Providing a comfortable life for our family is an important goal of many of us. It is a key reason why we work hard, hustle, and try to advance in our careers. It drives us to look for ways to build wealth for our family beyond a monthly paycheck. You hear of people attending overpriced weekend financial seminars or learning the “best secrets” to get rich that are promoted by slick marketers.

In reality, building wealth and growing rich over time is not as complicated as people think. As John Bogle wisely stated, “The secret is there are no secrets.”

The most realistic path to attaining wealth over the long term is simply through investing. While there is no magic formula behind investing success, these time-tested principles can help you reach your wealth goals faster.

#1. Start early

Growing wealth starts with saving money. The more money you save, the more you have to invest. And the earlier you invest, the more you accelerate the rate of compound interest, and by extension, the growth of your money.

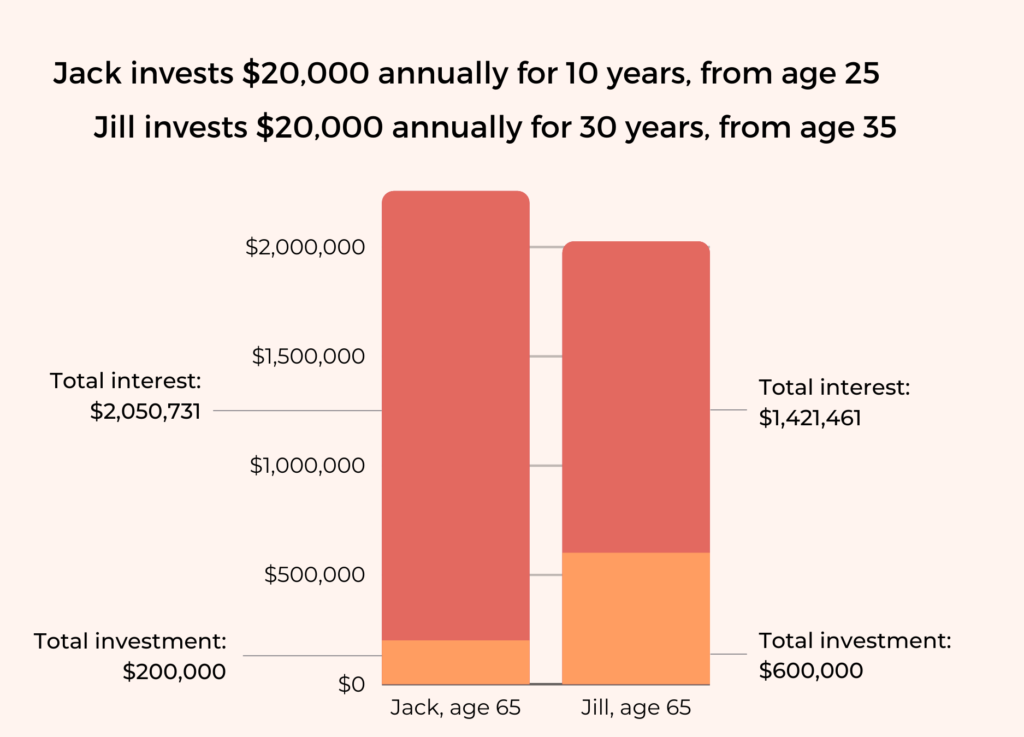

Consider the example of two friends, Jack and Jill below.

Jack starts investing at age 25 and invests $20,000 every year until he turns 35. Jill only starts investing at age 35 and invests $20,000 every year until she turns 65. Surely her deck must be stacked against Jack.

Not so. Jack’s investing headstart more than offset Jill’s greater total contribution, boosted by his compound interest earned over 30 years. So, don’t wait to invest. Start now.

#2. Don’t put all your eggs in one basket

Diversifying your portfolio across asset classes, sectors and geographies is key to optimising risk-adjusted returns. Investing in a diversified portfolio helps you to spread out your investment risk because your portfolio assets don’t correlate with each other. This means that they tend to react differently to the same economic event (like a recession) and their performance differs from each other. When some of your assets perform poorly, others can bring profit.

One of the most common mistakes investors make is holding the majority of their portfolio in one or a few individual stocks. This exposes them to significant concentration risk. Think about Hyflux and the many investors who put their life savings into the company. Should a particular stock underperform, your portfolio can lose a large percentage of its value in just a short period of time.

