The original version of this article was firstly published in Business Times.

Ritesh Ganeriwal, Managing Director and Head of Investment and Advisory at Syfe, explained why ‘higher for longer’ interest rates have created market conditions that make now a great time for savers to become investors.

Savers have been spoilt for choice over the last couple of years. Adoption of money market funds and other alternative cash instruments flourished as interest rates rose. Banks responded with eye-watering headline savings rates to woo customers back.

But with the US Federal Reserve indicating rate cuts once inflation comes under control, and with many Singapore banks already trimming savings rates, the party for savers seems to be coming to an end.

The big question is when. A recent poll found that two thirds of economists expect two rate cuts this year, starting in September, but the Fed will keep rates in the ‘higher for longer’ default until it sees inflation targets being met. The good news is that markets cannot fully price-in lower interest rates without more certainty, so for now there are some very attractive investment options available.

Too much of a good thing

Preparing for lower interest rates is not the only reason to consider investing. After such a long period of high interest rates, many people are now hoarding cash well beyond their emergency funds and near-term cash needs. This has yielded some decent returns, but not enough to beat inflation in the long term. In fact, inflation over the last five years totalled around 15%, whilst savings over that period would only have yielded around 10%. Looking at the last 20 years the picture is even more stark, as savings would have grown around 20% against inflation of over 50%.

The potential for lower interest rates also increases the risk that savers may not be able to reinvest their returns at the same rate. Instead of cash, investors should consider investments such as bonds and equities, which can deliver higher returns over the long term.

Attractive prices and high yields, for now

Many savers are waiting for interest rates to drop further before exploring other investments, hoping to squeeze what they can from cash instruments. This could be a mistake, as any returns could be far outweighed by missed opportunities in a number of asset classes.

For instance, bond prices are now at attractive levels, whilst bond yields are near 15-year highs. Since bond prices have an inverse relationship with interest rates, prices could benefit when the Fed starts to cut rates. Investing now, before interest rates normalise, would give investors the double benefit of potential price appreciation while locking in comparatively high yields for passive income.

