So far, 2024 has been a dynamic year for China’s equity markets. In January, a derivative-induced meltdown sent Chinese stocks lower on the Shanghai and Shenzhen Stock Exchanges, spilling over to Hong Kong and US-listed China ADRs. But things may be looking up for China’s stocks.

Since February 2nd and through the end of April, the Shanghai Composite Index has returned +12.2% and the Hang Seng Index has returned +13.2% versus the S&P 500’s 1.90% and the Nasdaq 100’s -0.95%.Can this rally sustain itself? In this article, Brendan Ahern, Chief Investment Officer from KraneShares, shares five key points for investors to consider as to why this breakout may be fundamentally different from previous rallies.

Table of Contents

1. The government is buying stocks and talking about it.

China’s government is buying Mainland stocks to stabilise the domestic stock market and influence stock market indices. In the past, government buying was done discreetly without much publicity, this time China is being much more public with its stock purchases.

One such buyer is Central Huijin Investments, an entity within China’s sovereign wealth fund. The state-linked entity announced purchases of Mainland China-listed ETFs in February and subsequently increased its holdings of Mainland bank stocks in April, according to its quarterly reports.

State-linked stock buyers are common in Asian markets and their activity can shore up investor confidence. Japan’s central bank, for example, has a long history of buying stocks and ETFs listed on Japanese exchanges. We believe that investors are overweighting Japanese equities due to the government’s purchase of equity ETFs and ongoing corporate reforms. This similar recipe of equity investing success is being replicated in China as state-linked funds buy Mainland -listed mega-cap stocks and ETFs that, in turn, influence the stock indices.

2. Global investors are returning.

January’s fall was partly due to investors’ neutral or under-weights to Chinese equities. US investors were among the first to shed their China positions due to the Trade and Technology Wars, followed by China’s internet regulatory cycle and zero COVID policy. Next, European investors trimmed their positions after the geopolitical uncertainty that unfolded following Russia’s invasion of Ukraine. Asian investors eventually followed suit, though they were slower to reduce their exposure due to their proximity to China’s economic orbit. Finally, local Chinese investors divested from Mainland stocks much later, following the derivative-induced selloff earlier this year.

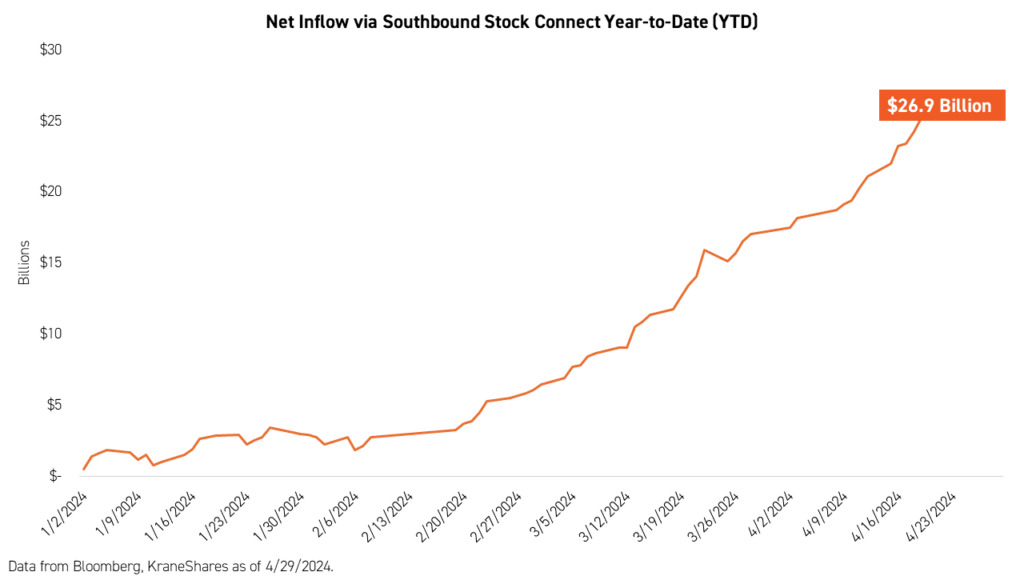

We suspect re-allocations to China’s equity market could occur in the opposite order as local Chinese investors return first, followed by Asian investors and then European and American investors.

