Singaporeans are known to be good at saving. According to the Department of Statistics Singapore, our personal savings rate was 35.2% in the fourth quarter of 2023. On the other hand, investing could be less familiar to many. Both saving and investing are important pillars in building a sound financial foundation, but they are not the same. Here are the differences between saving and investing, and why you should employ both strategies to build your wealth.

Saving vs Investing, what’s the difference?

Everyone knows what it means to save—to set aside money, readily available for future purposes. Saving is predictable and safe, knowing exactly where your money is and how much interest you are earning.

When you invest, you put your money into assets with the expectation that the value of the assets will increase over time. Some of the typical financial instruments and schemes include stocks, bonds, mutual funds, and exchange-traded funds (ETFs). Compared to saving, investing comes with higher risk, but you are also given the opportunity to accumulate and increase the value of your assets over time.

The decision between saving and investing depends on your risk tolerance and the time you have to achieve your financial goals. As a rule of thumb, for short-term financial goals, savings might be more suitable. For example, if you are planning your wedding next year, you are recommended to put your money into savings rather than investing.

For your long-term financial goals, ranging from retirement plans to paying for children’s education, investing could be more fitting. Investments have the potential to grow your wealth at a faster rate than the relatively low interest rates that saving provides, thereby preparing you for your plans in the future.

Saving vs Investing, which is more risky?

Many individuals are afraid of investing due to the fear of loss of capital. With the price swings, one might see their investments in red for a period of time. This leads many to stick to their roots of a safer and secure route – saving. However, leaving your money in bank accounts can actually carry a greater risk over the long term.

The value of your money can be eroded by inflation

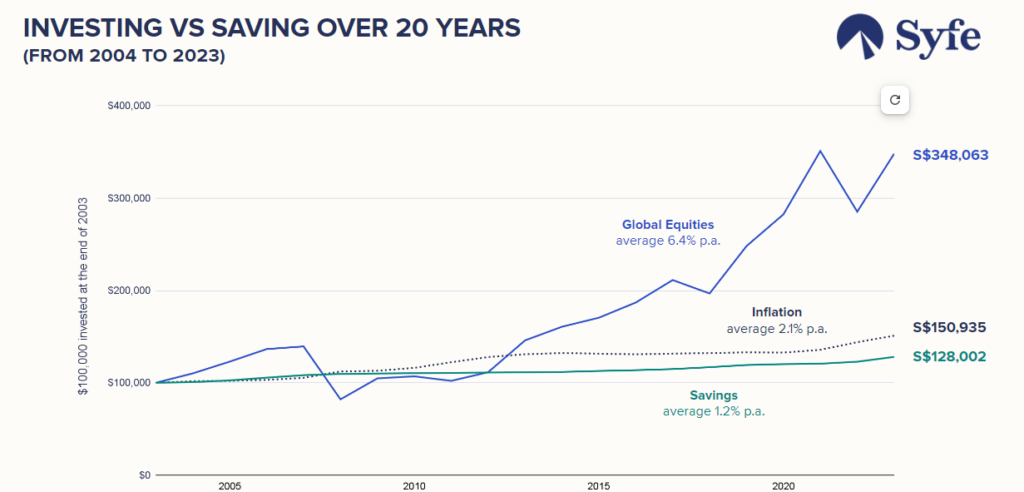

If one chose to put S$100,000 in a bank account at the start of 2004, within a span of approximately 20 years, one would get back $128,000, with an average interest of 1.2% p.a. However, with an average of 2.1% p.a. increase in inflation, the basket of goods that you could purchase for $100,000 back in 2004 would cost around S$151,000 now. Essentially, as the inflation rate clearly outpaces the returns in your savings account, the purchasing power of your money has been eroded.

Miss out the opportunity for higher returns

On the flip side, if an individual chooses to invest the same amount in global equities back in 2004, the investment portfolio would have grown to S$348,063, more than three times the amount initially invested. This would come with an average return of 6.4% p.a in SGD. Though the amount invested is subject to high volatility, it has much higher returns compared to saving.

Imagine two people with the S$100,000 set aside for their retirement in 2004, one chose to save in a bank account and one chose to invest in global equities; both will have very different values for their retirement funds 20 years later (S$128,000 vs S$348,000). Not investing may result in you not meeting your important financial goals, which could be a bigger risk in the long term.

The Bottom Line

Both saving and investing are important for building your wealth. How much you set aside for saving and investing depends on your goals, risk tolerance and time frame.

While investing may seem complex, in Syfe we try to simplify the process of investing. We offer four Core portfolios, designed to address some of the most important customer goals in life, from purchasing their first home to educating their children, and retiring comfortably.

Here’s a quick guide to help you understand which portfolio is right for you.

- Core Defensive is a low-risk portfolio that’s ideal for conservative investors, or those approaching a particular financial goal

- Core Balanced is a medium-risk portfolio that’s ideal for moderate investors with a mid-to long-term horizon

- Core Growth is a high-risk portfolio that’s ideal for growth-oriented investors with a longer time horizon

- Core Equity100 is a 100% equity portfolio that’s ideal for investors who are comfortable taking on higher risk for potential higher long-term returns

Syfe Core portfolios have no minimum investment amounts and no lock-ins. You can set up as many Core portfolios as you prefer based on your goals. For example, you may invest in Core Growth for a long-term goal like retirement and choose Core Defensive for a shorter term goal such as a house downpayment.

Ready to invest in Core portfolios?

You must be logged in to post a comment.