Table of contents:

Do any of the following resonate with you?

I am planning a family vacation for the upcoming holiday season.

I am preparing for my wedding next year.

I am saving for a housing upgrade in the next 3-4 years.

Life presents us with situations where we need to set aside some cash for specific goals that have a relatively short time frame, whether it is for a family vacation, a wedding, or a home upgrade. Simply leaving your money in a savings account might not be the most efficient choice. Let’s delve into alternatives that could yield better returns on your savings or investments that provide guaranteed principal and returns.

Before going into the details, consider three questions:

1) What are my financial goals?

2) How much cash do I need?

3) How soon do I need it?

Understanding these aspects will streamline your planning.

To better assist you, we will categorise options based on your goal timelines: “Now cash needs,” “Soon cash needs,” and “Later cash needs.” Furthermore, we will provide an overview of the tools you can utilise to meet these financial goals, highlighting the pros and cons of each instrument.

“Now” Cash Needs (less than 3 months)

What are “Now” cash needs? This category is tailored for cash you may need to access immediately or whenever an emergency arises. Here, the emphasis is on certainty and liquidity rather than high returns. It encompasses needs such as daily living expenses and emergency funds.

High-yielding savings accounts

Traditionally, savings accounts are where individuals keep their spare cash. Some banks offer bonus interest to promote the use of their other financial services, such as credit cards, investments, or insurance.

Estimated yield: 0.5% to 3.85% p.a, varying based on the bank and its conditions.

Pros: High-yielding bank accounts offer immediate access to the cash. The money is insured by the Singapore Deposit Insurance Corporation (SDIC) up to S$75,000.

Cons: The base interest rate is 0.05%. While the promoted bonus interest rates might seem enticing, they frequently come with conditions. These might include requirements like salary crediting, a minimum amount in credit card spending, a specific number of bill payments, or occasionally, the purchase of bank-specific investment or insurance products. Deposit requirements may range from a minimum amount to a capped maximum, often at S$100,000. A tiered interest rate system results in differing rates for various portions of your deposit. Navigating these varying conditions and calculations to attain bonus rates can be confusing and demand extra attention.

Syfe Cash + Flexi

Syfe Cash+ Flexi is a low-risk money management solution. The portfolio is structured with a 30% allocation to LionGlobal SGD Money Market Fund (MMF) and a 70% allocation to the LionGlobal SGD Enhanced Liquidity Fund (ELF).

Projected yield: 3.7% p.a. (as of 28 September 2023)

Pros: Syfe Cash+ Flexi offers daily liquidity, allowing withdrawals within T+1 business day, ensuring timely access to your funds during emergencies. There are no minimum investment requirements or maximum limits. Unlike savings accounts with tiered interest systems, the 3.7% p.a. projected return is applied for all your funds without any conditions. Additionally, returns are compounded daily,making sure you retain all accrued gains irrespective of the length of your investment.

In comparison to direct investments in the two funds, Syfe Cash+ Flexi takes advantage of the institutional share classes, which come with lower management fees than their retail counterparts.

Cons: Syfe charges a small 0.1% annual management fee on Syfe Cash+ Flexi. It is important to understand that Syfe Cash+ is not a bank savings or deposit offering. It is a low risk investment portfolio managed by Syfe and Cash+ Flexi does not guarantee any returns.