Southbound Stock Connect (the mutual market access program that permits Mainland investors to invest in Hong Kong-listed stocks) flows from Mainland China into Hong Kong stocks show that local Chinese investors have already started to return, at least to offshore stocks.

At the same time, we believe many Asia-focused investors who have been overweighting India and Japan are growing concerned about India’s high valuations and Japan’s continued currency weakness. China’s equity market could be a beneficiary of investors moving profits from high-valuation markets to low-valuation markets.

3. New policy supports shareholders.

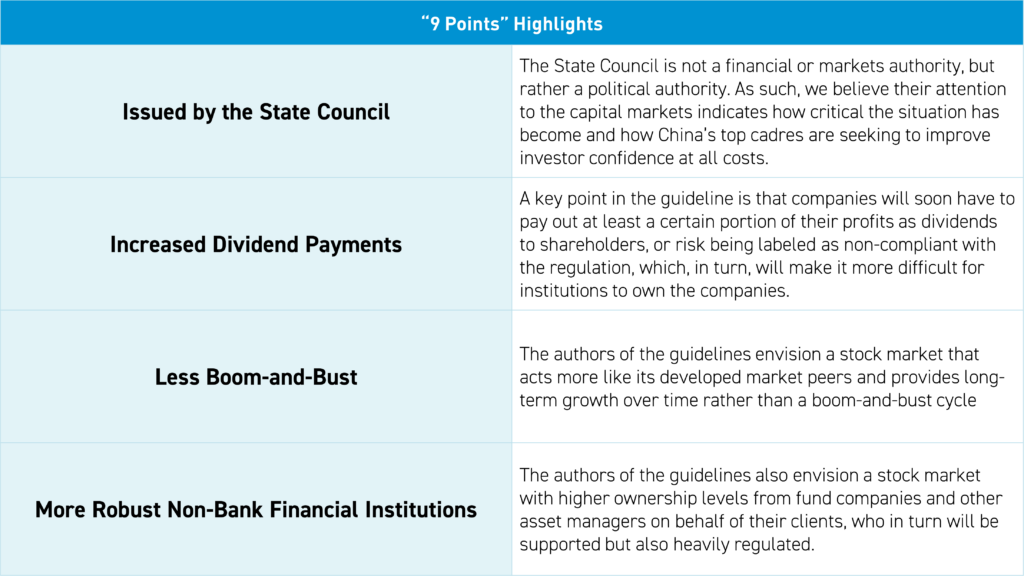

On April 12, The State Council issued “9 Key Points” to improve China’s capital markets, a rare document to come out of the State Council, China’s top political body (like the President’s cabinet in the US), which usually does not comment on markets. Among the measures are initiatives to control the supply of IPOs, encourage companies to pay dividends and improve their corporate governance, and promote bank and trust products to allocate more to equities.

