At Syfe, we believe that smarter investing can lead to better life outcomes. Our mission is to make institutional-level investment offerings accessible to everyone, at just a fraction of the cost charged by traditional institutions.

In this article, we will share more about our thinking and investment approach behind Syfe Core portfolios.

Table of Contents:

- Investment principles of the Core portfolios

- Overview of Syfe’s four Core portfolios

- How we built Core portfolios

- Passive strategies, careful curation of funds

- Getting started

Investment principles of the Core portfolios

At the heart of Syfe’s investment philosophy lie three pillars: diversification, cost-effectiveness, and a long-term vision. We are committed to playing the long game, and that is why our Core portfolios embrace a passive, enduring investment strategy.

Our core portfolios are globally diversified across asset classes, sectors, and geographies. Such diversification reduces risk while enhancing potential returns. We predominantly use index strategies to build these portfolios, ensuring minimal costs, transparent fees, and no hidden trailer-fees (kickbacks). By prioritising cost-efficiency and aligning our strategies with our clients’ goals and risk tolerance, we aim for enduring returns. Built upon years of research, expertise, and experience, our investment approach is designed to stand the test of time.

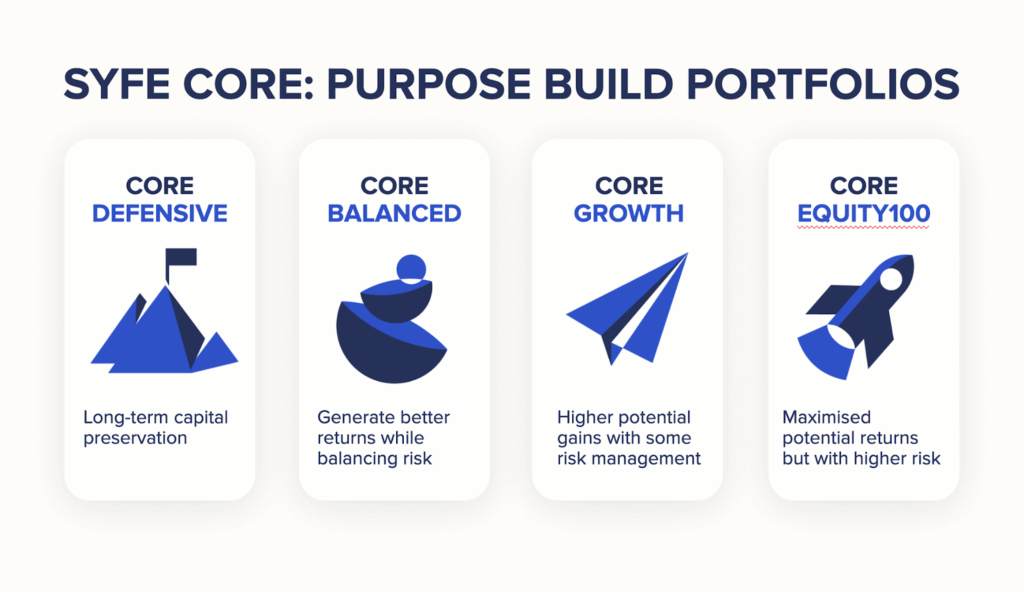

An overview of Syfe’s four Core portfolios

We offer four Core portfolios, designed to address some of the most important customer goals in life, from purchasing their first home to educating their children, and retiring comfortably.

Here’s a quick guide to help you understand which portfolio is right for you.

- Core Defensive is a low-risk portfolio that’s ideal for conservative investors, or those approaching a particular financial goal

- Core Balanced is a medium-risk portfolio that’s ideal for moderate investors with a mid-to long-term horizon

- Core Growth is a high-risk portfolio that’s ideal for growth-oriented investors with a longer time horizon

- Core Equity100 is a 100% equity portfolio that’s ideal for investors who are comfortable taking on higher risk for potential higher long-term returns