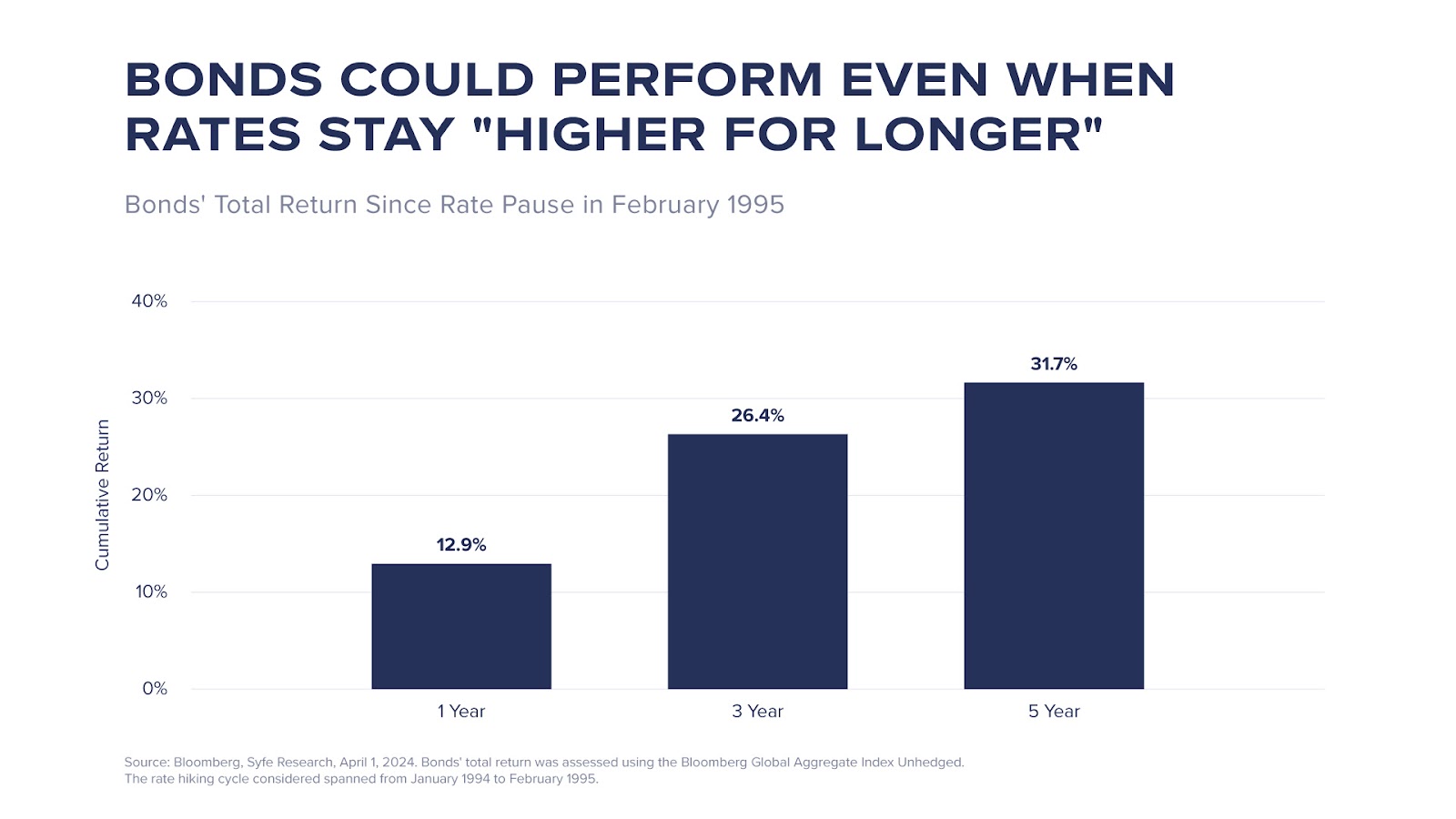

Even in a scenario where interest rates stay ‘higher for longer’, bonds can still generate attractive returns. Looking back to the 1990s, the US central bank, after pausing rate hikes in February 1995, maintained a high Fed funds rate until the end of 1998. During this period, bonds delivered a total return of 26.4% over three years and 31.7% over five years.

Source: Bloomberg, Syfe Research, April 1, 2024. Bonds’ total return was assessed using the Bloomberg Global Aggregate Index Unhedged. The rate hiking cycle considered spanned from January 1994 to February 1995.

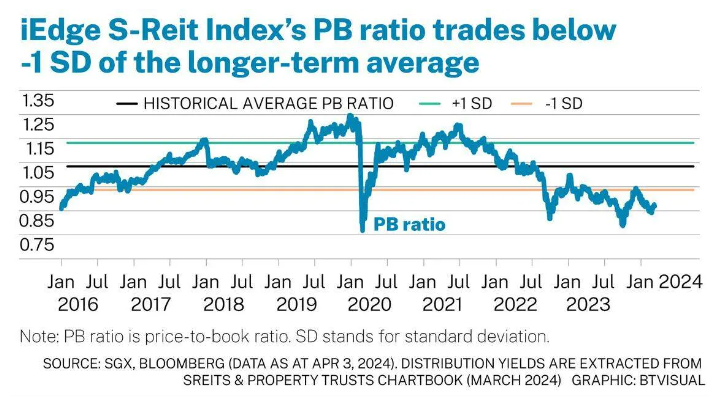

Real Estate Investment Trusts (REITs) present a similar set of potential benefits, although it’s important to note that REIT prices and yields are more volatile than bonds.

REITs combine real estate investment with steady returns in the form of dividends, making them a popular choice in Singapore. Singapore REITs (S-REITs) have struggled in recent years amidst high borrowing rates, but they stand to benefit when rates eventually come down.

Price-to-book ratio is currently trading 20% below its longer-term average, suggesting S-REITs might be undervalued, whilst 12 month dividend yields are close to a healthy 6%.

Equities still best for growth

For those who can invest on a longer time horizon, a diversified portfolio including equities is still the best route to growth.

Equities are expected to do well when rates fall, as lower borrowing costs will make it cheaper for companies to service their debts and finance growth, in turn boosting profitability and valuations.