4. The consumer is alive and the economy is improving.

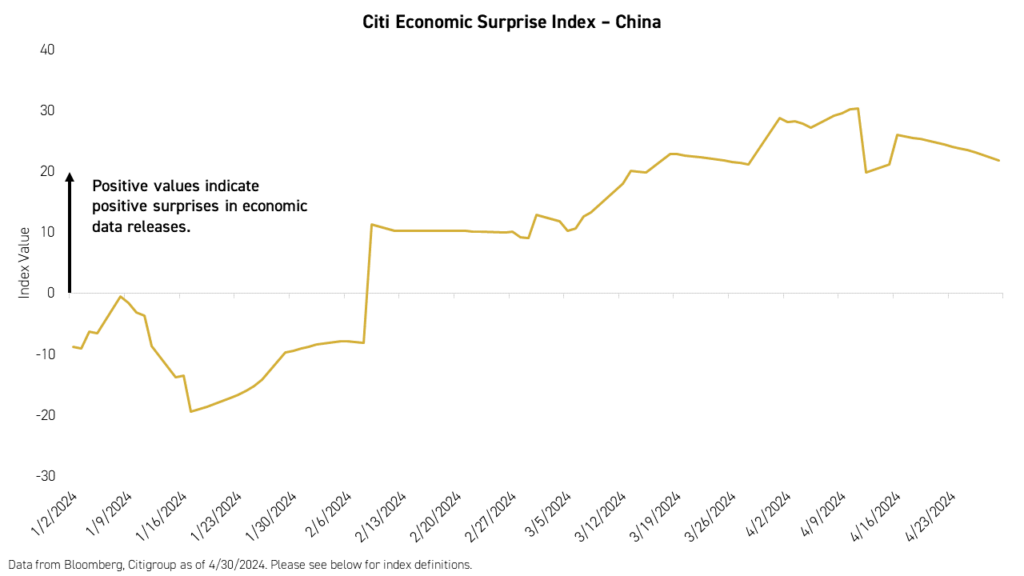

China’s economic cycle is improving, as evidenced by Q1 2024 GDP, which came in at 5.3% versus an estimated 4.8%, representing an improvement of +1.6% compared to Q4 2023.4 The Citi Economic Surprise Index measures the degree to which economic releases in a given country surprise to the upside or downside. The China index has moved up steadily since the start of the year after declining in 2023. Although expectations for these releases were already low, the index indicates a general upward trend starting in January.

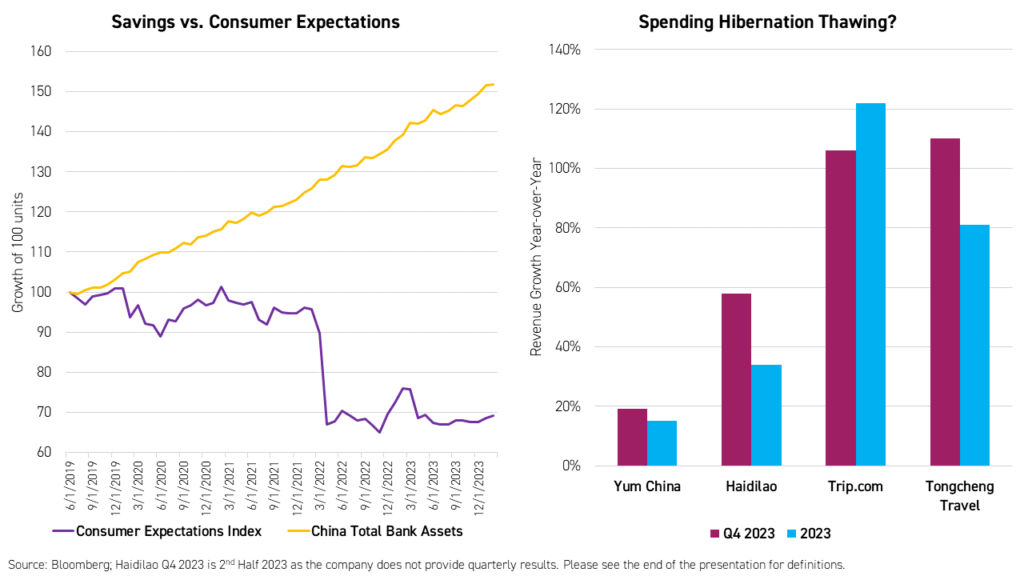

Consumer confidence is slowly improving, though Chinese households maintain their high historical savings rate. Unleashing these savings would likely produce a significant economic boost. Consumption is rebounding, but it continues to be concentrated in services such as travel, which was reflected in the Q4 2023 financial results from restaurant chains and travel agencies.

Policy support for consumption has been incremental, though support is starting to accelerate. Following the “Two Sessions” in March, the government announced increased incentives for the upgrading of large items such as automobiles and home appliances.This indicates the government’s keen interest in seeing the economy recover.