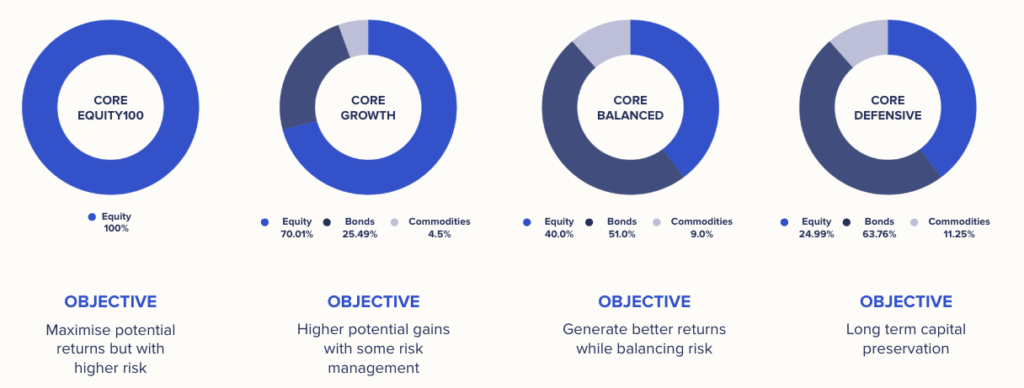

The key difference between each Core portfolio is their exposure to stocks and bonds, which in turn determines their overall risk level.

Growth assets like equities offer higher return potential but come with more risk, while defensive assets like bonds provide stability with lower returns. Essentially, portfolios with more equities pose greater risks and potential rewards. This is why Core Defensive is our lowest risk portfolio and Core Equity100 is the highest, with the latter showing a higher average annual return than the former.

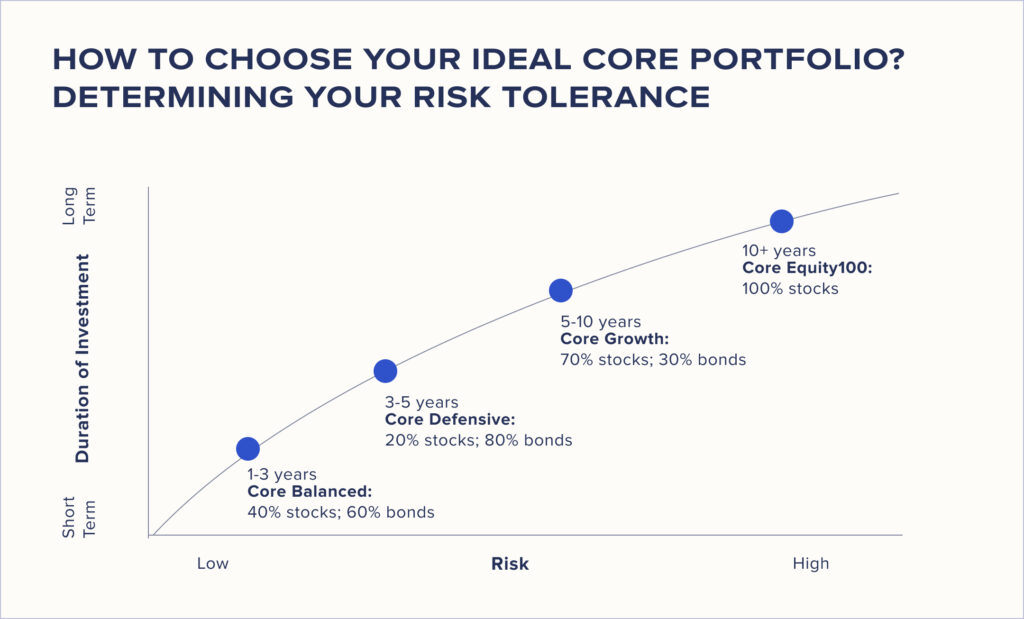

Choosing between the four Core portfolios very much depends on your investment goals, time horizon, and risk appetite.

How we built Syfe Core

Our portfolio methodology for Syfe Core rests on three guiding principles:

- Asset Class Risk Budgeting

- Smart Beta

- Stable asset allocation

Let’s delve into the details below.

Laying a foundation with Asset Class Risk Budgeting

Traditionally, asset allocation is viewed in terms of capital—e.g., a 60/40 portfolio with 60% equities and 40% bonds. However, Syfe Core portfolios use Asset Class Risk Budgeting, where risk, not capital, determines portfolio weights.

