Singapore’s banking sector has long been a source of pride and profit for local investors, with DBS, UOB, and OCBC consistently outshining their peers on the Straits Times Index. However, recent Q2 earnings reports coupled with the Fed’s hints at potential interest rate cuts have left investors pondering: Which of these blue-chip giants is best poised to navigate the shifting market tides?

In this deep dive, we’ll analyse each bank’s earnings, strategy, and outlook to help you choose the best investment for your portfolio.

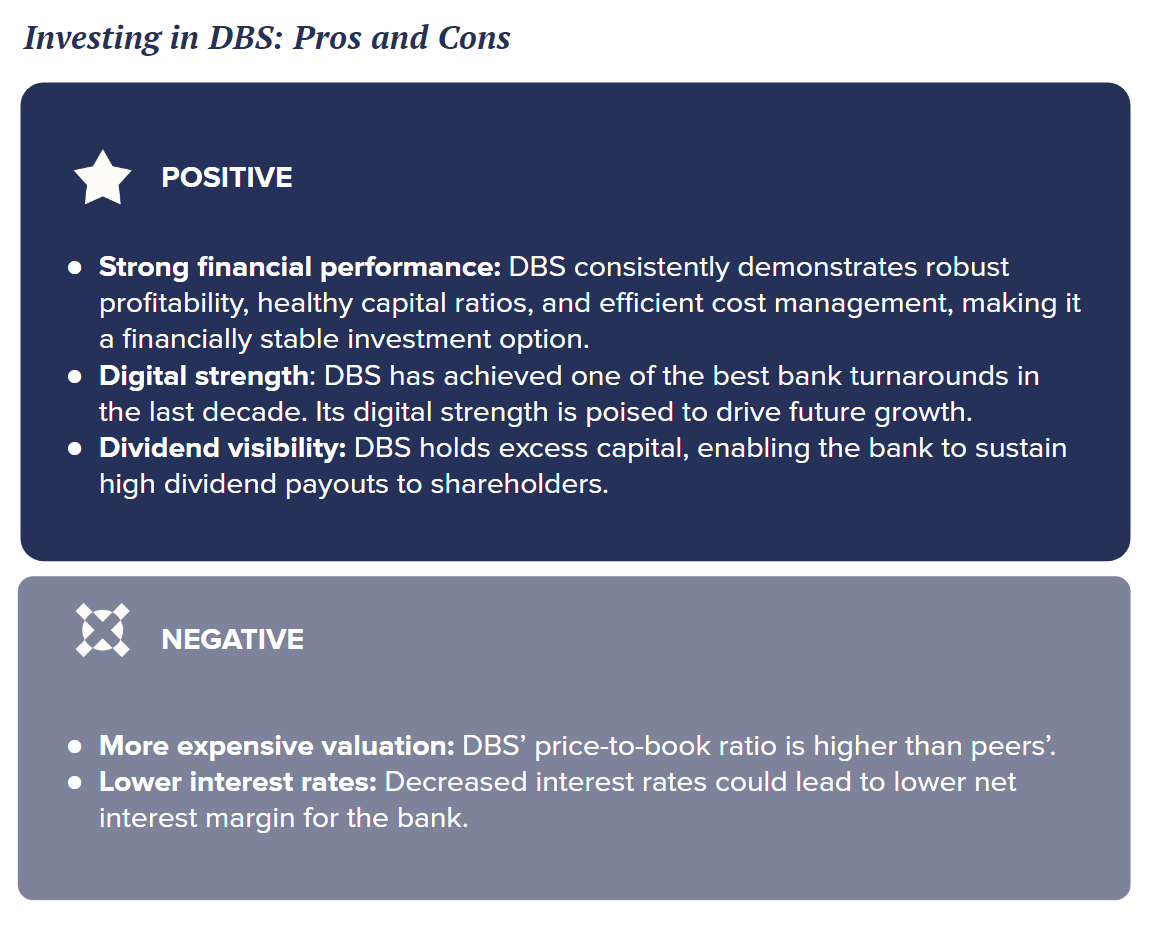

DBS: Strong Q2 results amid leadership transition

DBS delivered another outstanding quarter. Its impressive 18.2% return on equity(ROE) further solidifies the bank’s strong performance. Total income also saw a healthy 9% boost, reaching SGD 5.5 billion.

It’s a success story across the board. Commercial book net interest income is up, thanks to balance sheet growth and improved margins. Fee income hit a record high, and treasury customer sales remain robust. Market trading income also saw a positive uptick.

Wealth management is undoubtedly DBS’s shining star. Singapore’s appeal as a wealth hub, with its political stability, attractive tax policies, and favourable environment for family offices and trusts, is paying off for the bank. Wealth assets under management of DBS surged 24% to a record S$396 billion. This translated into a remarkable 19.6% increase in wealth management fees, reaching S$1.3 billion for the quarter.

Leadership change at DBS: Another key highlight is that DBS is going through leadership change. DBS has announced that Tan Su Shan slated to take over as DBS CEO from Piyush Gupta in March 2025. Ms. Tan has been appointed Deputy CEO in the interim to ensure a smooth transition. She has been with the bank for the last 14 years and played a crucial role in building DBS’s wealth management business into a major player in Asia. Her extensive experience across different banking segments, combined with the planned transition period, suggests that DBS is well-positioned for continued success under her leadership.

