Core Equity100, Syfe’s all-equity portfolio, is a smart beta portfolio built using a multi-factor methodology. In recent years, smart beta investing has become increasingly popular.

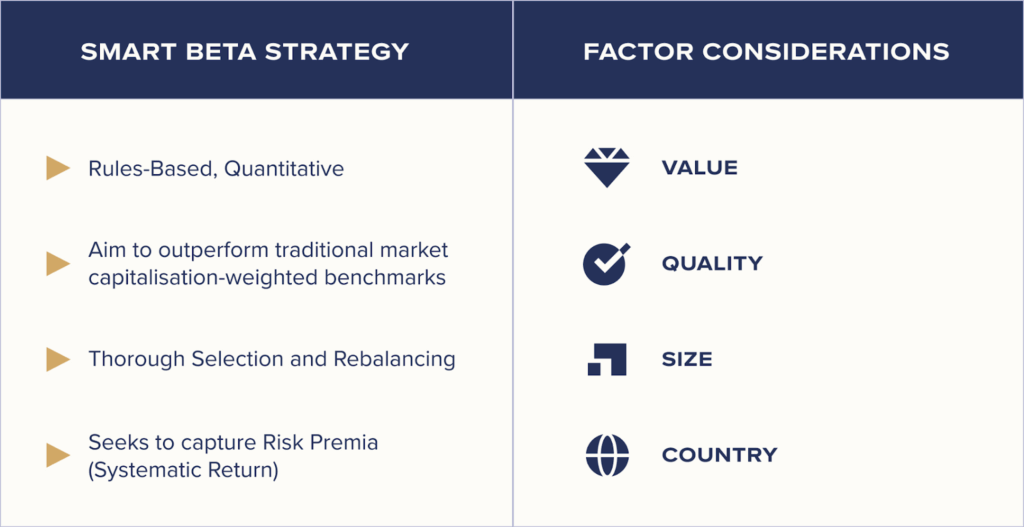

It is a strategy that seeks to deliver better returns by providing exposure to equity markets and to one or more factors at a lower cost. Factors are the characteristics that drive investment returns. This is why smart beta is sometimes also known as factor investing.

From an academic perspective, smart beta aims to enhance systematic returns by extracting risk premia from several factors. Risk premium is the additional return an investor receives for taking on extra risk, compared to that of a risk-free asset, in a given investment. To harvest risk premia, smart beta portfolios are tilted to one or multiple factors that contribute to outperformance.

Understanding factors

Factors are not new. They are grounded in rigorous academic research and backed by Nobel prize-winning work, the most famous being the Fama-French three-factor model. Conceptualised by Nobel laureate Eugene Fama and Kenneth French in 1992, the model states that market returns can be explained by three factors: size, value, and market risk. This was later extended to five factors including quality (or profitability).

Fama and French found that, over time, small-cap stocks earned higher returns than stocks with a large market cap on a systematic basis. The value factor was established based on the stronger performance of stocks with a low price to book ratio (i.e. value stocks) as compared to stocks with a high price to book ratio (i.e. growth stocks). Quality as an investment factor targets companies with strong fundamentals, such as high profitability, stable earnings, and solid balance sheets.

Syfe’s multi-factor approach

One way funds use factors to construct portfolios is to select individual factors they believe will outperform and then tilt their portfolios to those factors. For instance, if fund managers wish to follow the Fama-French five-factor model, they may allocate a judicious percentage of their portfolio to small-cap, value and quality stocks.

Similarly, Syfe’s investment team has taken into consideration the following factors when constructing the Core Equity100 portfolio: size, value, quality and country exposure. These factors have been selected to generate better risk-adjusted returns.

What’s in Core Equity100?

The portfolio is constructed using equity exchange traded funds (ETFs) and index funds that collectively invest in over 5,800 stocks from the world’s top companies. These include Microsoft, Amazon, Facebook, Walmart, Apple, and more.

Additionally, Core Equity100 uses a number of broad-based ETFs to provide international diversification across US, Europe and other markets.

Our ETF selection criteria

To implement our smart beta strategy, we use the most liquid and low cost ETFs to represent our selected factor tilts. Rather than including individual stocks in the portfolio, we use ETFs to provide broad and cost-effective diversification. And by choosing liquid and low-cost ETFs, we lower our customers’ investing costs, minimise bid-ask spreads, and allow customers the flexibility to enter and exit their investments whenever they need to.

To give Core Equity100 a size tilt, we use Xtrackers S&P 500 Equal Weight UCITS ETF (XDEW). XDEW is an equal-weighted ETF that tracks the S&P500, reducing the dominance of mega-cap names.

The size, quality and value are achieved through Dimensional US Targeted Value ETF (DFAT). DFAT provides focused exposure to small and mid cap companies in the US. Its top holdings include Chesapeake Energy, Invesco, and Sofi Technologies.

For value and quality/profitability, our portfolio also incorporates VanEck Morningstar Wide Moat ETF (MOAT) and Dimensional US High Profitability ETF (DUHP).

MOAT targets US companies with sustainable competitive advantages or “wide moats,” while DUHP focuses on large and mid-cap US companies with consistently high returns on capital and the ability to maintain strong profit margins, adding a systematic profitability overlay to our quality exposure. Together, they offer a systematic and diversified approach to investing in quality businesses.

MOAT and DUHP complement each other well, strengthening our portfolio’s exposure to high-quality US equities by blending MOAT’s focus on durable competitive advantages with DUHP’s emphasis on high profitability to create a balanced, resilient quality core. Furthermore, profitability as a factor tends to perform well even when other factors, such as value or size, experience periods of underperformance.

Some of MOAT’s top holdings are Applied Materials Inc and Estee Lauder while DUHP holds companies with the ability to maintain high profit margins, such as NVIDIA and Apple.

For EM exposure, we use iShares Core MSCI EM IMI UCITS ETF (EIMI), iShares MSCI China ETF (MCHI) and KraneShares CSI China Internet ETF (KWEB). They provide exposure to over 2,000 stocks from emerging market countries including China, South Korea, India and Brazil. Top holdings of EIMI include Taiwan Semiconductor Manufacturing Company, Alibaba, Tencent, Samsung, and Reliance Industries.

Learn more about the components of the Core Equity100 portfolio here.

Can investors DIY?

Some investors may wonder if it is possible to implement a smart beta strategy in a Do-It-Yourself (DIY) manner. That’s possible, of course, by using factor ETFs to provide exposure to certain desired factors.

But what distinguishes Core Equity100 from factor ETFs is our blend of factor selection and portfolio optimization. With Core Equity100, you have a 100% equity portfolio that is well diversified across global markets, allowing you to invest in stocks easily from Singapore. You also have a portfolio that is tilted to key factors that have driven and will continue to drive outperformance.

There is no need to analyse and choose from hundreds of factors as well – the Core Equity100 portfolio is optimised to tilt towards factors that will offer the highest potential risk-adjusted returns in the long run.

Smart beta made better with Core Equity100

Apart from the convenience and peace-of-mind that comes with a ready-made and professionally managed smart beta portfolio, there’s also the cost advantage Core Equity100 has.

The portfolio holds multiple ETFs. Replicating these ETFs would cost the DIY investor significantly in terms of brokerage fees and minimum investments. A better option would be to enjoy $0 brokerage fees and no investment minimums with Core Equity100. This way, investors can enjoy the long-term better risk-adjusted returns of smart beta factors while keeping their costs low.

You must be logged in to post a comment.