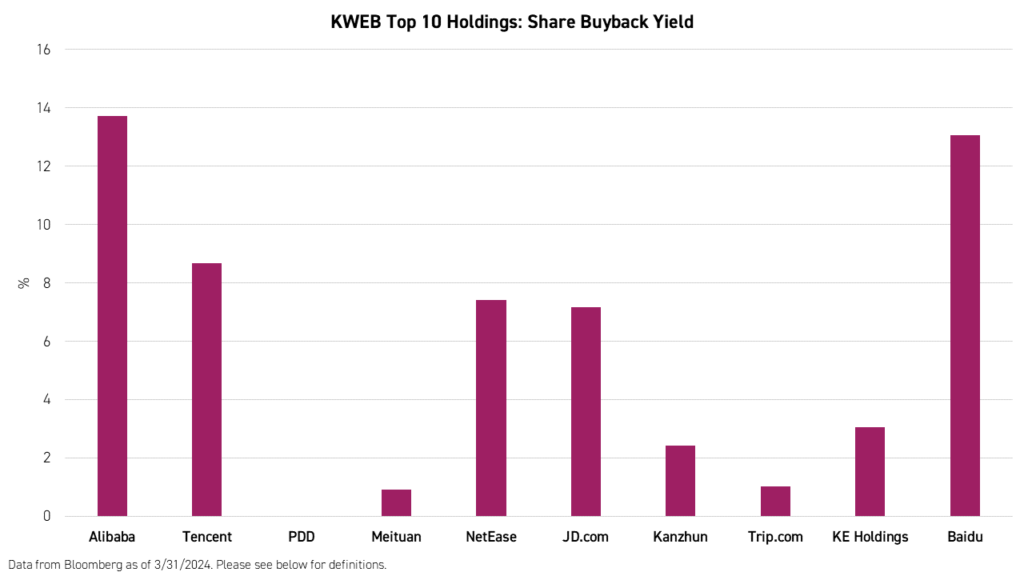

5. Present valuations cannot be ignored, and buybacks are surging.

Low valuations paired with improving earnings could be a catalyst for continued outperformance in certain sectors in China. Although some investors have yet to recognize the attractive valuations in China equities, many companies are taking the matter into their own hands by buying back their stock, mostly in the internet sector.

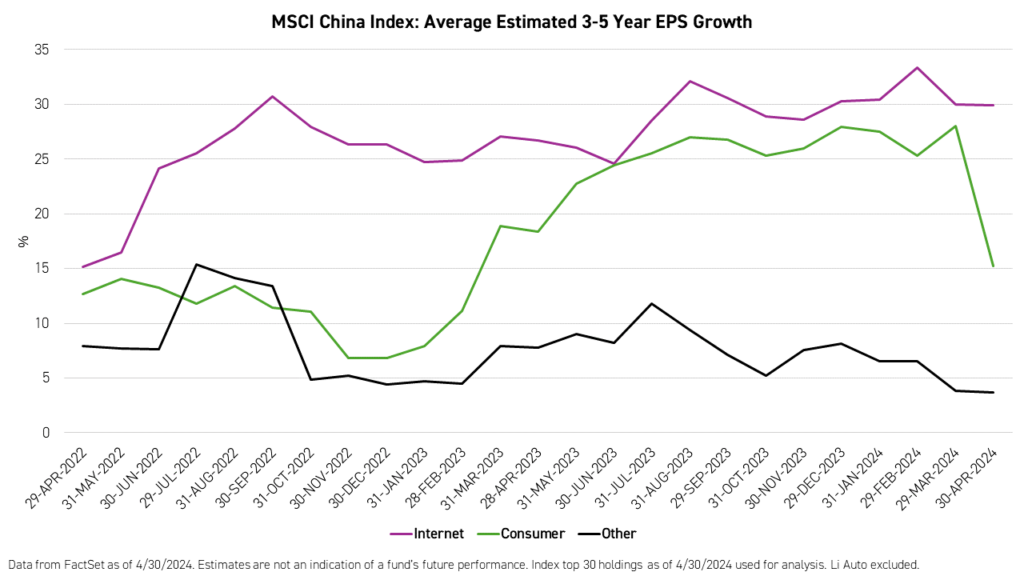

At the same time, the fundamentals for these companies are also improving. The 3 and 5-year earnings per share (EPS) growth estimates for the internet and E-Commerce companies within the MSCI China Index have been upward trending over the past two years and are currently multiples higher than broad consumer stocks and the average for other industries within the index.