A balanced, diversified investment mix like what Syfe’s global ETF portfolios offer can help investors build long-term wealth. Beyond stocks, bonds, and commodities, real estate is another valuable addition to further diversify your portfolio. The Syfe REIT+ portfolio holds more than a dozen quality Singapore REITs within one portfolio. It tracks the SGX’s i-Edge S-REIT Leaders index, which measures the performance of the 20 largest REITs in Singapore.

#3. Minimise investment costs

If fund costs are incurred regardless of fund performance, then it is a mathematical certainty that the lower your costs, the more you get to keep of any returns the fund makes.

This is a key reason why low-cost passive investments like exchange-traded funds (ETFs) have become hugely popular in recent times. Compared to ETFs, investors pay more in fees when they invest in actively-managed investments such as unit trusts.

High fees can eat away at your returns. A hypothetical investment of $100,000 invested at an annual return of 5%, would be worth $324,000 after 30 years if the annual investment cost totaled 1%. If the investment cost was 2%, the final investment value would only be $242,000 – $82,000 less.

#4. Manage risk first over returns

Many investors focus on investment returns and tend to forget that managing risk is at least as important – if not more so.

Risk can be defined as the likelihood of a significant loss. To understand the importance of managing risk in creating and preserving wealth, imagine this. If you lose 50% of your portfolio value, your remaining investment has to make a 100% gain just to get back to even.

Risk management thus seeks to limit your downside risk and minimise loss. While all investments carry a certain amount of risk, understanding the risk / reward trade-off can help protect your investment portfolio. Remember, while lower risk translates to lower returns, taking on more risk does not always equate to higher returns.

#5. Stay invested

Successful investing is ultimately a matter of staying the course, even during periods of extreme volatility. History proves that panic-selling during a downturn almost always ends poorly for investors.

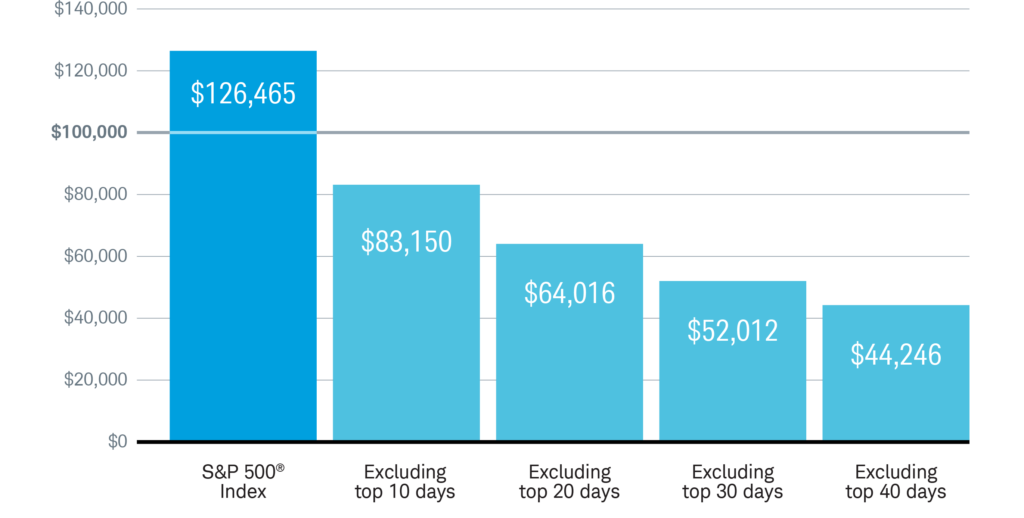

Many investors sell their stocks in panic during a downturn and re-enter the market only after a recovery has happened. Missing even a few trading days could mean missing some of the market’s greatest gains.

An investor who had invested $100,000 on 1 January 2009 – in the midst of the global financial crisis – but missed just a month of trading (or the top 30 trading days), would have had US$74,453 less by the end of the year compared to if he had stayed invested for the whole year.

The stock market has historically favoured investors who take a long-term approach. With average returns trending positive over longer horizons, it pays to commit to a long-term investing strategy and stay invested, even if stock market returns can vary greatly from year to year.

To put these 5 investing principles into action, consider investing with Syfe. To help you make the most of your investment, new clients who sign up will also enjoy $20 free cash credits using the code SYFEPROMO.

You must be logged in to post a comment.