Syfe was built out of a desire to bringing greater transparency to the fees associated with investing, and remove the layers of hidden commissions charged by financial institutions. Comparing investment platforms by looking only at platform fees tells only half the story of what you truly pay when investing in funds or unit trusts.

In this article, we get under the skin of fees and if you don’t have the time for the full article, here are the four main takeaways:

- While fee layers depends on each platform, investors mainly pay for two key ones – platform fees (charged by investment platforms and a.k.a annual fees) as well as fund fees (charged by fund manager and a.k.a management fees)

- The financial industry has been plagued by the issue of trailer fees which result in higher costs to investors – this is an often unseen fee that is hidden/ embedded into the funds’ management fees, beyond the platform fees

- Even with platforms which offer trailer fee rebates, mutual funds have higher fees than passive investments ETFs, resulting in greater costs to investors

- Ultimately, beyond costs, investors should focus on how digital investment platforms support investors through the tools, strategies and features which support their long-term wealth building journey

To help visualise this, we will take a local favourite kueh, the kueh salat, to understand fee layers. The bottom layer – sticky rice represents the platform fees charged by different investment platforms for the “service” they offer to users. This is usually the fee stated on the platform website. For Syfe, our portfolio fees range from 0.35 – 0.65%, depending on your tier.

Comparing digital investment platforms by only looking at platform fees is similar to eating half of the kueh, and missing the full picture. While doing so would show that some self-serve fund platforms indeed do charge the lower access fees vs higher management fees charged by robo-advisors, it misses the point of the fund fees (green layer of the kueh salat), charged by asset managers on top of platform fees. You don’t see these costs at the moment of investing but they could add up extra costs that eat into your returns.

The True Costs of Investing

Firstly, the average management fees charged by mutual funds average between 1.5% to 2%. This is much higher than investing into passive investment vehicles such as ETFs where the average management fees can be as low as 0.05% – a key reason why Syfe uses ETFs to construct its portfolios. Mutual funds have pivoted to launch index funds at lower costs, but they still cost much more than equivalent ETFs. While some mutual funds may make sense, especially for exposures such as fixed income where they could be more tax efficient and manage FX risks better, the majority of AUM is locked into strategies that can be easily replicated in the form of ETFs and at a fraction of the costs.

Secondly, the mutual fund industry has been plagued for decades from the “trailer fees” that distributors including self-serve platforms pocket from the fund managers they onboard onto their platform. So while these “access only” platforms claim to charge no sales fees, annual management fees, access fees, switching fees or platform fees, they make money from the trailer fees that they receive from the fund managers of the funds that they distribute on their platforms. On average, the trailer fees can be as much as 50% of the underlying fund management fees or 0.75% to 1% in actual percentage terms – which is never passed on to investors and pocketed by these distribution platforms.

In some markets, regulators have clamped down on trailer fees by requiring mutual funds to only offer clean share classes.

For Syfe, our Cash+ portfolio is the only place where we use mutual funds as the underlying assets, and there, we return 100% of the trailer fees to users.

Lastly, research has shown that almost 90% of mutual funds underperform their respective benchmarks. This underperformance can be as high as a few percentage points. Put together, the net return generated by clients investing into mutual funds can be lower by as much as3% to 5% compared to investing via passive vehicles such as ETFs. When investing, it is important to understand the underlying assets that you invest in, and why you are doing so. Ultimately, we believe that investors are best placed to decide what works best for them, but with the information needed to support and guide their decisions.

Going beyond costs – what value do I get from my investment platform of choice?

Beyond just the costs of investing, it is equally important to understand the full value that robo-advisors provide to investors on a journey of managing wealth for the long-term. When investors invest in the Syfe platform, they are able to put their money into pre-curated portfolios managed by an expert investment team and designed to solve their most important core investment goals.

