Singapore REITs have had a tough start in 2024. The expectation that the Fed may delay rate cuts has weighed on sentiments toward S-REITs. However, retail investors have continued to add to S-REITs, taking advantage of below long-term average valuations and attractive yields.

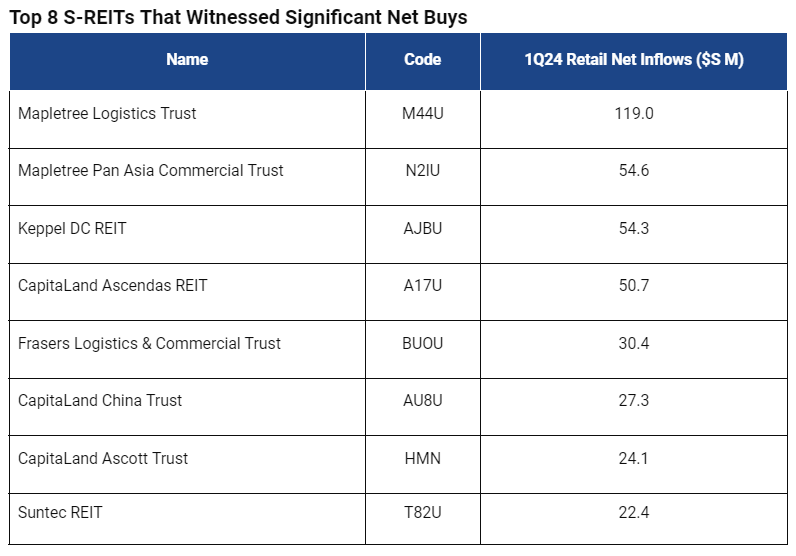

Here are the top 8 S-REITs that witnessed significant net retail buys in Q1 2024, along with their latest developments and earnings updates.

Mapletree Logistics Trust (SGX:M44U)

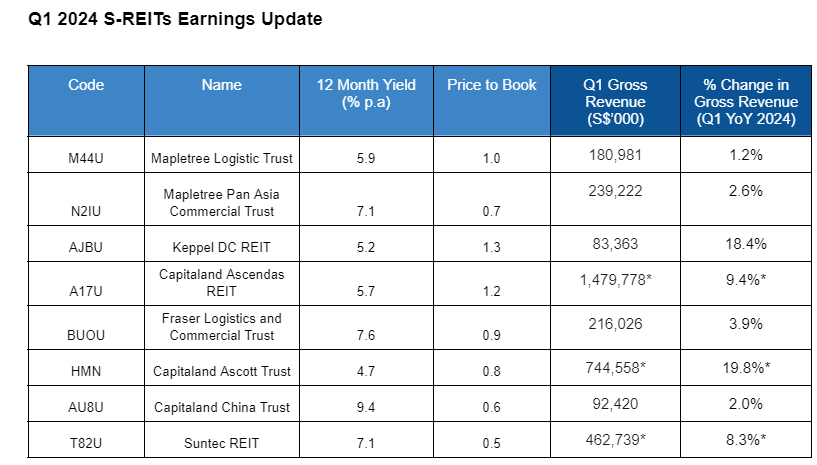

Mapletree Logistics Trust (MLT) reported a 1.2% year-on-year (YoY) increase in gross revenue to S$181 million for the quarter ending March 2024. It also shows a resilient portfolio, with a portfolio occupancy of 96% and an average rental reversion of 2.9%. The increase in gross revenue was mainly due to higher contributions from existing properties in Singapore and Hong Kong and acquisitions in Japan, South Korea and Australia completed in 1Q FY 23/24. Foreign currency forward contracts were also used to hedge the foreign-sourced income distributions, partially mitigating currency fluctuation. This partly offsets the lower contribution from existing properties mainly in China, absence of revenue contribution from divested properties and depreciation of foreign currencies against SGD assists in the moderation of the growth.

Mapletree Pan Asia Commercial Trust (SGX:N2IU)

Mapletree Pan Asia Commercial Trust (MPACT) reported gross revenue and net property income (NPI) climbed 2.6% and 3.2% YoY to S$239.2 million and S$183.1 million, respectively. The growth was mainly driven by the solid performance of the Singapore assets and stable contribution from Festival Walk. Despite a stronger Singapore dollar weighing on overseas income, the overall growth in NPI more than covered higher finance costs for the quarter. Consequently, DPU rose 1.8% YoY to 2.29 Singapore cents. Additionally, MPACT shows positive full-year rental reversion of 2.9% and improved committed occupancy to 96.1%, emphasising health occupancy and rental income.

Keppel DC REIT (SGX:AJBU)

Keppel DC REIT reported a 18.45% increase in gross revenue to S$83.4 million in Q1 2024. Higher gross revenue in 1Q 2024 mainly due to settlement sum received in relation to the dispute with DXC and positive reversions and escalations. However, distributable income and Distribution per Unit (DPU) decreased by 16.3%, to 46.3 million and 13.7% to 2.192 cents respectively, mainly due to higher finance costs and less favourable forex hedges in 2024.

Capitaland Ascendas REIT (SGX:A17U)

CapitaLand Ascendas REIT reported a 9.4% increase in gross revenues to S$1,479.8 million, attributed to acquisitions completed in 2023. Occupancy rates for retail, office, and integrated development properties stood at 94.2%. This led to a positive average rental reversion of 13.4%, resulting in a marginal 5.6% YoY growth in net property income to over S$1 billion. Additionally, DPU increased by 3.5% YoY due to the increase in NPI and the absence of the Managers’ performance fee.

