Singapore REITs (S-REITs), like their global counterparts, are required to distribute 90% of income earned (mostly from rental income and capital gains when a property is sold for example) as dividends to unitholders and investors. This explains why even though the pandemic hit the sector hard, dividend yields were still averaging 4% to 5%.

Table of contents:

- REITs prove resilient income generators

- Re-opening as a tailwind for S-REITs

- REITs as a growth inflation hedge

- REITs in rising rates

- REITs vs other assets

- Diversified S-REIT Exposure

S-REITs are resilient income generators

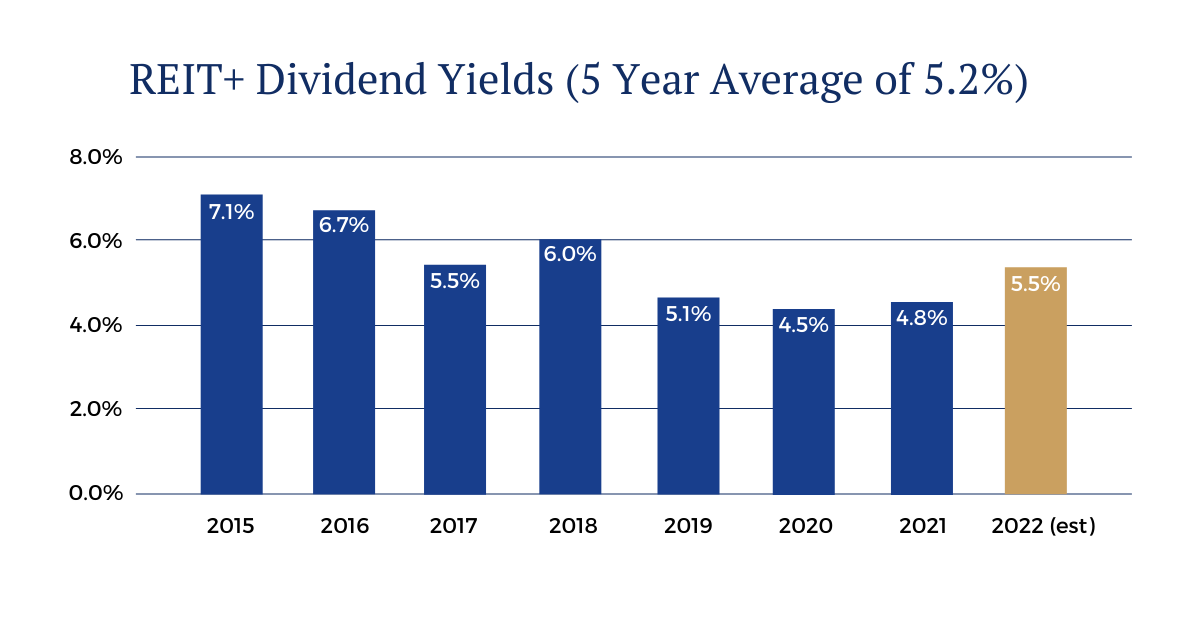

From 2015 to 2021, the average dividend yield for Syfe REIT+ was 5.7%, while the 5-year average was 5.2%. As we exit the movement restrictions due to Covid-19, we see S-REITs in a better position this year.

In the table below, we show income generated on a monthly basis when investing in Syfe REIT+. As compared to investing in physical real estate in Singapore, which typically cost more than a million dollars (and not including additional costs such as stamp duties, taxes and cost of maintenance), when an investor invests the same amount in REIT+, estimated income generated monthly is about $4,500.

Re-opening as a tailwind for S-REITs

Despite the disruptions caused by the pandemic, real estate value in Singapore and beyond have continued to grow.

Even before the latest easing of Covid-19 rules, we have seen some promising indicators: passenger volumes at Changi Airport, flight bookings on websites like Skyscanner, and increases in revenue in retail and hospitality related S-REITs, albeit from a lower base in 2020 and 2021.

Now, with the maximum group size for social gatherings at 10, optional mask wearing outdoors and up to 75% of employees expected to return to the office, along with easing of cross-border travel, S-REITs (and Syfe REIT+) are poised to benefit from the latest easing of rules.

Optimism for Office and Retail REITs

Office REITs and Retail REITs historically have the highest average dividend yields. This has mostly held up even during the pandemic. Moving forward, we see more cause for optimism. For example, Suntec REIT has highlighted the recovery of its retail business at Suntec City Mall, where December 2021 tenant sales exceeded pre-pandemic levels in December 2019.

