US Fed raise interest rates (again)

The Federal Reserve (the Fed) hiked interest rates by 50 basis points on 14 December, bringing its key rate to the 4.25%-4.5% range. Investors were indeed expecting a smaller hike after recent CPI data showed signs that past hikes have been working.

Does this mean that the investment market will have a Christmas rally?

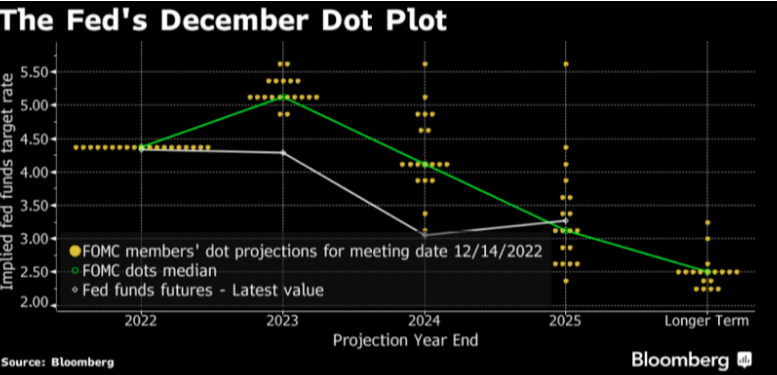

The Fed’s dot plot showed that the peak interest rate for 2023 has risen to 5.1% from 4.6% in September and that interest rate is projected to stay above 4% in 2024. This is more hawkish and the market will be pricing in this new information. It also doesn’t help when Powell sounded hawkish, saying “we are not done.” Having said that, fortunately the Fed has entered a new phase where they start to think about how much to raise, rather than raising rates at all cost to tame inflation. Taking all this information together, we are more optimistic than pessimistic. Yes, rate hikes would go on but this is not new. Additionally, given that the interest rate is currently at 4.25%-4.5%, there isn’t much room to reach 5.1%. Put more simply, investors seem to be betting that inflation will fall quickly enough and decisively enough to allow the Fed to soften its stance.

Why should you care?

This year has shown us that rising interest rates are harmful not just for the economy, but for asset prices. At this point, we are inching closer to the peak for interest rates and this means 2 things. On one hand, we are unlikely to see even more aggressive rate hikes and that could be good news for asset prices. On the other hand, rates are still significant and that could slow down the economy and possibly push it into a recession. This would affect companies’ earnings and by extension, harm the share price of riskier assets like stocks. Which side are you on?

US inflation beats analyst’s expectation

Inflation is still extremely far from the 2% target set by the Fed but we have witnessed a small Christmas miracle. The Bureau of Labor Statistics reported on Tuesday that the consumer price index rose 7.1% from a year ago in November, falling below economists’ expectations of an 7.3% increase. Additionally, prices for energy and used cars – major culprits in this year’s inflation boom – fell by 1.6% and 2.9% last month from the one before. The feds have been committed to reducing inflation and this data shows that their efforts have been effective.

Does this mean the worst is over for investors?

The resounding reality is that even though inflation rates are rising at a slower rate, at 7.1%, it is still extremely painful for consumers. Investors are hoping that falling inflation is a trend that will continue and this would ultimately influence the Feds to deviate from their aggressive interest rate hiking path. Coupled with a strong labour market growth and low unemployment in the US, the US may even experience a soft landing – the perfect case where inflation eases back towards its target without huge recessionary economic impacts. Suffice to say, the upcoming earnings season will definitely be an interesting one to track.

Will we be on Santa’s naughty list for overconsumption of coal? Let’s take a sneak peak into the 2022 commodities market.

By the end of 2022, we will have used a record-breaking 8 billion plus tons of coal, breaking the record set back in 2013. That is worrying news for global emissions: if you did not know, coal produces twice as much C02 as natural gas, whose environmental record is already subpar. This unprecedented rise in demand and prices of coal is in part due to the Russia-Ukraine crisis that disrupted energy supplies all over the world.

What is causing this unprecedented increase in demand?

Demand for coal has risen so much that half of all coal companies including Alliance Resource Partners (ARLP) and Consol Energy (CEIX) are expanding right now, posing a major setback for climate goals. Alternatives such as natural gas are also becoming less price competitive, with U.S natural gas prices trading >200% above where it traded at the end of 2019, just before the Covid 19 pandemic kicked in. China and India have also experienced coal shortages, assisting in sending coal prices around the world to new highs. Therefore, coal companies may be posting good income statements during the upcoming earnings season. So far, coal stocks have experienced decent growth in 2022, with most stocks largely consolidating.

Coal stock investors may be sitting on hefty profits and would want to confirm the most optimal exit strategy for their positions. The question is whether coal stocks are gearing up for another run higher or they are poised for a serious pullback. Are you bearish or bullish on the coal industry in the long term?

| Index | Level | 1 Week | 1 Month | From Jan 1 2022 |

| S&P 500 (US Stocks) | 3,852 | -2.2% | -2.5% | -19.7% |

| Nasdaq 100 (US Tech Stocks) | 11,243 | -2.8% | -2.7% | -31.9% |

| CSI-300 (Chinese Stocks) | 3,893 | -1.5% | 2.3% | -20.8% |

| Bitcoin (in USD) | 16,759 | -5.9% | 0.5% | -64.9% |

Source: Google Finance, as of December 17th, 2022.

You must be logged in to post a comment.