Recent signals from the Fed, hinting at potential interest rate cuts as early as September, have sparked considerable interest among investors regarding the potential impact on the Singapore REIT (S-REIT) sector.

Anticipating this potential shift, we hosted an in-person event on 24th July, titled “S-REITs Mid Year Outlook 2024: Approaching A Turning Point?“. The event was a huge success, and we were pleased to have the opportunity to engage with our valued customers and partners on this timely topic.

We’s like to extend our gratitude to our distinguished panelists for sharing their valuable insights:

- Chu Toh Chieh, Co-Head, Fixed Income, Lion Global Investors

- Emelia Tan, Director, Research & Finlit, SGX

If you weren’t able to join us or would like to revisit the engaging discussions, watch the replay here:

Here are five insightful points from the event.

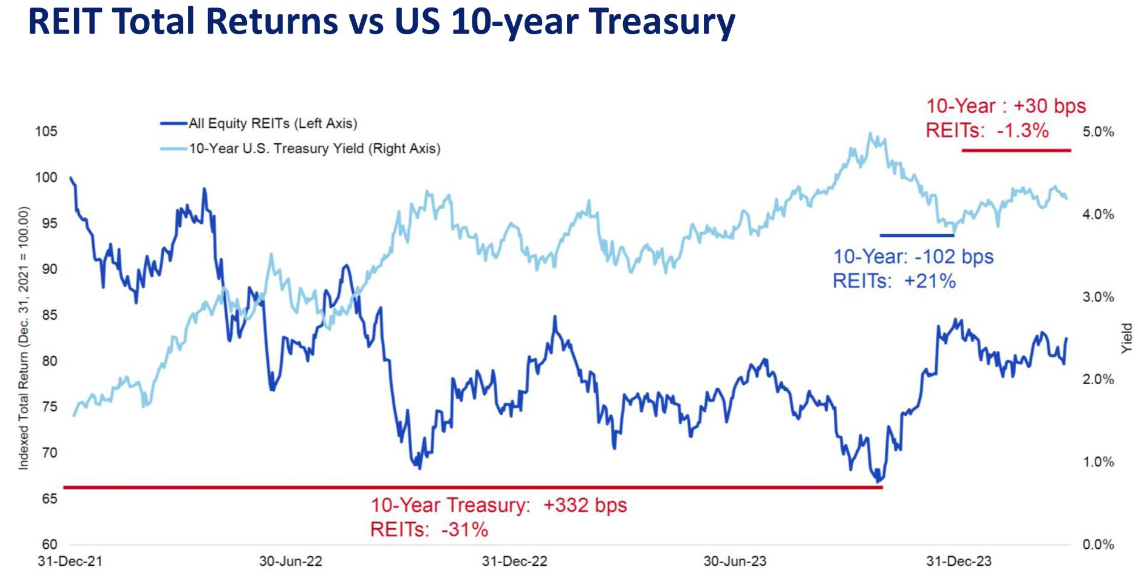

1. REIT total returns are highly correlated with Treasury yield movement

REITs are sensitive to interest rates due to three main reasons:

- Financing Costs: Changes in interest rates directly impact REITs’ borrowing costs, which can influence net profits and the distribution per unit (DPU) available to shareholders.

- Property Valuations: Interest rate movements can affect property valuations through their influence on discount rates used in valuation models, potentially impacting a REIT’s net asset value (NAV).

- Yield Competitiveness: Interest rate adjustments can alter the relative attractiveness of REIT yields compared to other investment options such as government bonds, potentially influencing investor preferences.

Source: NAREIT, SGX, as of 30 June 2024

Unsurprisingly, historical data reveals a strong correlation between Global REITs returns and Treasury yield movements. For example, from late 2021 to mid-2023, when the 10-Year Treasury yield increased by 332 basis points, global REITs experienced a 31% decline. Conversely, in the fourth quarter of last year, when the 10-year Treasury yield decreased by 102 basis points, global REITs rebounded with a 21% return. In the event that interest rates do fall as anticipated, this could favourably impact REIT prices.