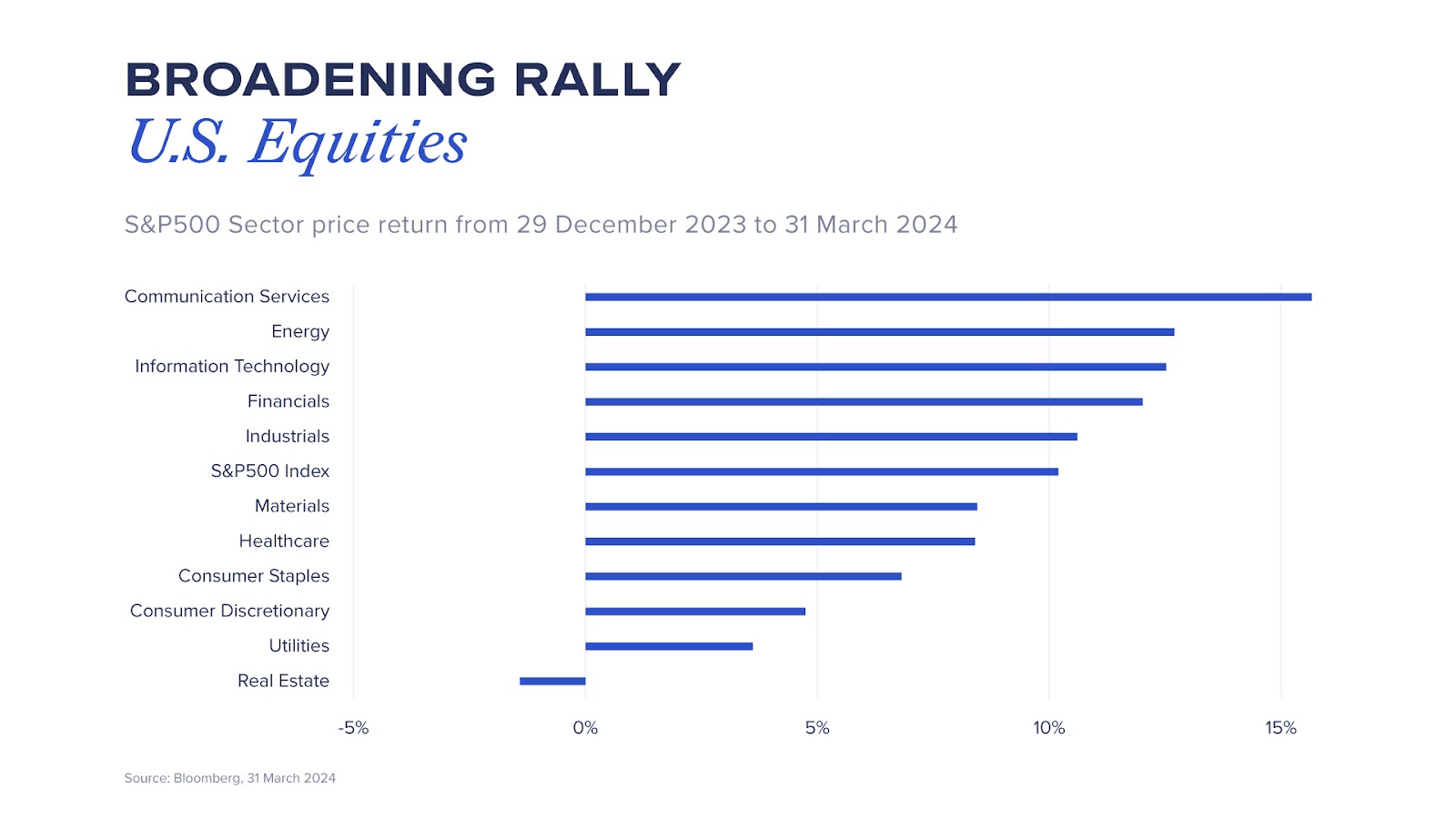

The rally in US equities has been widely discussed and some have even questioned if we are in a bubble, similar to the dot com bubble of the 1990s. The S&P 500 did perform very strongly in 2023, but it’s important to note that over 70% of the index’s returns came from the “Magnificent 7”. This year tech stocks are still leading, but we are seeing the rally broaden out to other industries, such as financials, energy and industrials. Considering that 87% of companies in the S&P 500 beat expectations in Q1, the signs indicate a healthier, more balanced market environment.

To capture upside potential whilst managing concentration risk, diversification is key. We recommend equal-weight ETFs over market-cap-weighted ETFs, as this will help avoid overexposure to any group of stocks, as well as including quality and defensive equity sectors such as healthcare, utilities and consumer staples. Investors can also consider adding safe-haven assets like gold as an extra hedge against market volatility.

The party for savings might not be over yet, but you may want to look for a taxi before the prices go up.

You must be logged in to post a comment.