Deciding what your portfolio should include is a complex decision. From equities to unit trusts and bonds to exchange-traded funds (ETFs), you’re spoilt for choice when choosing where to invest your hard-earned money.

Savvy investors however, know that when it comes to building their investment portfolios, diversification is their best friend. And while ETFs and unit trusts make it easy for investors to quickly diversify their investment exposure, the tricky part is deciding which is better.

Broadly speaking, both ETFs and unit trusts pool together investors’ money, which then becomes part of a fund that invests in different assets. ETFs and unit trusts can provide investors with exposure to a broad range of asset classes, sectors and even geographies. In this regard, both fund types offer retail investors an easy way to build a diversified portfolio with just a single investment.

That said, there are differences between ETFs and unit trusts that may impact your portfolio. To help you decide which is better for you, here is a breakdown of what ETFs and unit trusts are and a comparison of their key differences.

What is a unit trust?

A unit trust (also known as a mutual fund) is usually an actively managed investment fund. The fund is managed by a fund manager who chooses which securities (such as stocks or bonds) to invest in according to the mandate of the fund. When someone invests in a unit trust, he or she buys units of the fund – as opposed to individual securities – and earns returns if the underlying securities of the trust perform well and the trust appreciates in value.

Unit trusts generally charge high management fees as fund managers will monitor the markets and conduct research to pick securities they think can outperform the market. They are a popular investment product offered by many banks and financial institutions; you probably know of someone who has invested in unit trusts – or is trying to sell you one.

What is an ETF?

An ETF is usually a passively managed index fund that trades on a stock exchange. An index represents a smaller sample of the stock market based on certain criteria such as geography or market capitalization. Some examples include the Standard & Poor’s 500 index (S&P 500) which combines 500 large-cap US stocks into one index, or the Straits Times Index (STI) which tracks the 30 largest companies listed on the Singapore Exchange (SGX).

ETFs aim to mimic the performance of the index they track and generally hold the same proportion of securities as its index. In other words, if you invest in an ETF that tracks the S&P 500, you gain exposure to the US market without having to invest in all 500 of its component stocks. Due to their passively managed nature, ETFs have lower management fees and operating expenses than actively managed unit trusts.

ETFs have skyrocketed in popularity over the past decade, due in part to the growth of the passive investing movement worldwide. There are more than 6,000 ETFs globally today, up from just 276 in 2003!

How are they different?

ETFs and unit trusts both have their respective benefits and risks. Besides the difference in management styles, ETFs and unit trusts also differ in terms of investment cost, performance and liquidity, as we explain further below.

Fees and costs

It is important to know how much it costs to invest in ETFs or unit trusts because their respective fees and charges can impact your overall investment return.

Investing in unit trusts typically costs more than ETFs as you pay more for fund management fees, upfront fees, trail fees and miscellaneous fees such as marketing, administration and audit fees.

Here’s a look at how the fees for both ETFs and unit trusts stack up in Singapore.

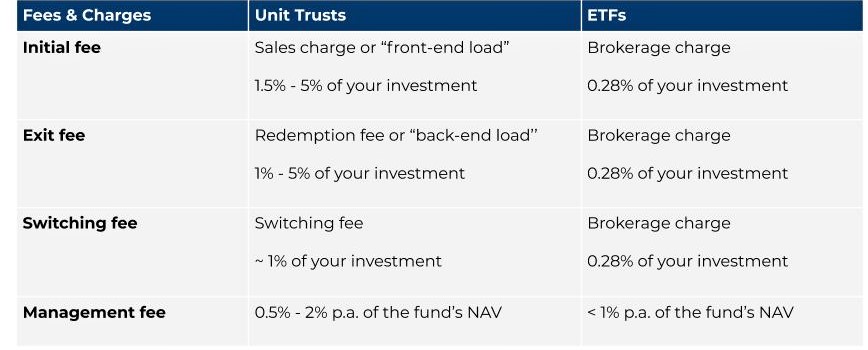

One-off fees

One-off fees include your initial fee, exit fee and switching fee. When you buy a unit trust, you normally pay a sales charge which is then deducted from your investment amount. This means if your investment is $10,000 and the sales charge is 2%, your actual amount invested will only be $9,800.

When you buy an ETF, the sales charge is simply your stock brokerage fee, which is generally 0.28% of your trade amount. If you don’t meet the minimum transaction amount, you will be charged a minimum fee (typically $25). In other words, if you invest $10,000 in an ETF, your actual amount invested will be $9,972.