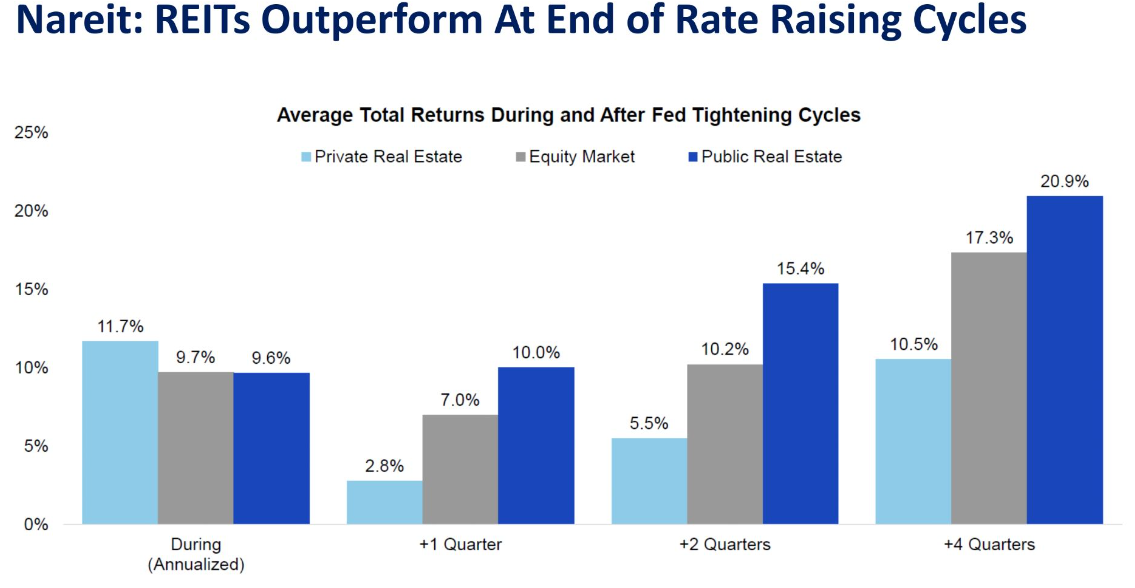

2. REITs tend to outperform at the end of Fed tightening cycle

Source: NAREIT, SGX.

Global REITs have historically outperformed global equities at the end of Fed tightening cycles. On average, in the four quarters following the conclusion of a Fed tightening cycle, public real estate has delivered a 20.9% return, surpassing the 17.3% return of global equities. This historical trend could signal a promising opportunity for investors in the current market environment.

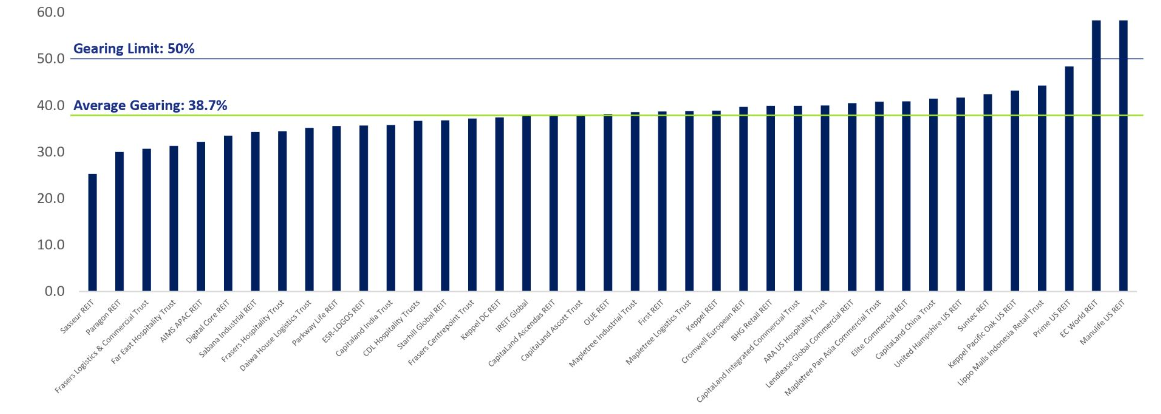

3. S-REITs have healthy balance sheets

Source: Based on Bloomberg data for total assets multiplied by company-related gearing ratio (April 2024). Bloomberg, SGX S-REITs & Property Trusts Chartbook (April 2024)

Overall, the Singapore-listed REITs have strong balance sheets. The average gearing ratio of the 40 REITs listed on the SGX stands at 38.7%, comfortably below the regulatory limit of 50%. The sector’s average interest coverage ratio (ICR) is around 3.8 times, indicating a healthy capacity to meet debt obligations.

Recently, the Monetary Authority of Singapore (MAS) has proposed easing the leverage provisions for S-REITs. All S-REITs are subject to a minimum ICR of 1.5 times, down from the current 2.5 times. These newly revised rulings will introduce more financial flexibility for S-REITs. The measure would enable S-REITs to be more competitive in pursuing acquisitions of attractive properties, which could be positive for dividend growth in the long run.