Here is a deep dive into these two REIT subsectors:

REITs as a growth inflation hedge

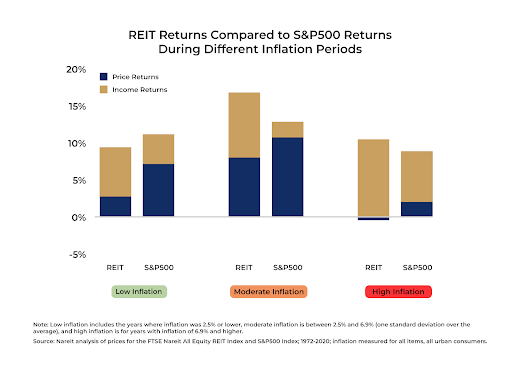

Real assets do well during inflationary periods. In Singapore, we have not had a sustained period where inflation (measured by Consumer Price Index, CPI) was above 2% since the inception of the iEdge S-REIT Leaders Index (made up of the 20 largest and most liquid S-REITs) in 2014.

To use an example from the US, when we compare US REITs vs S&P 500 during different inflationary periods, we see REITs outperforming when inflation is moderately high (more than 2.5% annually). We would expect to see this trend play out in Singapore too; income from real assets like REITs are generally tied to inflation – as leases and streams of revenues increase, that passes through to income. As economic activity increases, rents rise, utilisation improves and those benefits are passed on to the investor.

S-REITs in Rising Rates

REITs, along with other capital intensive sectors, are sensitive to interest rates, given the impact on borrowing costs and yield spreads. S-REITs have been managing their interest rate exposures actively. According to SGX, on average, close to 75% of S-REITs’ current debts are either in fixed rates or hedged through floating-to-fixed interest rate swaps.

In addition, S-REITs currently have an average gearing ratio of 37%, comfortably below the regulatory threshold of 50%. Gearing ratio, which measures leverage, is calculated by dividing total borrowings by total assets. A lower gearing ratio below the threshold implies healthy balance sheets and that S-REITs can service their debt and still have room to raise more debt (if and when needed) for additional acquisitions or operations.

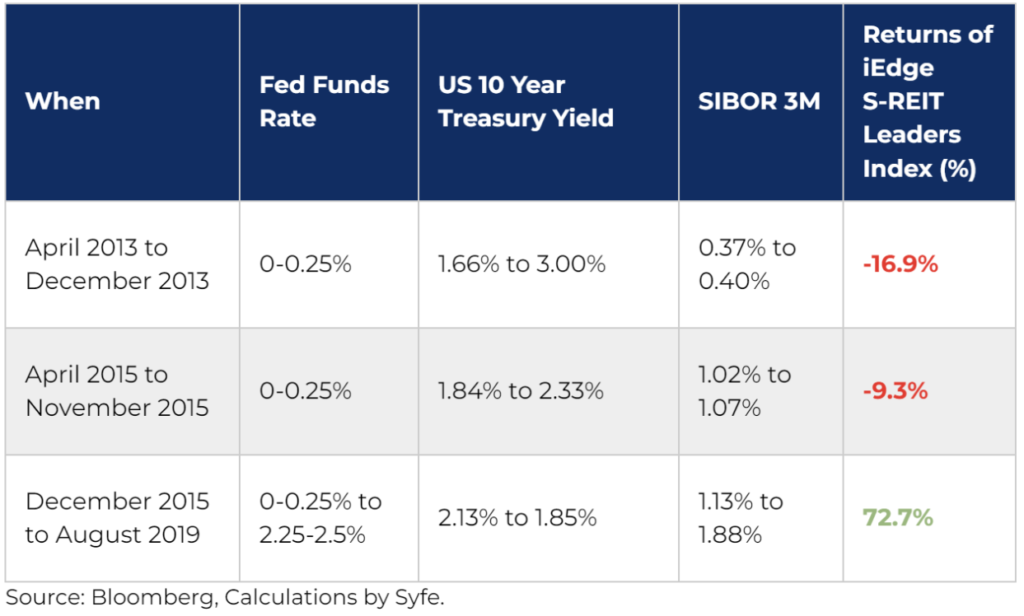

Looking at periods in the past where the Fed funds rate has increased along with the 3m SIBOR rate, the performance of S-REITs have been mixed.

During the taper tantrum of 2013, S-REITs fell by close to 17% over 9 months. In 2015, where global markets experienced a sell-off with the Greek debt default, a sharp fall in petroleum prices, and slowing growth in China, S-REITs fell 9% over 8 months.

However, from the time we saw the first rate hike in late 2015 to when the Fed funds rate hit 2.25% -2.5% (the highest in ten years), S-REITs delivered stellar performance of almost 73%.

So far this year, S-REITs have taken the first rate hike in March 2022 in stride, gaining 4.5% over the month ending March 31, 2022.

Over a 5 year period, which captures part of the previous rate hiking cycle, S-REITs demonstrated their resilience and ability to grow despite higher interest rates and borrowing costs.

What was different in 2013, 2015, 2016-2019, and now?

