Chinese equities tumbled on Monday (24 October) following China’s 20th Party Congress. Here’s what to know.

Xi 3.0

The National Congress of the CCP closed over the long weekend. President Xi Jinping appointed loyalists while staying for an unprecedented third term. This makes him the first leader since Mao Zedong to stay in power for more than 10 years.

How did investors react?

Monday’s selloff was not driven by fundamentals. This consolidation of power was largely expected, but not particularly welcomed by international investors. The reshuffle carried the implication of a less moderate approach to managing Covid-19 and dealing with the United States – possibly at the expense of economic growth.

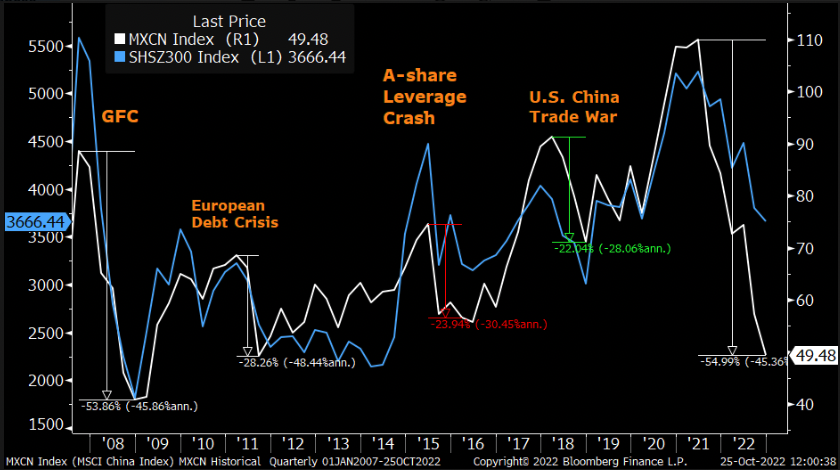

MSCI China, which tracks Chinese equities that are available to international investors, fell 9.6% on Monday before recovering 1.8% on Tuesday. Chinese internet companies fared worse, with Kraneshares CSI China Internet ETF, falling 14.2% before recovering 3.4% on Tuesday. After the selloff on Monday, international investors turned net-buyers on Tuesday.

Onshore, investors were more measured, with the benchmark CSI 300 index (comprising Shanghai and Shenzhen listed stocks) falling almost 3% before making up for half of those losses subsequently.

Long term secular growth trend remains

China continues to be the world’s second largest economy and contributes almost 18.5% to the world GDP based on PPP (Purchasing Power Parity) terms in 2021.

China has historically been the world’s manufacturer, where growth was driven by trade and exports. As the intentional transition to a more consumer-led economy is underway, market volatility may persist in the near term. However, this transition remains well supported by both fiscal and monetary policy as China evolves to be less reliant on capital intensive industries, such as real estate development.

To reflect that and capture long term secular growth trends in China, Syfe Core portfolios maintain a more representative allocation to China ranging between 3-18% depending on the risk level of the portfolio selected. Moreover, exposure to Chinese equities offer portfolio diversification. US equities and Chinese equities exhibit moderate correlation over the medium and long term as the drivers of investor flows and earnings differ.

2023

The latest quarterly GDP reading was released on Monday, Oct 24, 2022, about a week late, a somewhat unusual delay, which added to worries about the state of the economy. China’s GDP grew 3.9% on a year on year basis, better than consensus estimates of 3.3%, but below the full year target of 5.5%.

In the effort to boost growth and support the beleaguered property sector, the PBoC has cut lending and interbank lending rates and increased liquidity even as most major central banks have gone the other direction. Monetary policy is expected to remain accommodative in 2023.

Post Monday’s strong selloff, valuation for Chinese equities are now about 10 times forward PE (forecasted price-to-earnings ratio), putting them in the 5th percentile in the last two decades. One bright spot is the rise of China’s domestic brands. Fuelled by rising nationalism and improvements in quality, Chinese consumers are increasingly shifting away from foreign brands towards domestic names like Li-Ning and Midea, the Chinese equivalents to Nike and Panasonic respectively.

What we are watching

Alibaba’s 11.11 Shopping Festival pre-sales kicked off this week, this will be an area to watch to understand if retail sales and consumer sentiment in China holds up even as top-line growth moderates.

China is the remaining mega-economy to re-open. The gradual re-opening of Hong Kong is a positive sign, with the city preparing to host a major financial conference and World Rugby Sevens soon. We will be tracking how Hong Kong fares and signs of greater easing of Covid-19 restrictions in the mainland.

The CCP’s annual Central Economic Work Conference in December will also shed more light on China’s economic policy direction.

Despite recent pressures, Chinese equities still have a place as part of a globally diversified portfolio. We encourage investors to keep a long-term perspective and consider China’s role in strategic asset allocation.

You must be logged in to post a comment.