Joint accounts aren’t just for couples. Here’s how to think about investing together, whoever your ‘together’ is with.

When most people hear “joint account”, they picture a couple freshly married, combining their salaries, splitting the utility bills, and planning for their shared future. That’s a fair picture. But it’s not the complete one.

The reality is that your financial life rarely revolves around just one relationship. You may be investing with your spouse, supporting your parents in retirement, or even coordinating your finances with a sibling. Each of these relationships comes with its own goals, timelines, commitments and expectations—and how you invest together should reflect that.

That’s why people are increasingly realising that joint accounts are not just a convenient tool, but a way to build wealth and legacy together.

Jack Prickett, Chief Commercial Officer at Syfe, shares more on MoneyFM about how you can use joint accounts to growth wealth with your loved ones—as well as secure your children’s future.

One account doesn’t fit all relationships

Different relationships call for different strategies.

Think about the different financial dynamics in your life and what each one calls for. You’re not just a partner—you might also be a child, sibling, or caregiver.

Therefore, a joint account strategy shouldn’t be one-size-fits-all. In fact, one of the biggest mistakes people make is treating a joint account like a single financial setup that can serve every purpose.

With your spouse or partner: long-term wealth building

While this is the most familiar use case for joint accounts, it’s also an evolving need.

Couples are no longer just using it to pay bills. They’re also saving up for a home, their retirement, or their child’s education, and using joint accounts to invest and build shared wealth.

A globally diversified portfolio like Syfe’s Core portfolios can help couples balance risk and long-term growth. By investing across global equities and bonds, the portfolios— with equity-bond variations across Defensive to Equity100—are diversified and catered to your risk appetite so you can choose an allocation you both are comfortable with.

With your parents: steady growth and income generation

A joint account with an aging parent usually means different priorities:

- Capital preservation with some growth

- Generating consistent income

- Supplementing retirement needs.

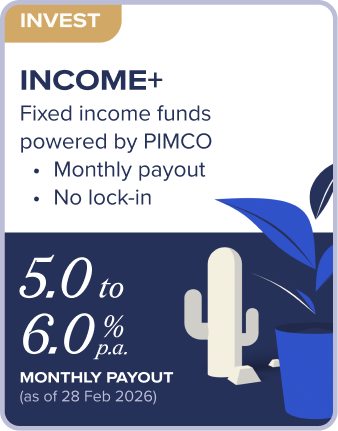

Syfe’s Income+ portfolios are built for this. They are focused on generating regular income from a diversified mix of bonds and dividend-paying assets.

For families, this setup also improves transparency. Instead of one person managing everything behind the scenes (as seen in nearly 30% of households, according to our recent survey), a joint account allows for shared visibility and decision-making, allowing all members to collaborate financially.

With a sibling: flexibility and liquidity

Not all joint accounts are about long-term investing. Some are designed for coordination and convenience.

A joint account with a sibling might be used to:

- Pool funds for a parent’s medical or living expenses

- Build a shared emergency fund

- Save for short-term goals

In these cases, liquidity is essential. You need immediate access to funds when situations change, not months or years down the line as with long-term portfolios.

Solutions like Syfe’s Cash+ Flexi offer higher yields than traditional savings accounts while keeping funds accessible and liquid. This makes them ideal for shared responsibilities that require flexibility.

Here, the goal is mainly to keep readily deployable funds at hand rather than maximising returns.

The rise of purpose-driven joint accounts

Another key insight from Syfe’s survey is a shift toward purpose-driven investing.

More than 1 in 3 respondents plan to use joint accounts for their children or for wealth transfer to the next generation. This signals a growing focus on generational wealth, not just individual financial success.

Joint accounts are no longer just about the present. They’re becoming tools for children’s savings, education planning, and even estate and wealth transfer strategies.

This evolution reflects a broader mindset shift, from managing money together to building wealth across generations.

The case for ring-fencing

With multiple financial relationships comes the need for structure.

One of the most effective ways to manage this complexity is by keeping different financial goals separate instead of merging everything into one account.

In this method of ring-fencing, you create:

- One account per relationship

- One purpose per account

- One investment strategy aligned to that purpose

This means that your long-term investments with your spouse remain separate from the account you manage with your parents. Your sibling fund for shared expenses doesn’t get mixed up with anything else. Each account has a clear objective—and that clarity leads to better decision-making.

With Syfe Joint Accounts, you can open up to five joint accounts, each with a different co-holder. Each account can be assigned a different Syfe portfolio depending on its goal—growth, income, or liquidity—and both account holders will have equal visibility and control.

A different question to ask yourself

Instead of asking whether you should open a joint account, the better question is: “Which of my relationships could benefit from us investing together, and what would the right portfolio be for each of them?’

Here’s how you can approach each financial relationship:

- A long-term joint investment account with your partner

- A stable, income-focused account with your parents

- A flexible, accessible account with your siblings

- A consistent growth account for your children’s future

Joint accounts are no longer just about splitting expenses, but solving coordination challenges, improving transparency, and building wealth together.

With Syfe’s Joint Accounts, you can move beyond fragmented financial management and create a system that reflects your financial relationships, goals and strategies.

Ready to invest together? Set up a joint account today.

You must be logged in to post a comment.