Some funds charge a redemption fee whenever you sell or redeem your unit trusts. If you switch from one unit trust to another managed by the same fund manager, you may sometimes have to pay the distributor a switching fee as well.

For ETFs however, selling or switching your ETF is similar to selling any other stock and you will incur the standard brokerage fee.

Recurring fees

Major differences lie in the way ETFs and unit trusts charge their recurring fees. An important figure to look out for when evaluating such fees is the fund’s total expense ratio (TER).

A unit trust typically has TER between 1% and 2.5% of its net asset value (NAV). Its TER comprises management fees, trustee fees and other miscellaneous fees. Passively managed ETFs however have much lower TERs due to their significantly lower operating costs. For comparison, the Straits Times Index ETF (STI ETF) has a TER of 0.3% while the Aberdeen Standard Singapore Equity fund, a unit trust which also benchmarks the STI, has a TER of 1.64%.

High TERs can substantially erode investment returns. An investment of $100,000 invested at an annual return of 5%, would be worth $324,000 after 30 years if the TER was 1%. If the TER was 2%, the final investment value would only be $242,000. A 1% difference in TER may seem minimal initially, but over 30 years it adds up to an additional $82,000 forfeited to fees.

Adding to the opacity of unit trusts is the issue of trail fees. Trail fees make up 20% – 60% of the management fee fund managers charge, and they are paid to distributors – the e-platforms, banks, insurance and financial advisors offering the unit trust – so that they continue to provide financial advice or services to you. This begs the question – how do investors truly know if a recommended unit trust is actually the best for them or the one paying the highest trail fee?

Performance

Many investors who choose to invest in unit trusts often do so for higher potential returns since actively managed funds often contend that they can beat the benchmark. If the old adage “You get what you pay for’’ holds true, then it makes sense that investors would expect active funds such as unit trusts to outperform their benchmark indices.

The reality however is that active fund managers usually fail to beat their index targets over the long term once investment costs are factored in.

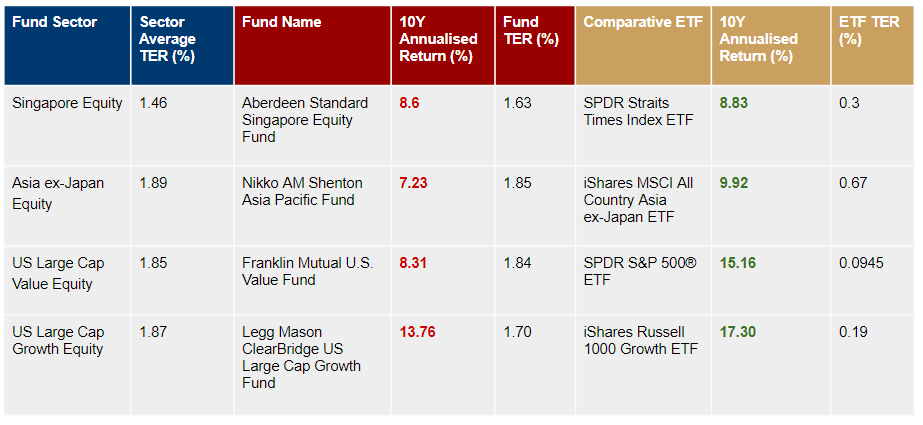

Need more convincing? Here’s a closer look at a few of the largest equity fund sectors in Singapore (based on Morningstar data for funds registered for Singapore sale) and the performance of the popular unit trusts within each category.

Despite their high TERs, the unit trusts we examined actually underperformed their respective indexes over a 10-year period. Yet, investors pay active fund managers high fees with the expectation that they can outperform the market. Their comparative ETFs also generated better returns at significantly lower TERs and the majority of them outperformed their benchmarks as well.

The upshot of all this is that retail investors who invest in unit trusts are faced with higher costs but not necessarily better returns than their peers who invest in ETFs tracking the same indices.

The verdict

Which investment is best for your portfolio will depend on your investment goals, time horizons and risk tolerance. If you already know that you want to start investing right away, Syfe allows you to begin investing in global ETFs in Singapore. If you are still on the fence and want to gain a better understanding of an asset allocation that’s suitable for your risk appetite and investment objectives, find out which Syfe portfolio to invest in based on our recommendations.

You must be logged in to post a comment.