Different assets carry varying levels of risk (e.g., equities are more volatile than bonds). With this approach, we allocate portfolio weights to balance overall risk and aim for the highest possible Sharpe Ratio, optimising returns for the risk taken.

Using Smart Beta to add robustness to Core

Another facet of our Core portfolio strategy is our use of factors (or Smart Beta) to further optimise equity allocations.

The equity component of all Core portfolios takes into consideration the following key factors: size, value, quality as well as emerging market exposure. These factors have been selected to generate better risk-adjusted returns over the long term.

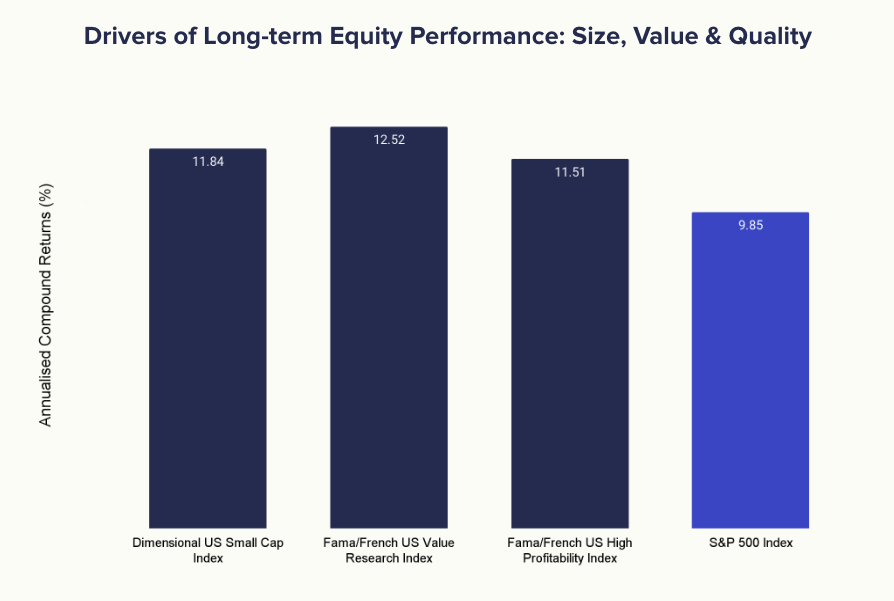

Here’s a closer look at each Smart Beta factor, these come from the academic research which produced the extended Fama-French 5 factor model. These factors demonstrate excess expected returns over time.

- Size: Historically, smaller companies have consistently outperformed larger ones over the long term, despite their higher risk. This outperformance is often due to their greater growth potential and ability to adapt quickly to market changes.

- Value: Value investing focuses on companies that are undervalued relative to their fundamentals, offering strong potential for long-term appreciation. Historically, value stocks have tended to outperform growth stocks, particularly during periods of economic recovery or market dislocations.

- Quality: Quality (or profitability) as an investment factor targets companies with strong fundamentals, such as high profitability, stable earnings, and solid balance sheets. Over the long term, high-quality companies have demonstrated the ability to deliver superior returns while also providing resilience during periods of market volatility.

How do we use them:

