Highlights:

- In the May FOMC meeting, the US Federal Reserve (the Fed) sent mixed signals. It held its benchmark interest rate steady at a 23-year high of 5.25% to 5.5%, marking the sixth consecutive meeting where rates remained unchanged.

- Acknowledging the stubborn inflation, the Fed hinted that borrowing costs could remain at the same level for a longer period, but a rate hike is unlikely.

- As the Fed maintains the stance of keeping interest rates at relatively high levels to manage inflation, the policy may affect your personal finance in various ways—from loans to investments.

What Happened?

In the May FOMC meeting, the Fed sent mixed signals. It held its benchmark interest rate steady at a 23-year high of 5.25% to 5.5%. This marks the sixth consecutive meeting for the Fed to keep interest rates unchanged.

Acknowledging the stubborn inflation, the Fed hinted that borrowing costs could remain at the same level for a longer period of time. That said, Fed Chair Jerome Powell also highlighted that an interest rate hike is unlikely. This shows that the bar for the Fed to hike rates again remains very high, as we discussed in the Q2 Outlook.

Another focus is on the Fed’s balance sheet reduction or quantitative tightening (QT). The Fed is planning to taper its QT program, and the process can start as early as June. This aims to maintain financial stability.

Overall, this FOMC meeting showed that the Fed is taking a more measured approach to its monetary policies. The careful tapering of QT is essential for the economy to sustain the recovery without disrupting the financial system.

The Immediate Market Reaction

Assets generally reacted positively to the news. After the Fed’s announcement, the market is pricing in two rate cuts this year, with the first rate cut to start in September, according to the CME FedWatch Tool.

Bonds stabilised as US Treasury yields declined. The US 10-Year Treasury yield pulled back from 4.69% to 4.59%, while the US 2-Year Treasury yield retraced to below 5%.

Meanwhile, US stocks staged a rally on Thursday after initial mixed reactions.

What Could “Higher for Longer” Interest Rates Mean For Your Money?

As the Fed maintains the stance of keeping interest rates at relatively high levels to manage inflation, the policy may affect your personal finance in various ways – from loans to investments.

Loans and Mortgages

The “Higher for Longer” environment may not be kind to borrowers. The cost of borrowing, including mortgages, car loans, and other personal loans, could remain high for an extended period. The financing costs can significantly impact your monthly budget. It is important to properly plan out your budget and not over-leverage based on the hope that interest rates will be lower soon.

Saving and Deposit

Cash management tools still offer attractive yields. However, it’s important to note that the Fed may delay rate cuts but is unlikely to increase rates, suggesting potentially lower rates around the end of this year and next year.

To take advantage of the current attractive rates, consider locking in cash that you don’t need in the immediate term in fixed deposit products with longer maturity terms. This approach helps reduce reinvestment risk—that is, the risk of receiving a lower return after the term matures.

We have introduced Cash+ Guaranteed for 6 months and 12 months, which offer 3.75% p.a. and 3.7% p.a., respectively, as of 2 May 2024. You may want to consider allocating part of your spare cash to lock in these attractive interest rates.

For your cash that you can put aside for your long term goals, it is advisable to allocate to investments. Historically, even in a high interest rate environment, bonds and equities have consistently provided superior returns over the long term compared to cash.

Investments

Some investors may associate “higher for longer” environments with negative investment returns. This may not necessarily be the case. During the 1990s, when interest rates remained high for an extended period, the S&P 500 delivered returns above 10% per annum, and US Treasuries returned 6.3% per annum. Similarly, the current “higher for longer” era could produce decent investment returns.

- Equities: The overall impact on equities depends on the reasons behind the interest rates staying at high levels. If the main driver is improved economic conditions, the negative effects of increased financing costs could be offset by stronger corporate earnings.Currently, the economy in the US has remained relatively robust, and earnings growth is healthy. A diversified portfolio such as Core Equity100 could benefit more in this environment, as the equity rally begins to expand from US tech to other sectors and regions.

- Bonds: In the short run, bond prices may be negatively impacted as the market is repricing for fewer rate cuts. However, over the long run, “higher for longer” interest rates can benefit bond investors, as investors can secure attractive and predictable future cash flows. Our bond portfolios, Syfe Income+ Preserve and Enhance, offer yields to maturity of 6.2% and 7.4%, with monthly payouts of 4%-5% p.a. and 5.0%-6.0% p.a. respectively.

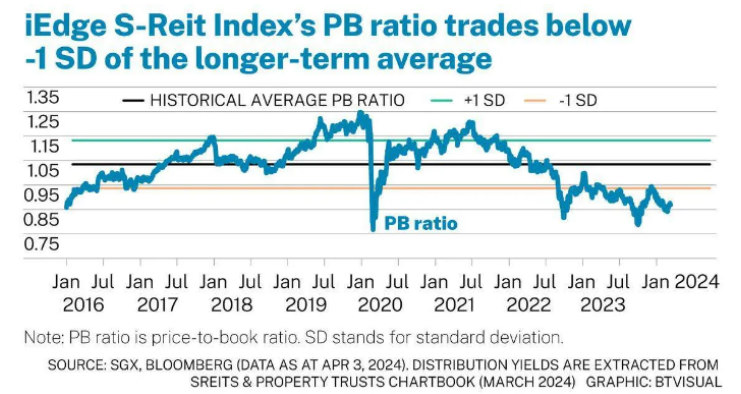

- S-REITs: We recommend investors be more selective with S-REITs, due to potential higher refinancing costs if interest rates remain elevated. A large part of the interest risks could have already been reflected in the price. The price-to-book ratio of the iEdge S-REIT index is around 0.87X, close to 20% below the long-term average.

If you look to take advantage of the recent selloff in S-REITs while managing risk, our REIT+ (100% REITs) portfolio is well positioned. It is composed of the top 20 SGD-denominated REITs, screened based on liquidity, market capitalisation, and reputation of the management teams. The REIT+ portoflio focuses on higher quality REITs and allows investors to gain diversified exposure to the S-REIT sector.

Read More: