Most of us in Singapore could be quite familiar with high-interest rate savings accounts such as the UOB One Account and OCBC 360 Account. These savings accounts can offer account holders quite attractive interest rates, provided that certain criteria are met, such as minimum spending on credit cards and a monthly salary credited into the account. However, as the Fed is expected to start lowering interest rates in the second half of 2024, some of the candies can be taken off the table.

Banks Start Cutting Interest Rates

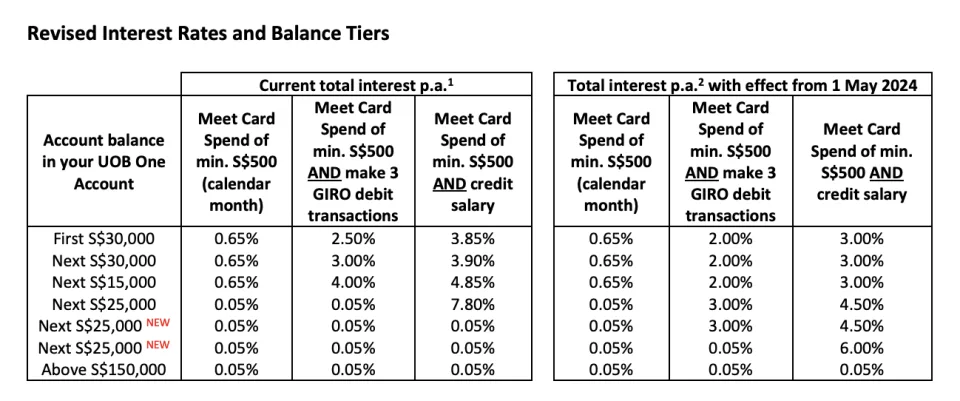

Last week, UOB announced that it would be cutting interest rates on its flagship UOB One account, starting from 1 May 2024. If you have S$100,000 in your UOB One account, you may see the effective interest rate on your balance decrease from 5.00% p.a. to 3.38% p.a. This means your monthly interest could decrease to S$281.3 from S$416.7.

UOB was not the only bank rolling back its bonus interest rates. Similarly, Standard Chartered announced that it would lower the maximum interest rate on its flagship savings account from 7.88% to 7.68%. Other banks are likely to follow suit as market conditions start to shift.

How to Optimise Your Cash as Savings Rates Decline?

If you have idle cash in your savings account, it is probably time for you to start looking for other options to optimise your cash savings. Here are some ways to make your cash work harder for you:

1. Look for alternatives to savings account

Beyond the standard savings account, there are other cash management tools that can potentially earn you higher interest rates.

