Caring for aging parents while managing your own finances? Here’s why opening a joint investment account can improve transparency, reduce stress, and make your parents’ savings work harder.

(Joint Accounts on Syfe is currently open to the first waitlist participants and will be available to all users soon. Watch this space.)

If you’re in your 30s or 40s, there’s a good chance you’re already part of the sandwich generation, balancing your own financial goals and commitments while supporting your aging parents.

You could be giving them a monthly allowance, or you could be helping them manage their savings or decide where their money should be invested. You might even have quietly moved their funds into a higher-yield account to optimise returns for them. Yet, there is little transparency and collaboration between you and your parents.

According to our recent survey, the “coordination gap” is a prevalent issue: more than 45% of people still invest separately and struggle to coordinate their finances manually, even when they have shared goals.

This highlights a growing need for better financial planning for parents, especially as life expectancy increases and retirement lasts longer.

But with joint accounts, instead of just managing parents’ finances for them, you can now manage it with them for better results and experience.

The Hidden Risks of Managing Money For Your Parents

Managing your parents’ money on their behalf often stems from good intentions. You want to simplify things, protect them from unnecessary stress. And sometimes, it feels more efficient to just handle everything yourself.

But this approach can create unintended challenges:

- Lack of transparency: Your parents may not fully understand where their money is or how it’s performing

- Loss of financial independence: They may feel disconnected from decisions that directly affect their lives

- More pressure on you: You carry the full responsibility for outcomes, including the performance of the investments

- Potential future conflicts: Misaligned expectations around risk, withdrawals, or returns can lead to disagreements

According to our survey, in nearly 30% of households, a single person manages all investments. This often leads to lower transparency, little shared control, and gaps in financial understanding.

This is where many families struggle with managing elderly parents’ finances—making the right financial decisions and making them in a way where everyone is aligned.

What a Joint Investment Account Can Change

A joint investment account with parents is more than just a logistical tool. It can change how financial decisions are made, where instead of one person managing everything behind the scenes, both parties:

- Participate in key financial decisions

- Have visibility into the account

- Can access performance updates

This addresses the coordination gap many families face. Rather than juggling separate accounts or relying on one person to manage everything, a joint setup creates clarity and structure for everyone to be equally involved.

More than 50% of users surveyed cite long-term wealth building as their primary goal for a joint account, not just splitting bills. A joint investment account allows everyone to look at the numbers on the same app and make decisions together.

Practical Financial Planning With Your Family Members

Cultural norms and generational differences often make conversations about money with your parents uncomfortable.

A joint account for families allows you to set something up together and opens up conversations about retirement and long-term security. This makes financial discussions more practical and targeted.

Our survey results show that over 1 in 3 people now intend to use joint accounts for children’s savings or wealth transfer, demonstrating that shared investing is increasingly about long-term planning, not just short-term convenience.

Choosing the Right Investment Strategy for Your Parents

One common mistake people make when opening a joint investment account with their parents is going for the same aggressive, growth-oriented portfolio they would choose for themselves.

While you might want to aim for higher returns, your parents’ financial needs are different. In their 60s or 70s, they have a shorter time horizon and a different relationship and response to market volatility than you do. This account is not primarily growth-driven, but income-oriented. It is meant to generate reliable, steady income while preserving capital and minimising volatility.

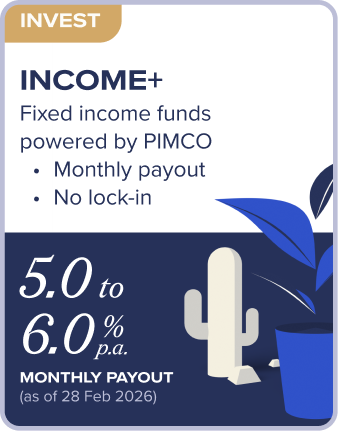

Syfe Income+: For steady payouts

Income+ portfolios focus on generating regular payouts from a diversified mix of bonds, REITs, and income-generating assets. For retirees or those approaching retirement, this is a way to keep their savings working without exposing them to excessive risk. It’s a practical solution for retirement income planning in Singapore.

Syfe Core Balanced: For growth with lower volatility

If your parents are still in accumulation mode—perhaps in their late 50s with some ways to go before retirement—a more balanced approach might be more suitable for them. Syfe’s Core Balanced portfolio is globally diversified across equities and fixed income, offering growth potential with lower volatility than an all-equity portfolio.

Before you open a joint account with your parents, have these conversations with them:

- What is this money for—retirement income, healthcare buffer, or something else?

- How much will each party contribute, and how often?

- Who makes the call on withdrawals, and when?

- What happens if one of you needs the money urgently?

These are essential questions to work through together before setting up a joint account. Skipping them can turn a joint account into a source of tension instead of a tool for connection.

Help your parents’ savings work harder, together. Open a Syfe Joint Account and choose the portfolio that fits this chapter of their life—whether it’s steady income, balanced growth, or long-term security.

Joints Accounts are coming soon to Syfe and will be progressively rolled out to all users.

You must be logged in to post a comment.