These portfolios use passive investment vehicles such as ETFs as building blocks which are highly cost effective and efficient. They are periodically optimised/rebalanced to maintain a strategic asset allocation that maximises the risk-adjusted returns for the end client. On top of this, clients do not incur any brokerage fees for the re-optimisation of their Syfe Wealth portfolios and get access to powerful features such as auto dividend reinvestment, ability to automate their investments via recurring contributions and more importantly speaking directly with human advisors to guide them through their investment journey.

Comparing apples to apples

To create a fairer comparison, we have constructed two tables:

- Comparing investments into ETFs via Syfe Trade, our brokerage platform with investments into funds via self-serve platforms (see Table 1); and

- Comparing our managed portfolios solution Syfe Wealth, with other robos and self-serve platforms (see Table 2);

to show how investors can use different tools within Syfe to get the best value when growing wealth for the long-term.

Table 1: Syfe Trade vs Self-Serve Fund Platforms

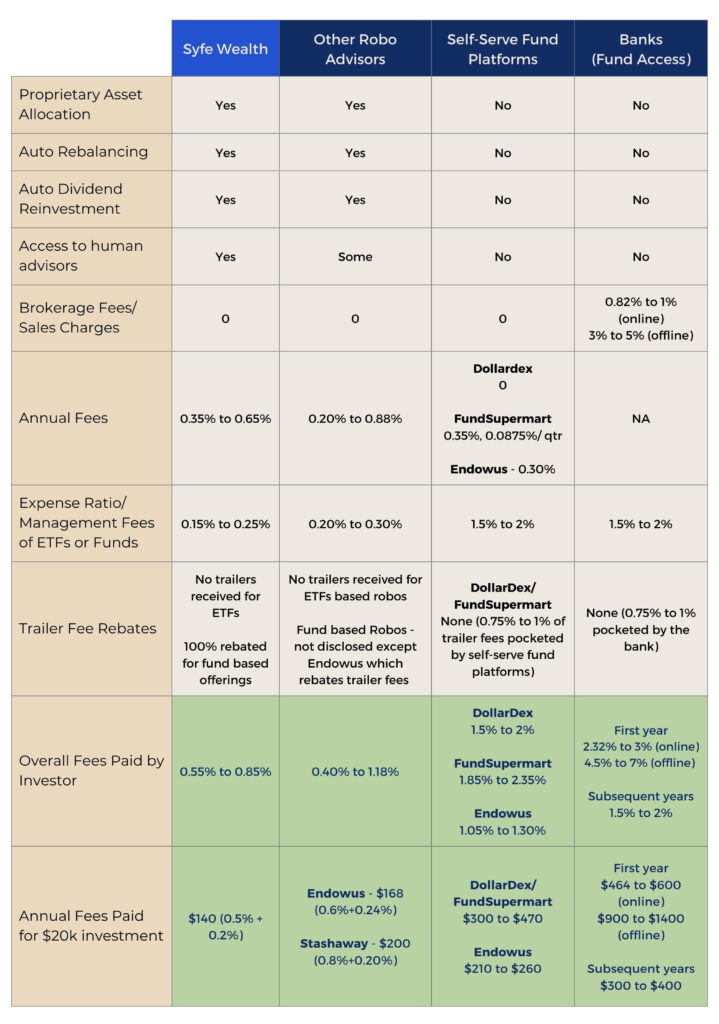

Table 2: Comparing Syfe Wealth, Other Robos vs Self-Serve Fund platforms

Ultimately at Syfe, we are creating an offering where users can grow their money to its fullest potential.

With both managed portfolios and brokerage, investors get to build wealth on their own terms, all in one place and tap into institutional strategies built by our investment team to get the best outcomes for their wealth. Low fees are a key priority for us and we are confident of being the one of the lowest cost offerings in the market.

Together with the suite of tools and platform features – expert curated portfolios, automatic reinvesting, recurring buy, free trades, fractional investing and more, we endeavour to support users on every step of their wealth journey. Just like every piece of kueh that you taste, it’s important to assess it in full, and focus on the value and quality you get.

You must be logged in to post a comment.