Frasers Logistics & Commercial Trust (SGX:BUOU)

Frasers Logistics & Commercial Trust reported a 3.9% increase in revenue as well as a 1.8% increase in adjusted NPI. The increases were due to positive rent reversions and rental escalations, and contributions from Ellesmere Port, Connexion II and Worcester. These were partially offset by higher vacancies in commercial assets and higher property operating expenses.

Capitaland Ascott Trust (SGX:HMN)

CapitaLand Ascott Trust recorded an 19.8% increase in gross revenue to S$744.5 million, attributed to higher revenue from existing portfolio and new acquisitions. Occupancy rates rose from 68% to 78%. In 2023, Distribution per Stapled Security (DPS) increased by 16% YoY to 6.57 Singapore cents, reflecting strong performance and asset acquisitions. CLAS’s balanced portfolio enables it to seize growth opportunities while maintaining resilience.

Capitaland China Trust (SGX:AU8U)

CapitaLand China Trust initially showed a 1.6% decrease in gross revenue to $89.2 million for Q1 YoY as only 9 retail malls led to recovery compared to 11 retail malls in 1Q 2023. For equal comparison, excluding CapitaMall Shuangjing and CapitaMall Qibao’s contribution in 1Q 2023, retail gross revenue would have increased by 5.7% YoY and 1Q gross revenue would increase by 2.0% to $92.4 Million. There is also a 7.7% decrease in NPI to $59.7 million. This would be due to lower contributions from logistics parks and absence of one-off property tax refund from business parks led to the decrease in NPI. Additionally, the decline further increased to 11.8% YoY partially due to 4.7% YoY depreciation of RMB to SGD.

Suntec REIT (SGX:T82U)

Suntec’s gross revenue increased by 8.3% to S$462.7 million, while net property income decreased slightly by 0.8% to S$313.1 million YoY. Higher contributions from Suntec City Office, Suntec City Mall and Suntec Convention along with The Minster Building (London) played a part in the increase in gross revenue. Higher maintenance fund contribution, commencement of sinking fund contribution in 2023 and lower contribution from Australia portfolio, are some of the reasons for the decrease in NPI. Investors will also received lower dividends this quarter, as distributable income declined by 19.1% to S$206.8 million and DPU dropped by 19.7% to S$0.07135 compared to the previous year, primarily due to increased financing costs, lowered contributions from the overseas properties and a weaker AUD against the SGD.

Is now the time to invest in S-REITs?

Contrary to the widespread pessimism in the market, operations of S-REITs have stayed resilient in 1Q 2024. Most S-REITs, in the latest quarterly results or latest available results, have shown signs of healthy occupancy rates and rental revision. For instance, Mapletree Pan Asia Commercial Trust not only maintained high portfolio occupancy but also improved the rate to 96.1%, thanks to proactive management efforts. Capitaland Ascendas REIT also maintained a healthy occupancy rate at 94.2%, leading to positive rental reversion of 13.4%. Overall, S-REITs have demonstrated their ability to generate stable, visible and durable cash flows from their underlying assets despite the macro headwinds.

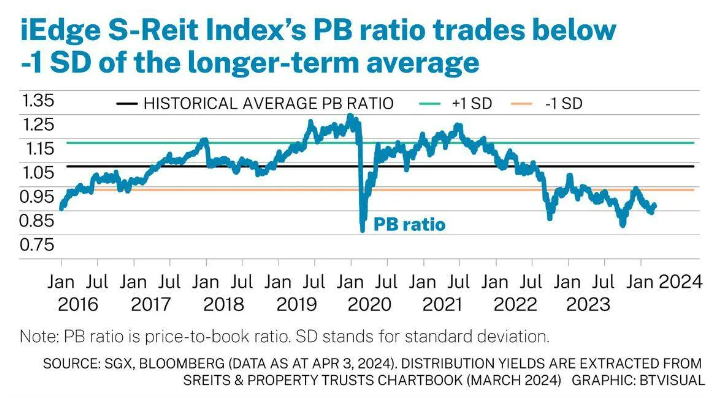

Currently, S-REITs are trading at attractive valuations, with price-to-book ratio of the iEdge S-REIT Index at 0.85X, nearly 20% below its longer-term average. The 12-month dividend yield is close to a healthy 6%. Combined with increased gross revenues and net property income, this suggests that S-REITs might be undervalued

Focus on Quality and Diversification

In the near term, sentiment towards S-REITs may remain soft as the market reprices for a “higher-for-longer” interest rate environment. However, for investors looking to build passive income for the long run, this could be an opportunity to buy into the S-REITs with quality assets at attractive entry prices. They stand to benefit when rates eventually come down.

It is advisable to invest in a portfolio of quality S-REITs, such as REIT+. With a diversified portfolio, the poor performance of a single REIT will have a much smaller impact on your overall portfolio returns. This also helps you avoid the risk of being overexposed to any one REIT.

If you are eager to accumulate more REITs at the current attractive prices, consider adopting a dollar-cost averaging (DCA) strategy. For example, you could choose to invest $1,000 into your Syfe REIT+ portfolio each month. This approach allows you to buy more at lower prices during market dips while minimising the risk of deploying all your cash should the market decline further.

Read More:

Answer Your Top Three Investing Questions: Q2 2024 Investment Outlook

FOMC Update: What Do “Higher For Longer” Interest Rates Mean for Your Money?

You must be logged in to post a comment.