2024 started off on a high note for both the US economy and developed market equities. However, with geopolitical tensions and potential delays in rate cuts, volatility has reemerged in recent weeks. Given the market uncertainty, investors are grappling with several key questions regarding the current market conditions. Ritesh Ganeriwal, our Managing Director of Investment & Advisory, offers his insights and discusses the potential impact on your investments.

A Broadening Equity Rally – Q1 Market Review

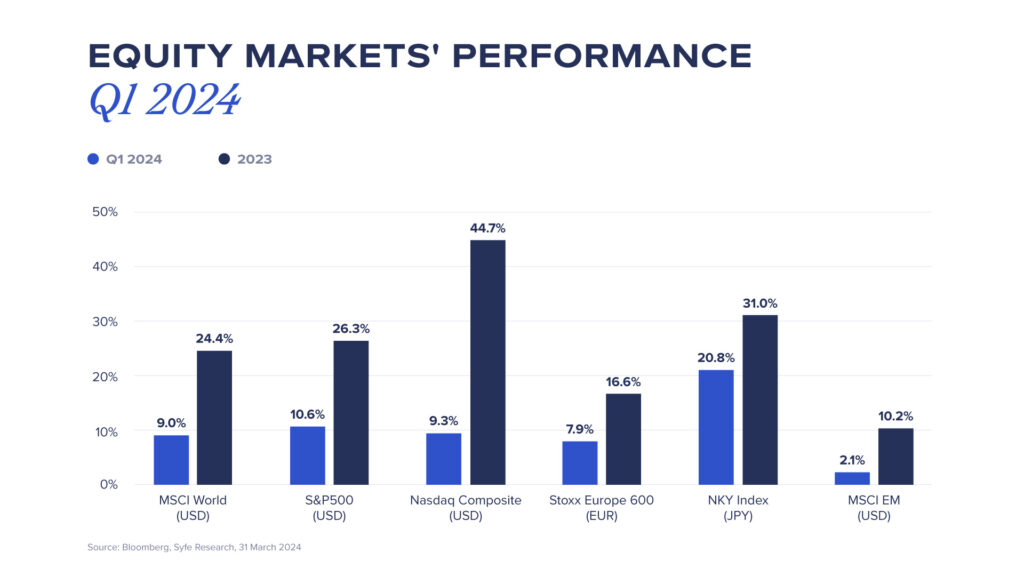

After a strong finish in 2023, global equities continued their momentum into the first quarter of 2024. Global equities gained +9.0% in Q1, following a +24.4% increase in 2023. The S&P 500 index returned +10.6%, posting its best first quarter since 2019. It marked another quarter that the US economy has defied expectation, supported by strong consumer spending and robust labour markets.

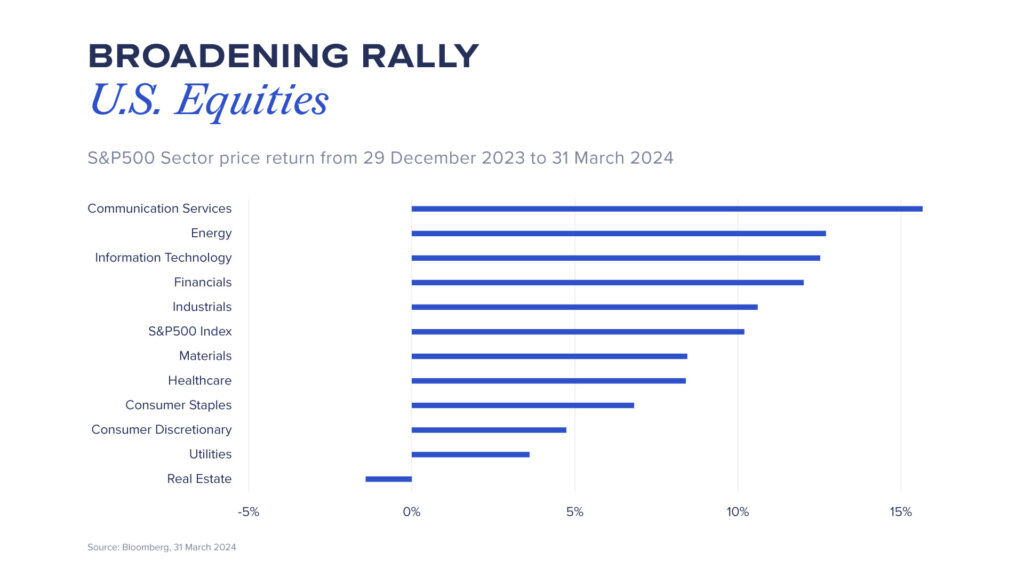

One key observation we have is that this year’s equity rally has finally broadened to include other sectors, as we forecasted in the Syfe Investment Outlook 2024 in January. While the tech sector continues to lead, other value-oriented sectors such as financials, energy, and industrials have also joined in. This broadening of the equity rally indicates a healthier, more balanced market environment.

