been powered by the “STAR” 50 index, which hosts newer, nimbler tech firms with a focus on “hard” tech. ETFs tracking both indices form parts of Syfe’s China Growth Portfolio.

With China’s AI capital expenditure projected to reach USD 330 billion by 2030, the “basket of tomorrow” holds plenty of promise. For our clients in Singapore, there is an opportunity to catch a glimpse of the future on 26 February 2026 at the Syfe Market Outlook 2026 event in Marina Bay Sands, where we will be showcasing Singapore’s first “Investment Humanoid”.

Sign up here.

Theme 3: Finding Value in “Boring” Companies

Less exciting but equally important is rising “shareholder return” in China. Regulators have been encouraging cash-rich companies to return more of their “lazy” capital – unused cash sitting on their balance sheets – to shareholders.

This theme is in vogue for good reasons. China is shifting its focus from the velocity to the quality of economic growth. In some industries, leading companies’ earnings growth outlook has become less appealing, as they go from seizing market share to defending it. Shareholders would only want to stick with them if the “total return” (capital appreciation, plus buybacks and dividends) is competitive enough with up-and-coming growth stocks.

Some analysts see this as a “culture shift”. The search for high-dividend stocks, in particular, has been egged on by falling Chinese bond yields, which have fallen as policymakers suppressed financing costs to boost growth. BBB-rated (the highest yielding “investment grade) corporate bond yields are now lower than blue-chip dividend yields.

This is a multi-year story. Regulators have been encouraging shareholder returns to rise, in a bid to attract long-term capital to equities. We have seen this play out in Japan and Korea. Already, there are meaningful pick-ups in “payout” ratios (proportion of the company’s earnings paid to shareholders) and buybacks among state-owned enterprises in China.

More “new economy” companies will join the wave as they become the incumbents of their industries. Baidu, China’s Google equivalent, paid dividends for the first time in February in its two decades as a publicly traded company.

Chart compiled by Allianz Global Investors.

A Final Word: Beware Overheating the “Fire Horse”

In the Chinese zodiac, the dynamism of the “fire horse” could also lead to exacerbation. Likewise, extreme optimism could push share prices too fast, too far beyond their fair values, especially in a retail-driven stock market like China’s. Regulators have stamped out speculation when trading got too hot, even at the cost of hurting market performance. This is why a “slow bull” market remains more probable than a euphoric run-up in Chinese equities this year.

Many analysts still worry about the property market, which is responsible for plenty of GDP growth and has yet to find a floor. But policy is heading in the right direction, with more relaxation on home purchases trickling through.

What’s clear is that policymakers are not about to unleash the “fire horse” and reflate the property market, the overheating of which was the source of so much trouble. This is part of a broader rebalancing towards technology-led growth, which is constructive to sustaining long-term growth.

You must be logged in to post a comment.