As part of our periodic rebalancing for Core Equity100, we will be updating our allocation for the portfolio over the next few days. Once the rebalancing is complete, the equity component of Core portfolios will track the allocation of Core Equity100 as well.

Key updates to Syfe Core Equity100

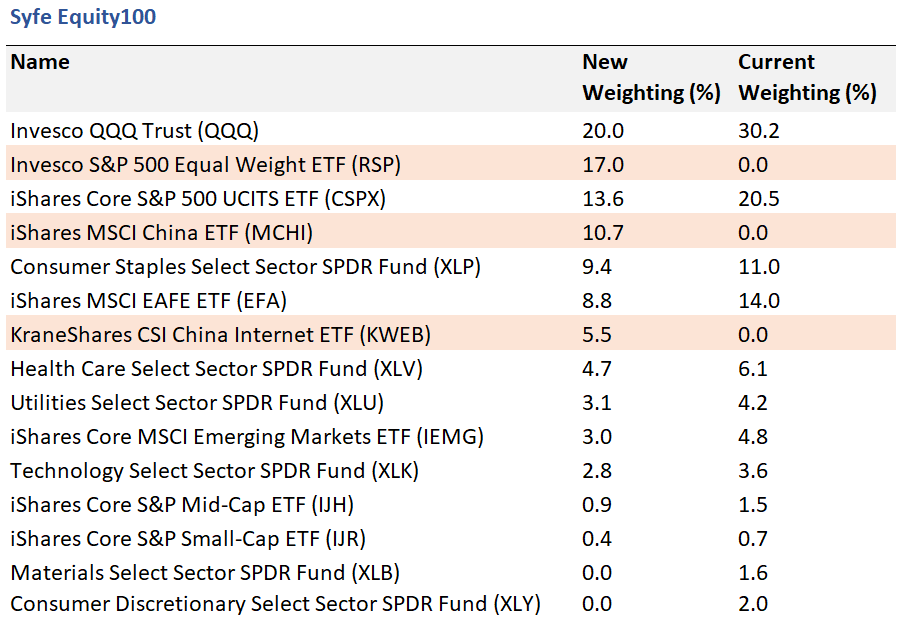

Additions

- iShares MSCI China ETF (MCHI)

- KraneShares CSI China Internet ETF (KWEB)

- Invesco S&P 500 Equal Weight ETF (RSP)

New constituent list

Frequently Asked Questions

Why is Core Equity100 being rebalanced?

Core Equity100 is rebalanced twice a year to maintain portfolio efficiency and to continue delivering the best expected risk-adjusted returns for you. Such periodic rebalancing is necessary because of market movements and factor style drifts.

Why are the MCHI and KWEB ETFs being added?

These ETFs are being included to provide an enhanced exposure to China and Chinese tech stocks. We selected these sector and geographical factors using econometric and graphical screens, then validated their selection by back-testing these factors using our point-in-time algorithms.

With the Chinese market outperforming since last year, we believe the China and Chinese tech factors will not only provide additional diversification benefits but will continue to outperform going forward.

Why is the RSP ETF being added?

RSP is an equal weighted ETF that tracks the S&P 500 index. This means that every stock held by the ETF has the same weight, regardless of how large or small the company is. Therefore RSP adds a Size factor tilt biased towards small-cap stocks. At the same time, RSP also simultaneously adds a Value (Vs. Growth) factor tilt.

Our analysis indicates that the large-cap factor, and to a lesser extent the Growth factor, might no longer provide optimal risk-adjusted returns for Core Equity100 going forward. As such, the addition of RSP moderates our factor tilts towards the large-cap and Growth factors, respectively, albeit to different degrees.

What are the factor tilts after this rebalancing?

The Core Equity100 portfolio was constructed with factor tilts towards growth, large-cap and low volatility.

Following this rebalancing, the portfolio will continue to have a low volatility tilt in addition to a geographical tilt towards China, and a moderated tilt towards growth.

We have chosen to moderate – but not remove – our growth tilt due to the relative factor volatility between growth and value, and the fundamental shift to greater technology adoption globally, accelerated by the Covid-19 pandemic.