Note: The projected return for Syfe Cash+ has been revised to 3.0% p.a. in December 2022.

Amid the current environment of persistently low interest rates, we are revising the projected return of our Syfe Cash+ portfolio from 1.75% to 1.5% p.a. for the second quarter of 2021.

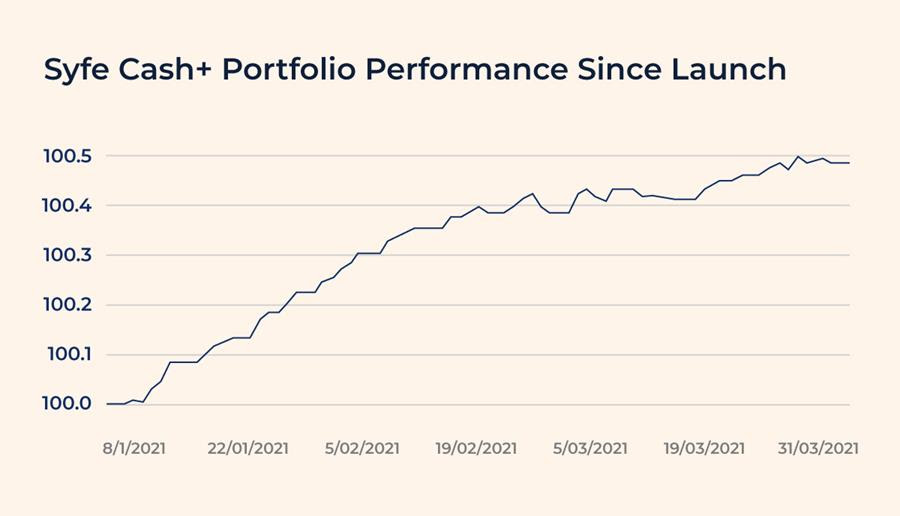

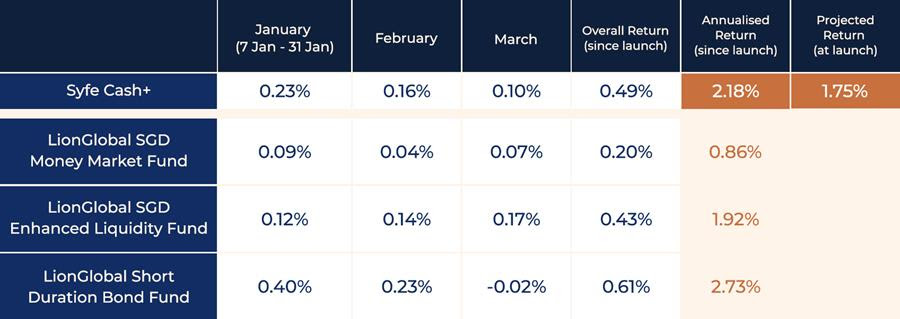

Since its launch on 7 January 2021, our Cash+ portfolio has delivered actual net returns higher than originally projected. Our annualised return since launch was 2.18%, while our projected return at launch was 1.75% p.a.

However, given that interest rates and yields on short-term bonds are expected to remain low in the months ahead, now is the time to make an adjustment to our projected return.

If and when the interest rate environment changes, you can be assured we will revise our projected return accordingly.

How has Syfe Cash+ performed in the first quarter?

The annualised return of Cash+ stands at 2.18% as at 31 March. This is higher than the projected return of 1.75% p.a. that we shared with our clients when Cash+ was launched.

During the first quarter of 2021, many local banks cut interest rates yet again on their savings accounts, in line with the low interest rate environment.

