The Week Ahead

- China Q1 GDP (YOY)

Thought Of The Week

$2.25 Trillion Infrastructure Plan, Taxing the World

U.S President Joe Biden promoted his $2.25 trillion infrastructure plan in a White House speech on Wednesday. It was not just a matter of replacing lead water pipes in communities and installing charging stations for electric vehicles, but a wide programme of economic reform aimed at education, healthcare and climate change.

While Biden is open to negotiating with lawmakers on specifics of the plan, he expressed his unwillingness to inaction. With the risk of adding too much momentum to an economy (1 month after a $1.9 trillion fiscal stimulus package funded by borrowing), two features of the Biden plan commend it. One is its long view: The funds will be utilized over 8 years which makes the cost less daunting while preventing an overheated economy. Second, it addresses the funding with a proposal to raise U.S corporate tax rate to 28% and implement a new global corporate tax agreement. That compares with the current 21% rate and 35% rate before the 2017 tax cuts.

However, many challenges still lie ahead for the minimum tax proposal such as the long-standing disagreement over digital taxation. U.S markets closed higher for the week while Asia markets were mostly in the negative range.

Diverging Recoveries

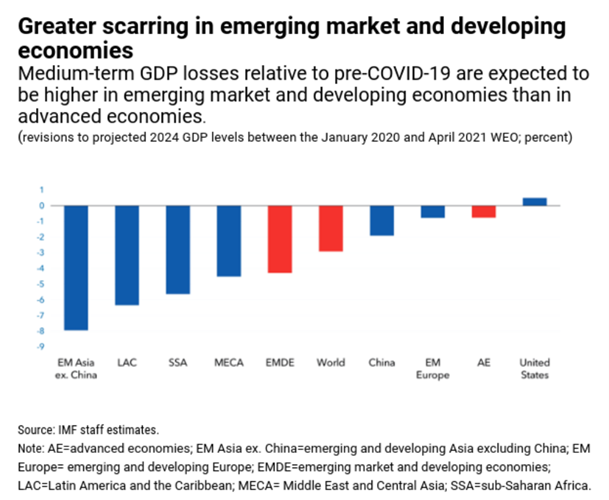

IMF raised the forecast for a stronger global recovery in its latest World Economic Outlook, with growth projected to be 6% this year, a 0.5% increase from its January forecast. The upgrade is due to better outlook for advanced economies, particularly for the United States. Among developing economies, China is projected to grow at 8.4% in 2021, contributing more than one-fifth of the total increase in the world’s GDP in the five years through 2026. Other contributing economies include India, Japan and Germany.

IMF also warned that despite the better forecast, growth may be unevenly spread which creates wider income gaps especially in emerging markets compared to pre-pandemic expectations. Young and lower-skilled workers are the ones bearing the most brunt since many of the jobs lost are unlikely to return due to the acceleration in digitalization and automation during this pandemic. Policymakers will need to continue to support their economies and it will be more difficult for economies with limited fiscal space and higher debt levels.

Other highlights include green infrastructure investment to help mitigate climate change, digital infrastructure investment to boost productive capacity and strengthening social assistance to address rising inequality.

Chart Of The Week

Important Information and Disclosure

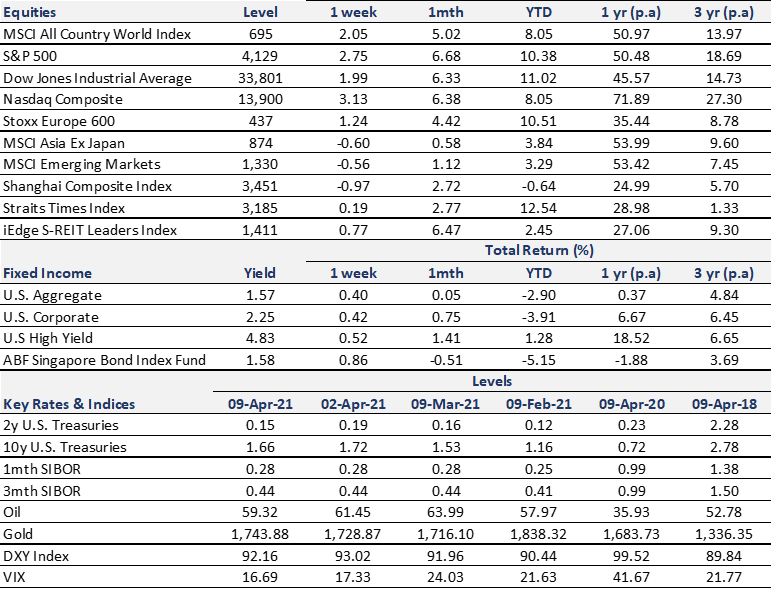

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.