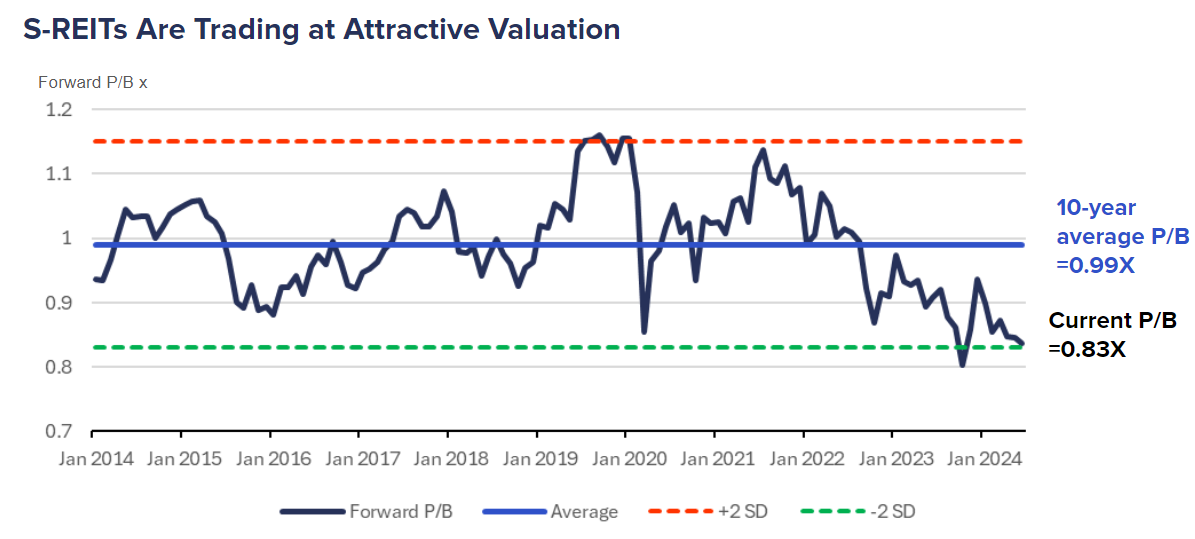

4. S-REITs are trading at almost a 20% discount

Source: FTSE ST REIT INDEX, Bloomberg, data as of June 30, 2024.

Price-to-book (P/B) ratio is a common metric used to assess the fair value of S-REITs. P/B ratio measures how much investors are paying for the underlying properties held by these trusts. The long-term average P/B ratio for the sector is around 1.0x.

Currently, the S-REIT sector’s P/B ratio stands at approximately 0.8x, representing a near 20% discount to the long-term average. This undervaluation could present an opportunity for value-oriented investors, with room for potential rerating as interest rates decline.