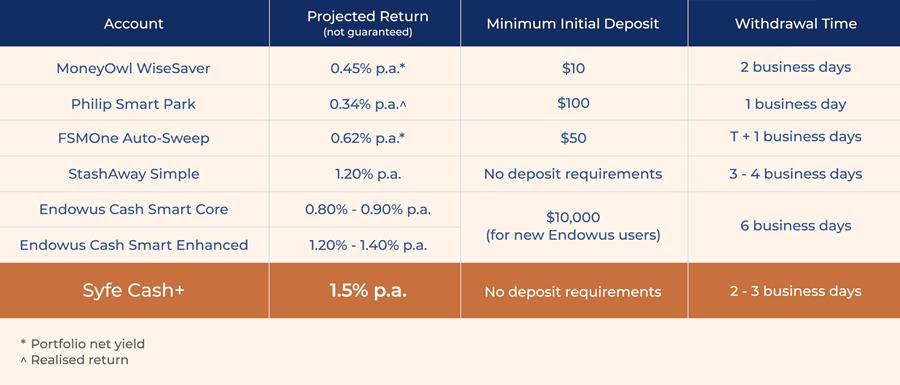

Cash+ provides an alternative to traditional bank savings accounts. With no lock-in periods, zero fees, and free withdrawals at any time, it has quickly become one of our most popular portfolios.

As of now, one in four Syfe clients has a Cash+ portfolio, and we expect that number to grow even further as people seek ways to earn more on their cash in this low interest rate environment.

Understanding how Cash+ works

Given the strong interest in our Cash+ portfolio, this quarterly update also serves as a recap of how Cash+ works.

Cash+ is invested in a combination of money market, enhanced liquidity and short-term bond funds managed by Lion Global Investors. The underlying holdings in these funds are low-risk assets such as Singapore and international government bonds, commercial bills and high-quality corporate bonds.

The portfolio’s daily value is updated based on the Net Asset Value (NAV) of the three funds, which is driven by the performance of the underlying holdings.

As with all investments, the prices of bonds may fluctuate over time, although you can expect price movements to be more muted due to the low-risk nature of bonds relative to other asset classes.

It is important to realise that although Cash+ is considered a low-risk investment, it is not risk-free. To earn an enhanced return above bank deposit rates in this low interest rate environment, investors have to take on some interest rate and credit risk. Let’s explore what these risks actually mean.

Interest rate risk, explained

Interest rate risk is the risk that comes with buying bonds with some period of time left until maturity.

Interest rate fluctuations impact the market prices of bonds, causing investors to experience mark-to-market or realised gains and losses. When interest rates increase, bond prices decrease, and vice versa.

An individual bond or overall portfolio’s sensitivity to interest rates is known as its “duration”. Typically, bonds with shorter maturity have less interest rate risk than bonds with a longer maturity.

Governments and companies issue bonds with different maturities for their own capital management. You often hear references to the “10-year US Treasury Bond”, but the US Treasury issues bonds with a broad range of maturities, from short term out to 30-years.

Short-term and long-term interest rates are driven by different factors:

Short-term rates. These are primarily influenced by policy, as central banks seek to stimulate or slow down the economy by targeting a particular borrowing rate. Currently, short-term rates in the US are anchored by the Federal Reserve setting overnight interest rates at near zero.

Central banks globally, including in Singapore, are typically anchored to the US in setting short-term rates. Right now, the expectation is that short-term interest rates will remain at or close to zero for an extended period.

Long-term rates. These are more market-driven, being influenced by several factors, most notably changes to inflation expectations. In recent months, we have seen an increase in long-term interest rates as many investors expect the economic recovery to eventually create inflationary pressures.

Since Cash+ invests in short maturity bonds with modest amounts of interest rate risk, the recent increases in long-term rates have had only a minor impact on returns.

In fact, despite the move up in long-term rates, some short-term interest rates have actually contracted further in recent months, which has contributed to the reduction in the projected return for Cash+.

Credit risk, explained

Credit risk is the risk that the government or company that issues the bond will not be able to pay back the principal, in other words that they might “default” on the bond. Investors would naturally expect a higher return on bonds that are considered more risky.

Credit risk is assessed by rating agencies using a “credit rating”: you may have heard of AAA as the highest rating, for example.

Government bonds issued in their own currency are considered risk-free since the government also controls the supply of that currency.

Investors can earn a modest increase in returns by buying bonds that are still highly rated, but slightly riskier than government bonds. An example is a bond issued by Singapore Airlines, which is majority owned by the government but is still considered to have a modest amount of credit risk and therefore a slightly higher yield than equivalent-maturity government bonds.

Investor’s perception of credit risk changes over time. In periods of increased volatility, bonds with a high level of credit risk (such as high yield bonds) will typically sell-off together with equities and other risky assets.

In recent months as investors have become more positive about the economic recovery, the additional return (or “spread”) demanded by investors for riskier bonds has decreased.

Bonds with a very low level of credit risk, such as those held by Cash+, are mostly insulated from these types of moves. Having said that, recent changes in credit spreads have had a modest impact on the downward adjustment of the projected return.

Balancing risk and reward

At Syfe, we have constructed Cash+ with underlying funds that take a modest amount of interest rate and credit risk in order to provide an enhanced return above bank deposit rates.

This allows investors who have a slightly longer time horizon (3-6 months and longer) to capture a yield premium.

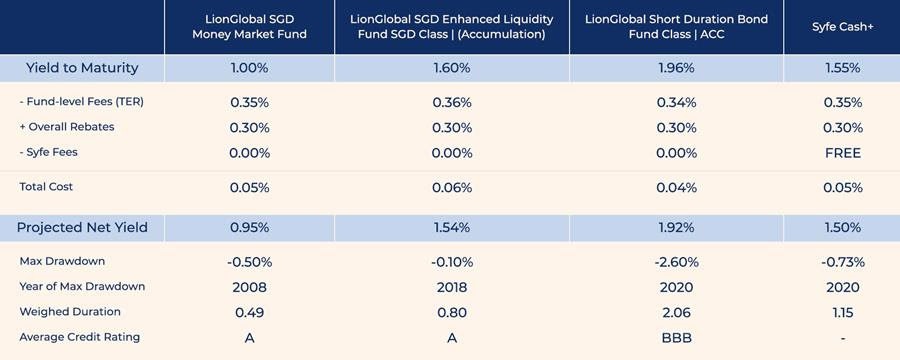

The average weighted duration for the Cash+ portfolio is currently 1.15 years, and the average credit rating is around A-.

This means that although there may be modest fluctuations in the daily returns of Cash+ during periods of volatility, periods of sustained negative performance should be rare.

As such, the chances of permanent capital loss are low, given that the underlying investments of Cash+ are mostly high quality government and corporate bonds with low levels of interest rate risk and credit risk.

Between launch and 31 March, there were 15 days where the daily return was negative. In all but one of these cases, the negative return was offset by positive returns within three days, and in one case the total return was positive again within two weeks.

Why we are revising our projected return

While longer term interest rates have increased, short-term rates have continued to remain low and, in some cases, have reduced further in recent months.

In addition, the yield premium that can be earned by taking modest credit risk has continued to contract as the economic recovery has advanced.

In light of these changes in the market environment, we are adjusting our projected return for Syfe Cash+ to 1.5% p.a. in the coming quarter.

Nothing has or is changing in how Syfe allocates Cash+ funds or how Lion Global manages the underlying funds.

Although our prudent revision of the projected return comes amid the current environment of persistently low interest rates, the adjusted return is still attractive compared to most bank savings or fixed deposit options in Singapore.

Cash+ also offers one of the highest projected returns for cash management solutions in the market.

Looking ahead

Syfe Cash+ has exceeded expectations since launch, delivering an annualised net return of 2.18% compared to the projected return of 1.75% p.a.

Although we retain the discretion to optimize the fund allocation to deliver the best possible projected return in a given interest rate environment, we believe Syfe Cash+ strikes the right balance between enhanced return and risk, in order to help you grow your cash.

You must be logged in to post a comment.