All Eyes on Inflation

On the rates front, all eyes are now on inflation. Core inflation rose for the third consecutive month in March, with a 3.8% year-on-year increase, sparking concerns that inflation may be more persistent than originally expected.

Market now anticipates only two rate cuts for the year, down from five at the start of year. This resulted in the US 10-year Treasury yield jumping from 3.9% in January to 4.6% now.

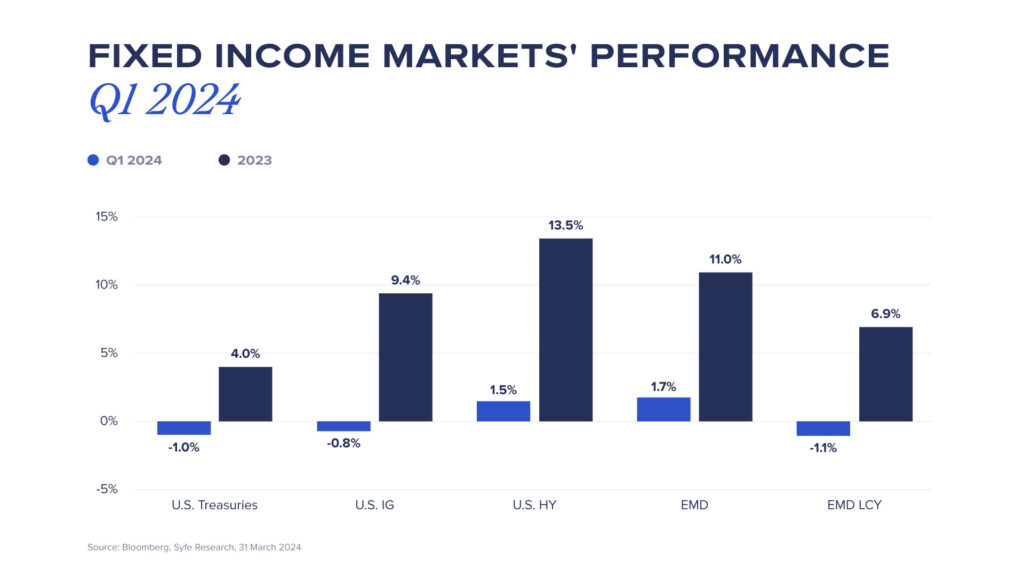

The increase in bond yields has negatively impacted their returns in the short term. US high yield bonds returned +1.5%, while US investment grade bonds and Treasuries delivered negative returns in Q1.

Top 3 Questions on Investors’ Minds

Heading into the second quarter, investors are grappling with questions about the Fed’s policies, the sustainability of the equity rally, and geopolitical risks. We’ve identified the top concerns and provide insights to navigate these issues.

Q1: What would happen to bonds if the Fed does not cut interest rates this year?

- We believe that while the timeline for rate cuts has been delayed, the bar for the Fed to hike rates remains high.

- And even with the delay in rate cuts, bond prices may not suffer greatly, thanks to robust underlying bond yields. Currently, yields are at 15-year highs, presenting an attractive entry point for investors.