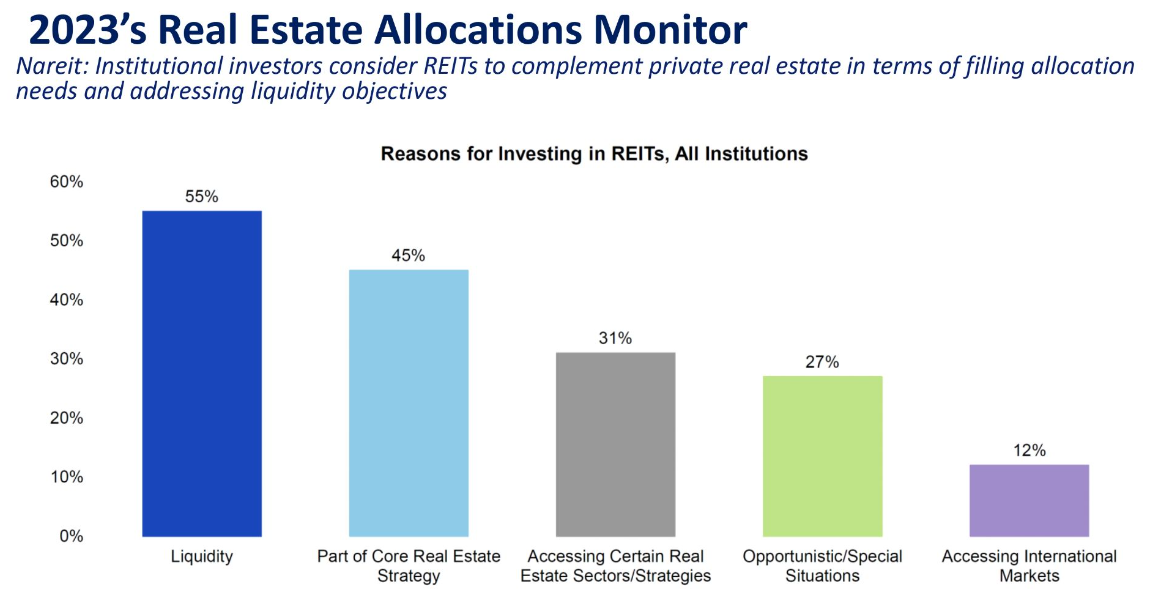

5. Institutional investors come back to REITs when interest rates move lower

REITs are not just for retail investors. Institutional investors often use REITs to complement their private real estate holdings and address liquidity needs. As the interest rate outlook shifts towards a lower rate environment, institutional investors may increase their REIT allocations to capitalise on the changing dynamics.

Source: NAREIT, Cornell/Hodes Weil “2023 Real Estate Allocations Monitor”

Invest in S-REITs through Syfe

We understand that every investor has unique investment styles and preferences. Here are the ways you can gain exposure to S-REITs:

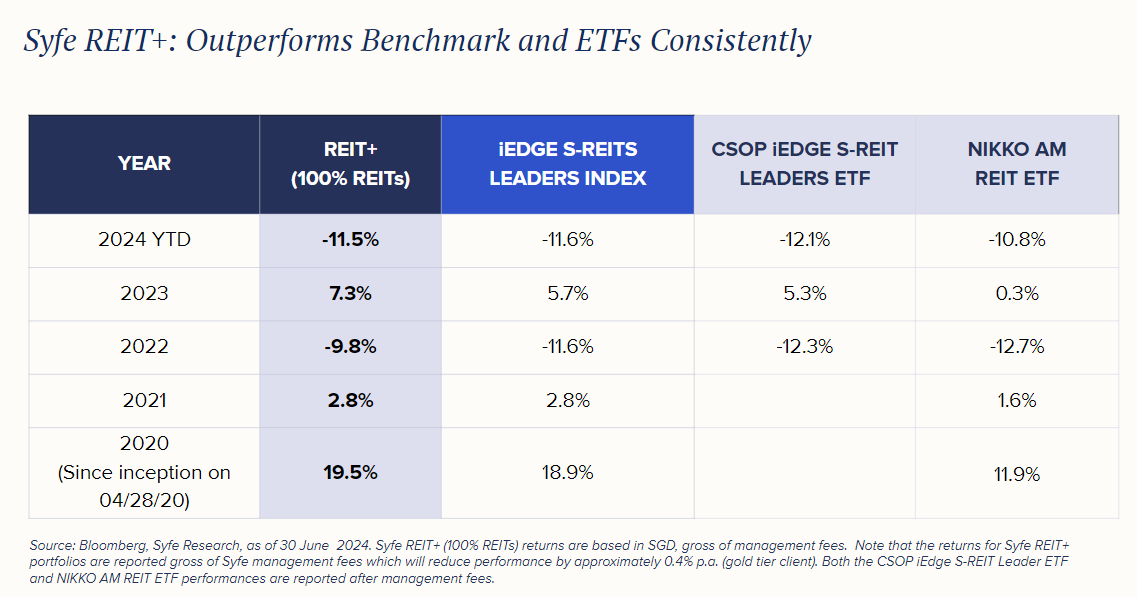

- Syfe REIT+: If you’re looking to gain diversified exposure to S-REITs, Syfe REIT+ is the ideal managed portfolio for you. Through REIT+, you can access the largest and most tradable REITs in Singapore.

Launched in partnership with the SGX, REIT+ is the first investment offering designed to closely replicate the performance of the iEdge S-REIT Leaders Index. This portfolio invests in the top 20 SGD-denominated REITs, selecting those that are liquid, with large market capitalizations, and backed by reputable management teams. Dividends are automatically reinvested to enhance long-term returns, and quarterly dividend payouts are also available. There are no minimums, all brokerage costs are absorbed by Syfe, and overall management fees range from 0.25% to 0.65% per annum.

As a result of the optimisation process, REIT+ has consistently outperformed its benchmark and other REIT ETFs listed on SGX.

- Syfe Brokerage: If you’re looking to gain exposure to individual S-REITs, consider using the Syfe Brokerage platform. It offers attractive fees, with commissions ranging from 0.04% to 0.06%, transparent pricing, and no hidden fees.

Read More: