Life is unpredictable. Having cash at your disposal is essential. However, having an excessive amount of cash can pose more risks to your wealth too. Let us delve deeper into the pitfalls of holding onto too much cash and the strategies to efficiently manage it.

The risk of having too much cash: inflation erodes your money’s value

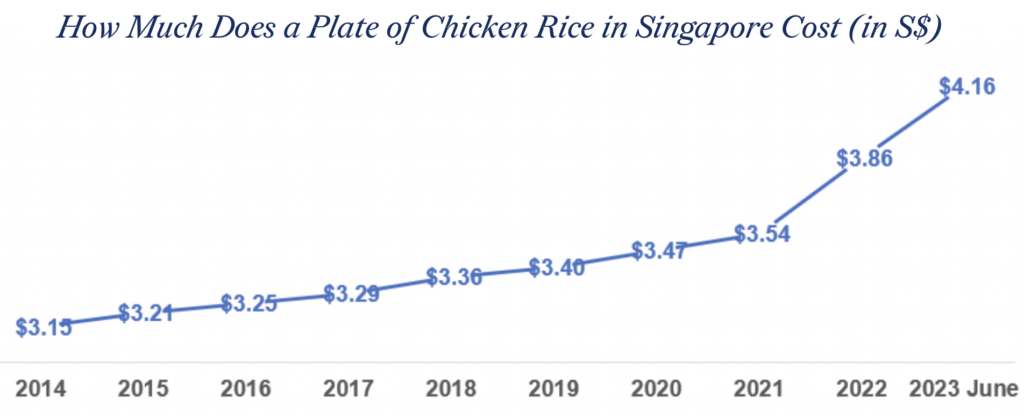

Inflation’s silent creep can erode the true worth of your cash. If your savings are not matching inflation’s pace, you are losing buying power. Take Singapore’s beloved chicken rice example, in 2014, the average price was S$3.15 a plate. Mid of this year, prices went up to S$4.16 – a 32% hike in less than a decade. Your cash should work as hard as inflation does.

How much cash is too much?

How can we determine if we have too much or too little cash? There is no one-size-fits-all answer, but having a guiding principle can help. There are several buckets of funds in the budget, and you need to determine how much cash to allocate to each:

- “Now” cash needs: This category is tailored for cash you may need to access immediately or whenever an emergency arises. Here, the emphasis is on certainty and liquidity rather than high returns. It encompasses needs such as daily living expenses and emergency funds.

- “Soon” cash needs: This category is for cash needs that you anticipate using between 3 months and 2 years. Typical uses might be savings for special occasions like weddings, family trips, or for big-ticket purchases. While security remains a priority, you can afford to compromise slightly on liquidity. Since there is no immediate need for the cash, you can lock it away for a period of time to enhance your returns.

- “Later” cash needs: This category refers to funds you do not require in the immediate future. Classic examples include saving to upgrade from an HDB to a condominium. You may also consider cash flow matching to cover cash outflows, such as mortgage payments. Given the longer timeframe, you can take slightly more risk. However, you would still prioritise some level of liquidity while optimising for better yields. Some instruments to be considered for “later” cash needs could be bonds and REITs.

So, to determine if you are holding too much cash, first calculate the total amount you need based on the buckets listed above. If the cash in your bank significantly exceeds the combined amount of your listed goals, you likely have too much cash. In that case, consider investing this surplus into your investment portfolio for potential long-term returns.

How to maximise return on your cash?

Case Study Of Benson

Background: Benson, at 35, enjoys a comfortable life with his family. Married and blessed with a child, they reside in a 4-room HDB flat. Drawing a monthly gross salary of S$10K, Benson manages his finances well. His household expenditures total S$5K monthly, ensuring his family’s needs are met.Of the S$2.5K monthly mortgage, S$1.8K is conveniently offset using his CPF, with the balance of S$700 settled in cash.

And speaking of cash savings, Benson has impressively accumulated S$200K in savings – a testament to his financial acumen and discipline.

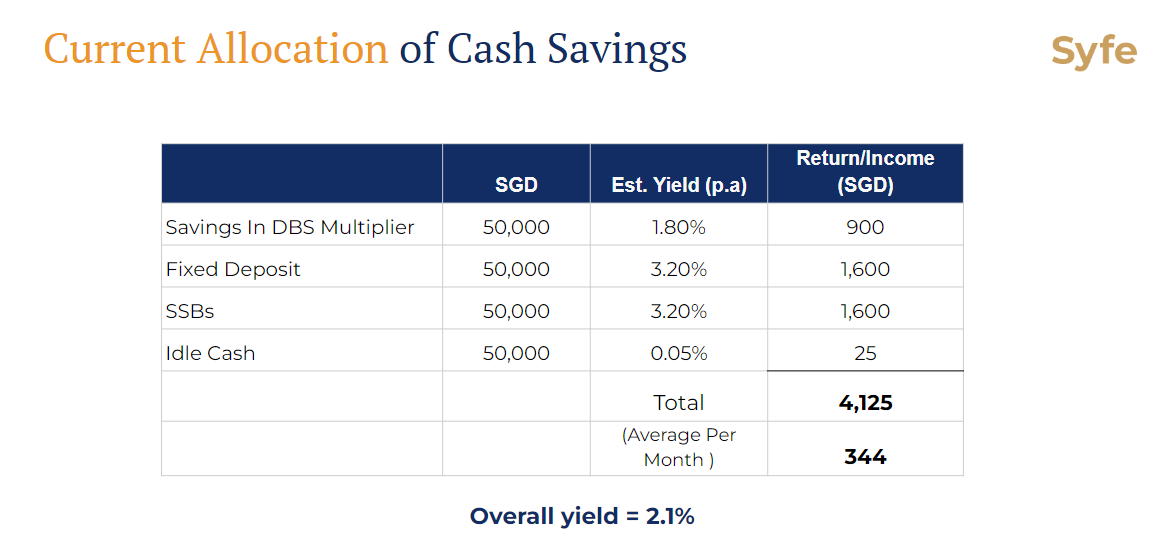

How he manages his cash currently: Currently, Benson has allocated his hard-earned savings into secure instruments. He has S$50K in a DBS Multiplier account, S$50K in a fixed deposit, another S$50K in Singapore Savings Bonds (SSB), and the remaining S$50K in idle cash. From these instruments, he generates an interest income of S$4,125 per year, which equates to a yield of 2.1% p.a. There is potential for optimization in this arrangement.

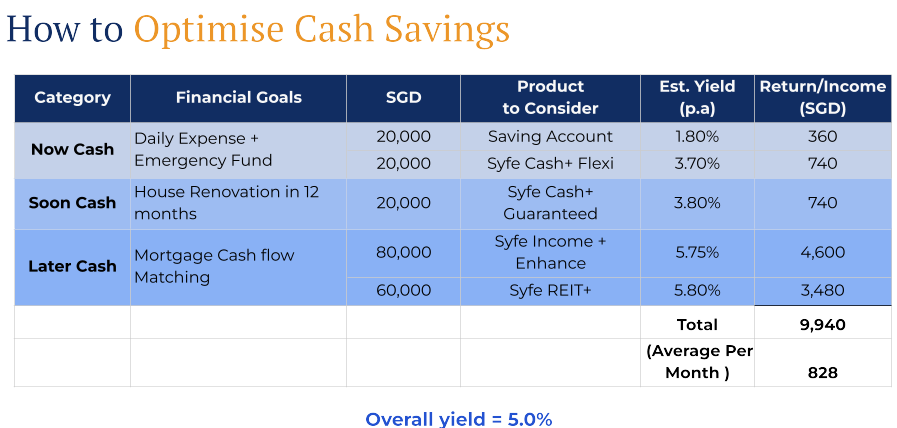

How Benson can optimise his cash savings: Benson’s financial strategy can be enhanced by first aligning his cash management with specific financial goals, categorised as “Now,” “Soon,” and “Later.” “Now cash needs” include immediate expenses and emergency funds. Benson can maintain a portion of his funds in a savings account. However, to optimise returns on this category, he can consider allocating part of it to Syfe Cash+ Flexi. This instrument allows T+1 business day withdrawals while offering a potentially higher return than regular savings.

“Soon cash needs” is short-term commitments less than two years. Benson is planning a home renovation in the next 12 months that will require S$20K. For such upcoming expenses, he can lock away a portion of his funds without affecting his liquidity. The Syfe Cash+ Guaranteed is an ideal choice for this, given its options for a 3, 6 or 12-month lock-in period, allowing Benson the flexibility to choose between a shorter or a longer-tern commitment.

“Later cash needs” is for cash needs in later than two years and for cash flow matching commitments. In Benson’s case, his primary focus is his mortgage. It’s essential that he aligns his funds effectively for this commitment. Benson can optimise his returns by investing in Syfe Income+ Enhanced and Syfe REIT+. These instruments not only offer better yields but also align with his long-term financial strategy.

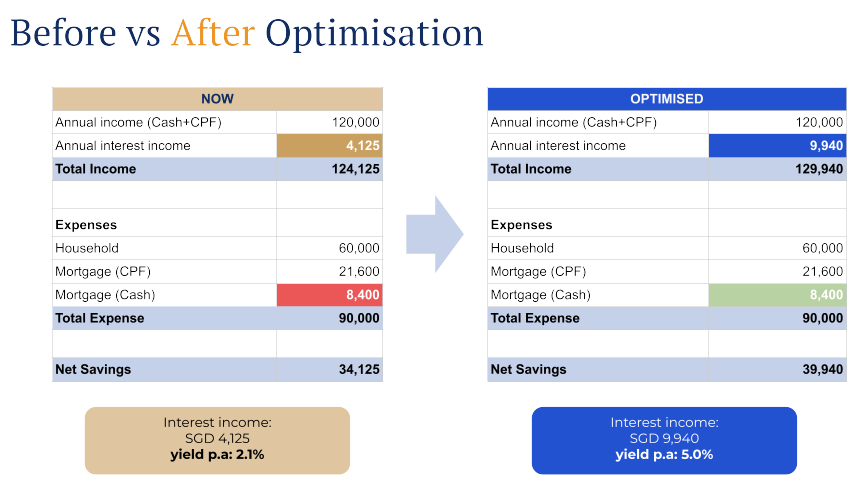

In sum, by restructuring his finances around specific goals and timelines, Benson can unlock greater financial efficiency and return potential. After optimising his cash savings, Benson can anticipate an interest income of approximately S$9,920 a year, an additional S$5.8K then before. This corresponds to a yield of 5.0%.

Better prepared for the future:It’s noteworthy that after optimisation, the annual interest income from these instruments can cover Benson’s out-of-pocket cash for mortgage payments. This adjustment allows him to save even more. With his near-term cash needs addressed, his annual surplus savings (~S$40,000) can be channelled towards long-term objectives, such as retirement.

With this proactive approach to manage his cash savings, Benson not only ensures a stable present but also paves the way for a more secure future. By strategically redirecting his savings, he strengthens his retirement foundation, ensuring a comfortable and worry-free golden age.

Learn more about our cash management solutions:

You must be logged in to post a comment.