Outlook: Overall, DBS’ management struck a positive tone in its guidance. CEO Piyush Gupta emphasised the bank’s preparedness for economic challenges and lower interest rates, citing strong reserves, reduced interest rate sensitivity, and a solid financial position. This resilience will enable DBS to continue supporting clients and generating shareholder value going forward.

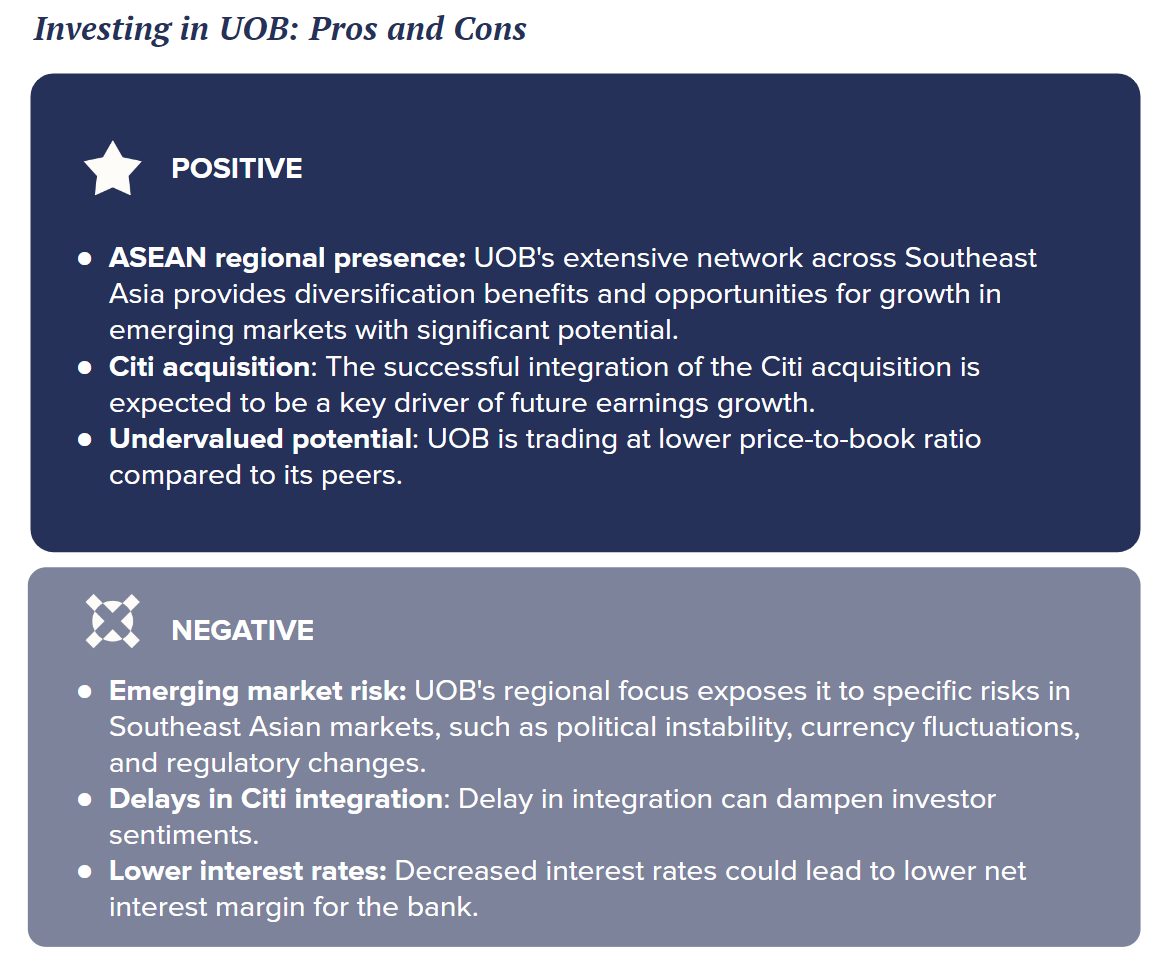

UOB: Cautious optimism despite mixed Q2 performance

UOB’s Q2 results were a mixed bag. Core net profit held steady at S$1.5 billion compared to the previous year. Its net interest income dipped 1% due to lower margins.

A bright spot was the bank’s wealth management segment. Group Retail’s wealth management income saw a strong 40% year-on-year growth, fueled by increased sales of structured notes, bonds, and unit trusts, along with consistent performance in bancassurance.

Outlook: UOB’s management team expressed optimism about the ASEAN region, expecting it to remain relatively resilient. They highlighted the region’s long-term potential, supported by strong fundamentals and foreign direct investment inflows as companies diversify their supply chains.

With an expanded customer base and improved market position, the bank believes it is well-positioned to capitalise on regional opportunities. The one-time costs associated with the recent acquisition of Citibank’s ASEAN consumer businesses are expected to decrease significantly next year, following successful integration in Malaysia, Indonesia, and Thailand.