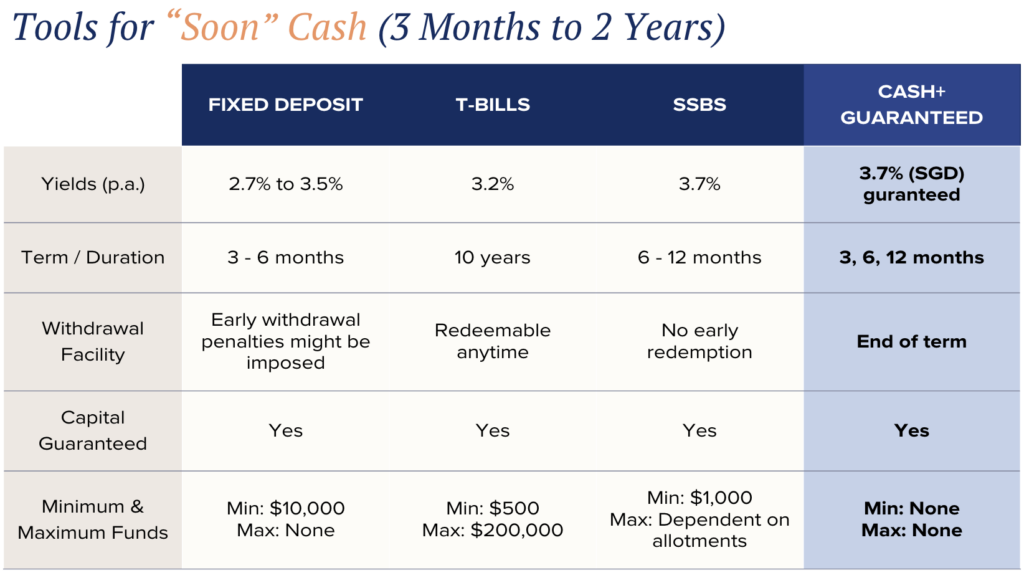

“Soon” Cash Needs (3 months -2 Year)

What are “Soon” cash needs? This category is for cash needs that you anticipate using between 3 months and 2 years. Typical uses might be savings for special occasions like weddings, family trips, or for big-ticket purchases. While security remains a priority, you can afford to compromise slightly on liquidity. Since there is no immediate need for the cash, you can lock it away for a period of time to enhance your returns.

Guaranteed is a low risk investment portfolio managed by Syfe.The guaranteed return is as of 25 September 2023.

Fixed deposits

You may already be very familiar with fixed deposits. With this option, you commit your funds to the bank for a specified duration. At the end of this term, the bank returns both your principal and interest, typically offering higher guaranteed returns than regular savings accounts.

Estimated yield: 2.7-3.5% p.a.

Pros: Fixed deposits are a low-risk option, ensuring the security of your principal and providing a fixed return upon maturity. They are insured by SDIC up to S$75K and offer a range of tenures from 3 to 36 months.

Cons: To qualify for promotional rates of fixed deposits, you need to meet certain conditions set by the banks. For instance, some banks might require fresh funds and a minimum deposit, typically S$20,000 and above. Often, the more attractive fixed deposit rates are reserved for a bank’s premium customers. Should you withdraw your funds before the maturity date, penalty fees may apply.

Singapore Savings Bonds (SSBs)

Singapore Savings Bonds (SSBs) are fixed-income securities that provide regular interest payments and repay the principal upon maturity. They’re an exceptionally secure option, being government-backed. The key feature of SSBs is the step-up interest rate structure where the rate increases over time. For instance, for the latest September 2023 issuance, the interest rate ranges from 3.1% and 3.5% depending on the tenor of one to 10 years.

Estimated yield: 3.2% p.a (3.05% in year 1 to 3.48% in year 10, September 2023)

Pros: SSBs offer Singaporeans a versatile approach to long-term savings. The longer you retain the bond, the more favorable the interest rate becomes. They’re also fairly liquid, allowing redemption in any month without penalties for early withdrawal.

Cons: SSBs generally offer lower yields, even compared to fixed deposit and T-bills. There’s a limit of S$200,000 an individual can invest in SSBs, which may not be suitable for large investors.

Singapore T-Bills

Singapore T-bills, backed by the Singapore government, are issued at a discount to their face value and repay investors the full face value at maturity. There are two available tenors for T-bills – 6 months and one year.

Estimated yield: 3.7% p.a (based on 6-Month T-bill actioned on 14 September 2023)

Pros: Backed by the Singapore government, T-bills are deemed as a very safe investment option. Their returns typically surpass those of standard savings accounts, making them an attractive choice for investors seeking both safety and a more favourable yield.

Cons: As the interest rates are determined based on a uniform-price auction, you do not know what interest rate you will get when you put the bid.

In addition, given their recent popularity and frequent oversubscription, you might receive only a partial allocation or none at all.

Also bear in mind that trading T-bills in the secondary market can be costly due to low liquidity . Before investing, ensure you are prepared to hold the T-bills to maturity, committing for either 6 months or a year.

Syfe Cash + guaranteed

Cash+ Guaranteed, Syfe’s newest cash management solution, offers investors guaranteed returns on your spare cash. We work with a MAS-regulated bank to garner competitive fixed deposits rates for our clients.

Guaranteed yield: 3.7% p.a. (as of 28 September 2023)

Pros: A primary advantage of Syfe Cash+ Guaranteed is our ability to negotiate with banks at an institutional level to secure better fixed deposit rates, the benefits of which are passed directly to our customers. Syfe establishes partnerships with multiple banks, all regulated by the Monetary Authority of Singapore (MAS), that provide fixed deposits. We consistently evaluate rates from these partners in conjunction with prevailing market rates to ensure the Cash+ Guaranteed rate remains competitive.