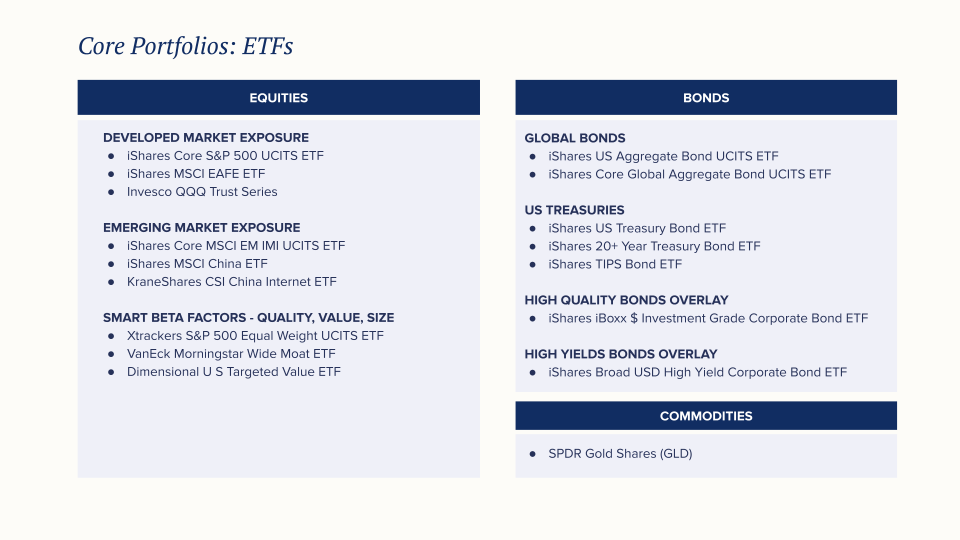

To capture the benefits of these historically proven factors, we use Dimensional U.S. Targeted Value ETF (DFAT) for comprehensive exposure to Size, Value, and Quality factors, VanEck Morningstar Wide Moat ETF (MOAT) further strengthens the focus on Quality and Value. We also use Xtrackers S&P 500® Equal Weight UCITS ETF (XDEW) to increase your portfolio’s exposure to size while benefiting from its tax-efficient UCITS structure.

These carefully selected ETFs collectively ensure your portfolio is optimally positioned with balanced exposure to Size, Value, and Quality for long-term success.

Stable asset allocation

With Core portfolios, investors will find that their asset allocation is relatively stable. This is because the portfolios utilise risk parameters that are calibrated for a longer term risk horizon to reduce short term portfolio reflexivity, i.e. short term asset allocation changes.

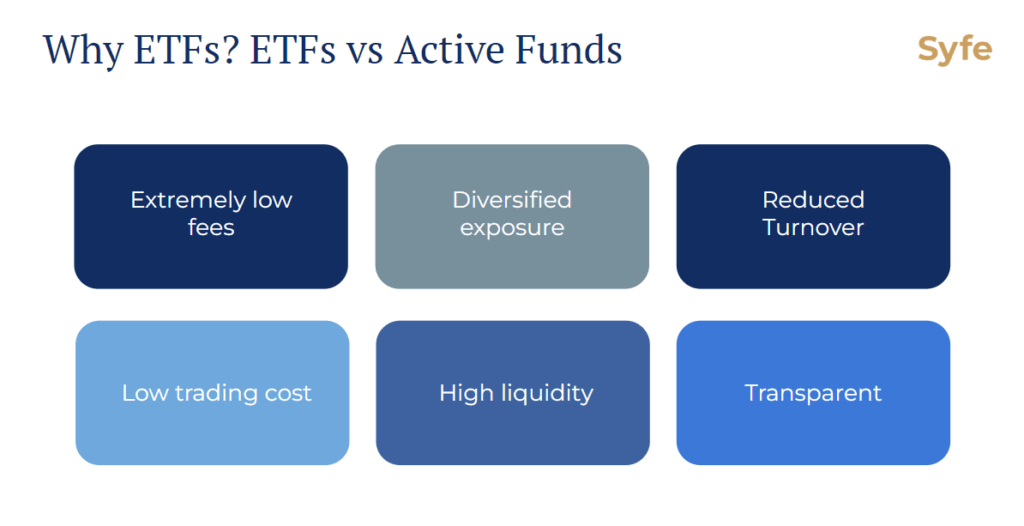

Passive strategies, careful curation of ETFs and index funds

ETFs and index funds are the building blocks of Core portfolios. Compared to actively managed funds, they provide a highly efficient, low cost and passive way to invest into the global markets.

While ETFs have been the poster child of passive investing, traditional active fund managers have picked up on the trend by introducing index funds to capture a piece of this movement. Investors need to carefully evaluate index funds before investing as some can come embedded with much higher fees than their ETF counterparts.

Our process for selecting funds is rigorous. We do not endorse specific fundhouses or managers. Instead, our investment team selects funds based on their liquidity, low expense ratios, and minimal tracking errors relative to their benchmarks.

Getting started

Syfe Core portfolios have no minimum investment amounts and no lock-ins. You can set up as many Core portfolios as you prefer based on your goals. For example, you may invest in Core Growth for a long-term goal like retirement and choose Core Defensive for a shorter term goal such as a house downpayment. Ready to invest in Core portfolios?

You must be logged in to post a comment.