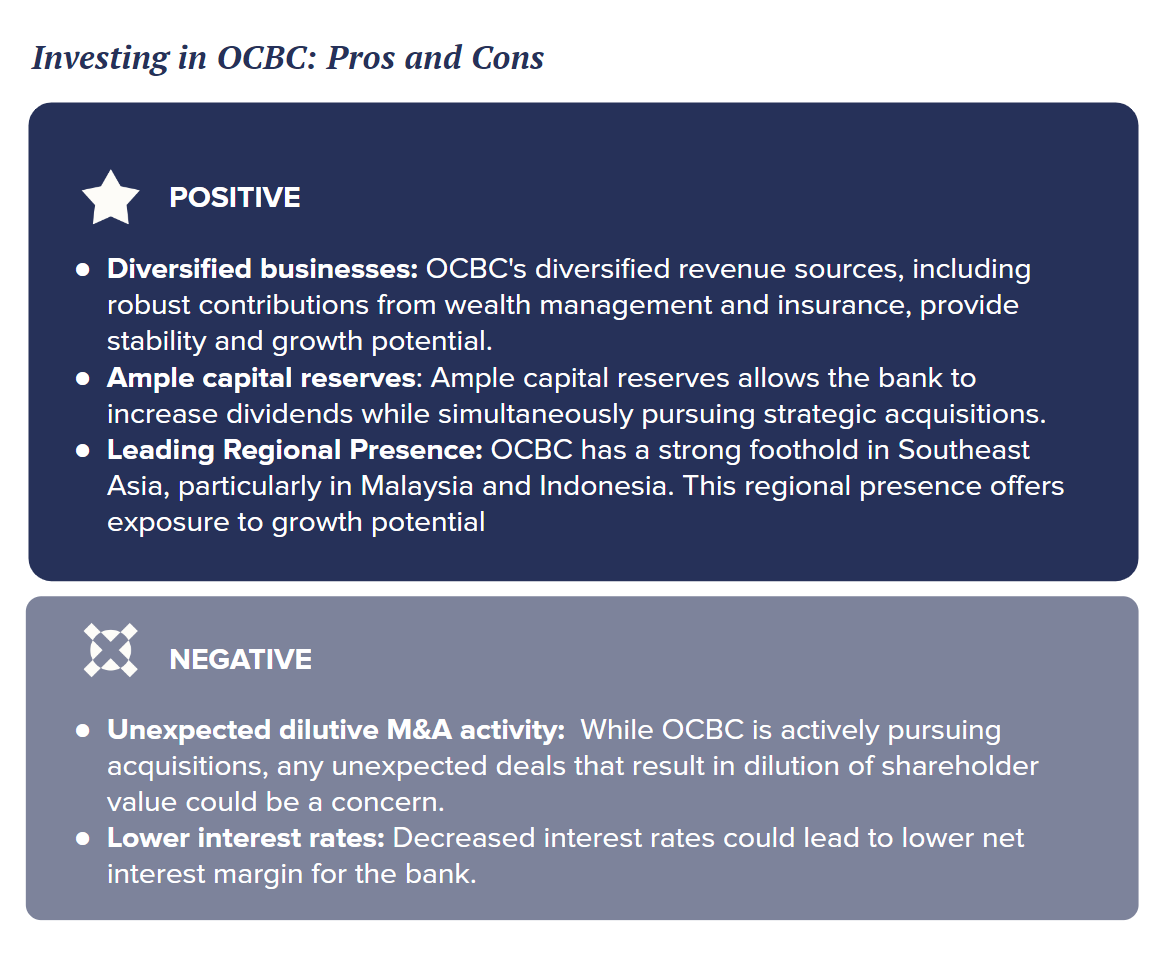

OCBC: Net profit hit new highs and strategic acquisitions continue

OCBC had a stellar Q2, leading the pack among the three major local banks with an impressive 14% surge in net profit, reaching S$1.9 billion. This outstanding result was fueled by growth across all key areas of their business. Net interest income saw a healthy 2% increase, hitting S$2.4 billion. Non-interest income also jumped by a robust 13%, reaching S$1.2 billion, driven by strong performances in fees, trading, and insurance.

In addition, the bank’s strategic growth initiatives remain on track, with the successful acquisition of PT Bank Commonwealth Indonesia and an increased stake in Great Eastern Holdings. These developments further strengthen OCBC’s position and pave the way for future growth.

Outlook: OCBC’s management team provided upbeat guidance. They believe the bank’s diversified business model and focus on key growth areas will enable them to navigate a challenging environment successfully. The bank’s strong capital position and prudent risk management practices provide a solid foundation for continued growth.

How to invest in DBS, OCBC and UOB

If you’re keen to gain exposure to Singapore banks, you can invest in them through a brokerage platform like Syfe Brokerage which offers access to both Singapore and US markets.

Syfe Brokerage is an easy and low-cost option for Singapore stock investing. Pricing for SGX stocks is just 0.06% of traded value (minimum S$1.98), and there are no platform and withdrawal fees.

Disclaimer: This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

You must be logged in to post a comment.