Additionally, you are now able to choose to have a 3, 6 or 12-month lock-in period, giving you flexibility to plan when to retrieve your returns based on your own needs.

Syfe Cash+ Guaranteed also stands out for its transparency and accessibility. The rate you see is the rate you get. There are no hidden caps, no complicated hoops to jump through, and no sneaky fees. Moreover, there is no minimum required funding amount or qualifying criteria, such as salary credits, to avail of this opportunity.

In addition, the management fees are waived for now.

Cons: There is a lock-in period of 3, 6 or 12 months, depending on your choice, for the Cash+ guaranteed portfolio during which you can’t take your funds out.

Cash+ Guaranteed is invested in fixed deposits with banks subject to rigorous regulations by the Monetary Authority of Singapore (MAS). While there is minimal protection with respect to SDIC insurance, this portfolio is considered to have very low risk as the portfolios capital and returns are guaranteed by the fact that it invests in fixed deposits with MAS approved banks.

Check out Cash+ Guaranteed for more details

“Later” Cash Needs (More than 2 Years)

For “Later” cash needs, this category refers to funds you do not require in the immediate future. Classic examples include saving to upgrade from an HDB to a condominium. You may also consider cash flow matching to cover cash outflows, such as mortgage payments. Given the longer timeframe, you can take slightly more risk. However, you would still prioritise some level of liquidity while optimising for better yields. Some instruments to be considered for “later” cash needs could be bonds and REITs.

Syfe Income + Portfolios

The Syfe Income+ Portfolios invest into global bonds for steady, diversified income. Unique in its approach, it leverages PIMCO’s established fixed income strategies. We offer two Syfe Income+ variations: Income+ Preserve for consistent income with capital safety, and Income+ Enhance for those eyeing higher immediate returns and long-term growth.

Estimated yield: 4.0% – 6.0% p.a. (as of 30 August 2023)

Pros: Compared to typical bond funds and bond ETFs, which often focus solely on one mandate, Syfe Income+ portfolios take a global approach. Syfe optimises the allocation across different sectors and regions depending on the market conditions.

Another advantage is the efficient handling of foreign exchange and taxes. Investors in Singapore might incur a 20-30% withholding tax when investing in US-domiciled bond ETFs directly. To optimise tax implications, Syfe Income+ Portfolios invest in Irish-domiciled funds, which are not subject to withholding taxes. Moreover, Income+ portfolios utilise currency-hedged share classes to mitigate foreign exchange volatility.

Syfe Income+ portfolios also have lower fees than typical bond funds. The Income+ Portfolios use institutional share classes, passing on rebates to investors. You can achieve up to 60% savings in fund fees compared to retail DIY investing

Cons: Returns from Income+ portfolios are not guaranteed. The portfolios may suffer losses due to change in market conditions, such as a sudden spike in interest rates. However, our base-case view is that we are near the end of the rate-hiking cycle. Historically, bonds had performed well after the Fed stopped hiking rates.

Understand more about Income+ Portfolio.

Syfe REIT+ Portfolios

Syfe REIT+ Portfolios are designed to track the iEdge S-REIT Leaders Index. You have two portfolio options based on your risk tolerance. One invests entirely in Singapore’s 20 largest REITs, while the other blends REITs with government bonds to mitigate volatility.

Estimated yield: 5.8% p.a. for 100% REIT, and 4.6% p.a for REIT with risk management (as of 30 August 2023)

Pros: With Syfe REIT+ portfolios, you benefit from diversification by investing in over 20 of Singapore’s top REITs. There’s no minimum investment requirement. Management fees are lower than those of REIT ETFs, and there are no brokerage or transaction fees.

The portfolio’s performance benefits from added optimisation. We have incorporated features like liquidity screening, automatic dividend reinvestment, and risk management to optimise returns.

Cons: By nature, REITs are sensitive to interest rate changes. When interest rates rise, REIT performance typically suffers. However, we believe we are nearing the peak of policy rates, even though a rate cut might only materialise only in the second half of 2024.

Get better understanding about REIT+ Portfolios.

Complete Suite of Cash and Income Solutions

REIT+ total return assumes 3% capital gain for REIT+ over the long term.

Source: Syfe. As of 31 August 2023. Statistics are based on the weighted fund allocation within each model portfolio.

To provide a clearer picture of how these tools can be combined to achieve your financial goals, we have assembled a case study. You can view it here: Case Study Of Benson

Watch our webinar: How to Optimise Your Cash Saving for Higher Return and Passive Income in Singapore?

You must be logged in to post a comment.