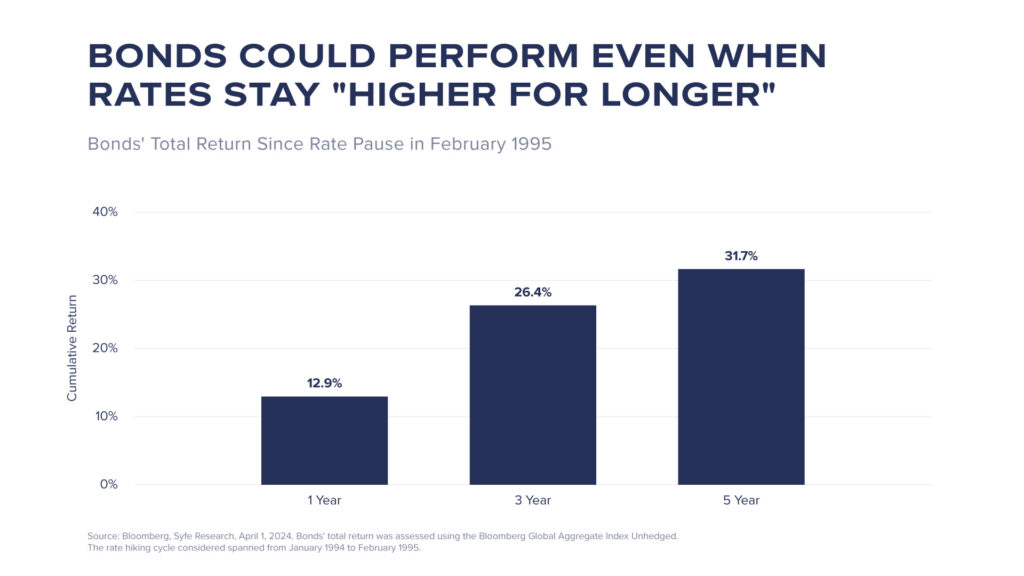

- Looking at historical precedents, bonds could still perform even when rates stayed “higher for longer”. In 1995, after pausing rate hikes in February of that year, the central bank maintained the Fed Funds rate “higher for longer” until the end of 1998. During this period, bonds delivered a total return of 26.4% over three years and 31.7% over five years following the rate pause.

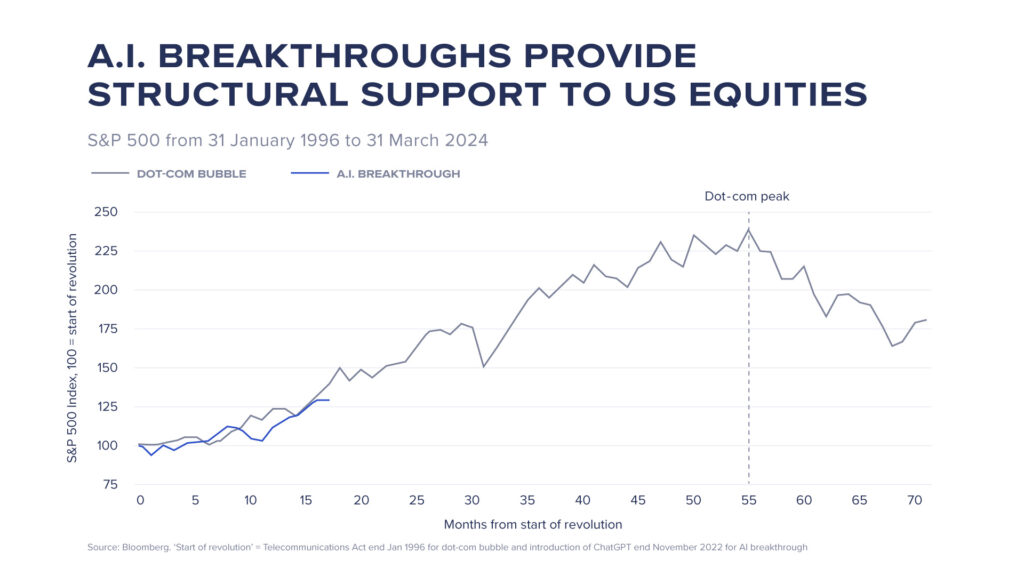

Q2: Are US equities in a bubble?

- The current valuation of US equities is at the expensive end. However, the development of generative artificial intelligence could provide structural support to the earnings of US equities over the long run.

- Drawing parallels between the current AI breakthroughs and the dot-com bubble, the current rally has reached around 35% over 16 months. During the dot-com bubble rally, US equity returns were close to 250% over 55 months. It appears that the rally may still have room to run.

- However, history shows that market downturns are common, with the S&P 500 experiencing an average yearly drawdown of 14%. Maintaining a diversified portfolio remains crucial for ensuring a smoother investing journey through periodic pullbacks in the market.

Q3: Will the conflicts in the Middle East derail the market rally?

- Geopolitical risks continue to be the focus. If tensions between Israel and Iran escalate into full-scale war, the oil supply could be at risk. Iran currently produces over 3 million barrels per day (bpd) of crude oil as a major producer within the Organization of the Petroleum Exporting Countries (OPEC). This could result in higher oil prices, which may further contribute to inflation.

- That said, the impact of war on equities tends to be short-lived. While geopolitical events often lead to short and sharp selloffs in equity markets, they usually rebound quickly, often within weeks.

- Investors may consider hedging their market exposures using safe haven assets such as gold, as well as take advantage of these short-term price dips to add to their positions.

Summary

Despite the delay in anticipated rate cuts, bond yields are at 15-year highs, presenting an attractive entry point. Historical trends indicate that bonds can maintain robust performance even if interest rates stay “higher for longer”.

Following a strong first quarter, equities could face short-term sell-offs due to persistent geopolitical risks and market repricing for delayed rate cuts. Maintaining a diversified portfolio remains crucial for ensuring a smoother investing journey through periodic pullbacks in the market. We prefer equal-weighted equity ETFs over market-cap-weighted ETFs. You can consider utilising safe-haven assets like gold to hedge against short-term market downturns or strategic buying during these fluctuations to bolster long-term gains.

You must be logged in to post a comment.