Risks of investing in Chinese equities

Before you get too excited about Chinese equities, we also would like to highlight some risks of investing in Chinese equities. Chinese equities tend to be volatile, especially for mainland Chinese stocks. Local retail investors, who trade more often and generally have short-term outlook, account for more than 80% of trading volumes in the A-share market. Meanwhile, the property market continues to struggle, which can make China’ economic recovery bumpy.

As such, it is crucial to be cognizant of your allocation when considering Chinese equities and to consider buying in batches to mitigate risk and capture potential upside at different market points.

How to Invest in Chinese equities?

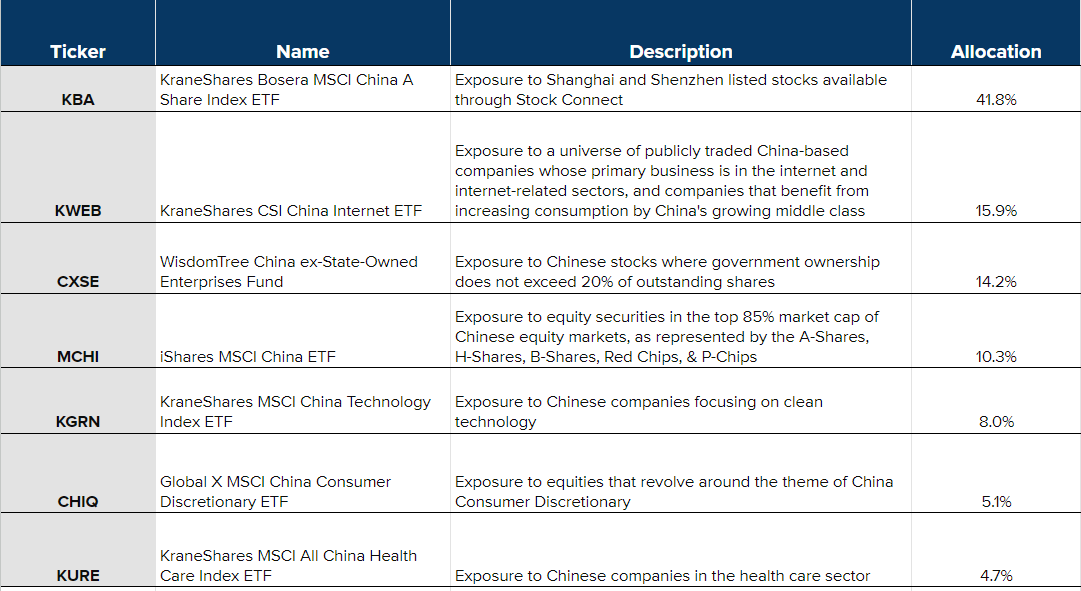

For investors looking to invest in China, Syfe’s China Growth portfolio is one way to take advantage of the currently attractive valuation of the Chinese equities . Our China Growth portfolio, powered by KraneShares, aims to capture the structural growth trends in China. The portfolio focuses on China’s new economy sectors – including innovation and technology, healthcare and clean tech.

There is no minimum investment, no lock-in period and no brokerage fees. As an added advantage, Syfe will manage your portfolio with free dividend reinvestment and automatic rebalancing. Invest in China growth stocks today with Syfe.

Note: In collaboration with KraneShares, we have modified this content for our audience: 5 Reasons China’s Recent Stock Market Rally is Fundamentally Different.

Read More:

Investment Strategy | Syfe China Growth, Powered by KraneShares