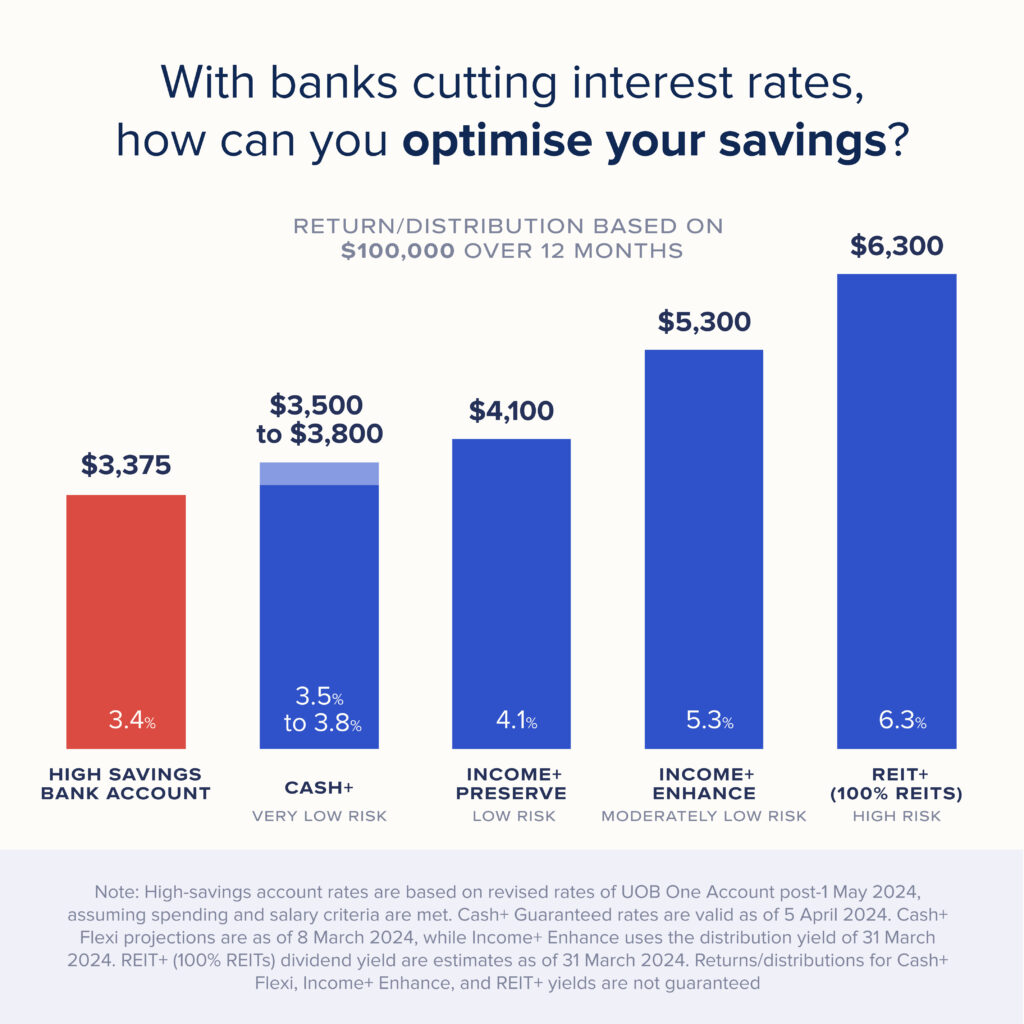

For instance, in Syfe, we have Cash+ Flexi, a low-risk money management solution that invests in money market funds. The product is suitable to park your emergency fund, as it is highly liquid and allows withdrawal within 1 to 2 working days. The current projected return is 3.8% p.a.

We also have Cash+ Guaranteed, which currently offers a guaranteed return rate ranging from 3.5% to 3.8% p.a., with a lock-up period of 3 months to 12 months.

Both cash management solutions can enable you to get potentially higher returns than leaving your cash in a savings account, and there are no hidden strings such as minimum required funding amount or qualifying criteria.

2. Lock into higher rates

As interest rates are expected to decline, for cash that you don’t need in the immediate term, you can consider locking your cash in fixed deposit products with longer maturity terms. This helps reduce the reinvestment risk—that is, after the term matures, you receive a lower return.

We have introduced Cash+ Guaranteed for 6 months and 12 months, which offer 3.8% p.a. and 3.5% p.a., respectively (as of 5 April 2024). You may want to consider allocating part of your spare cash to lock in these attractive interest rates.

3. Invest in assets that could benefit from lower interest rates

While the return on cash starts to dwindle when interest rates decline, some assets can actually benefit from lower interest rates, such as bonds and S-REITs.

Bond prices tend to increase when the interest rate declines. As interest rates lower, investors in bonds could potentially see price appreciation while receiving attractive income. S-REITs typically benefit from lower interest rates as their borrowing costs decrease, potentially leading to higher distributable income.

For bonds, we have the Income+ portfolios, which invest 100% in bonds by leveraging on PIMCO’s top-tier actively managed funds, with an estimated distribution yield of 4.0% p.a. to 6.0% p.a. REIT+ portfolios , developed with SGX, generate attractive dividends from Singapore’s leading REITs. The current estimated dividend yield of REIT+ (100% REITs) is around 6.3% p.a.

How much return/distributions can you receive from S$100,000 over 12 months?

Read More:

You must be logged in to post a comment.