Ultimately, growth matters here. Economic and earnings growth drive equity returns. Similarly, economic and rental income growth drive returns of S-REITs. Now that we are a quarter of the way through 2022, and two years after the pandemic started, things are looking better for the S-REITs.

The effects of higher inflation is difficult to ignore and as Senior Minister Tharman Shanmugaratnam pointed out this month, “the risk of stagflation is real”. We currently have one of three conditions for stagflation: above average inflation (4.0% for CPI-All Items in January 2022), but the labor market remains resilient (unemployment rate of 3.1% and 211 job openings for every 100 unemployed persons), and domestic and global economic growth is still expected to be positive. Inflation is expected to cause a shift in consumer spending and consumer and investor sentiment, but it is highly uncertain currently whether the economy would tip into negative growth territory.

In the words of Chair Powell, “the probability of a recession within the next year is not particularly elevated” as demand is strong, “household and business balance sheets are strong” signaling an economy that is still able to “flourish in the face of less accommodative policy”.

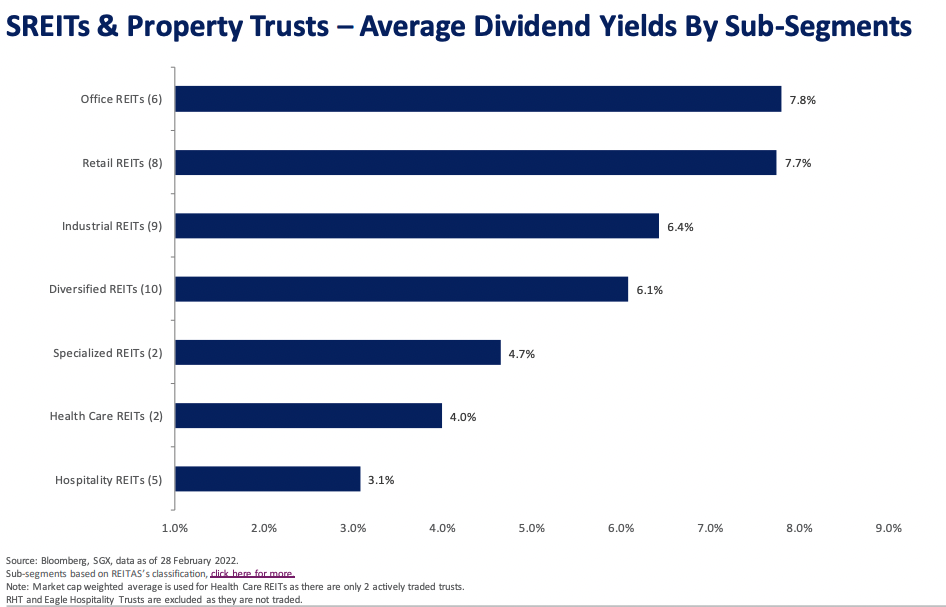

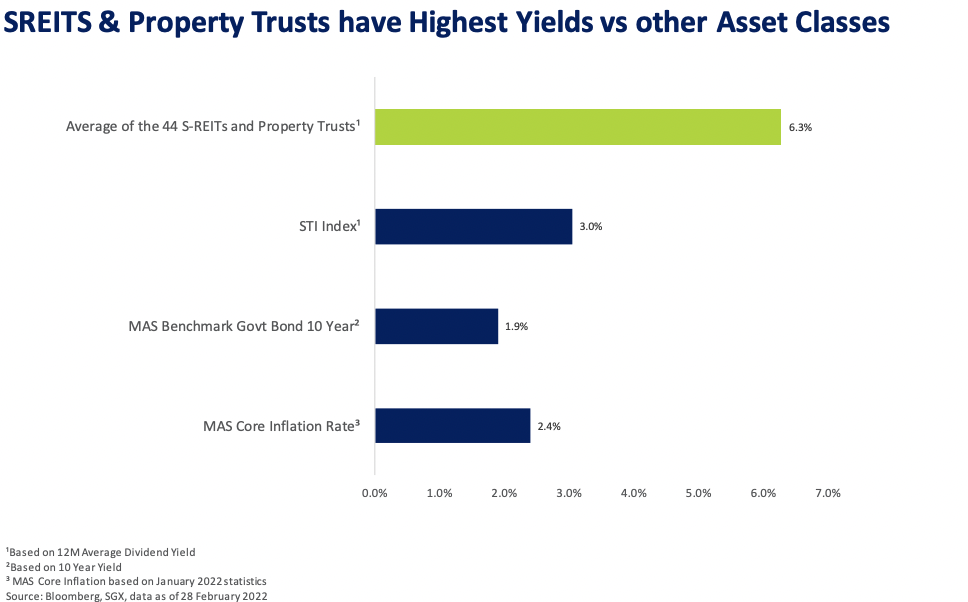

S-REITs Offer High Yields vs Other Asset Classes

Average yields for 44 S-REITs and Property Trusts was 6.3% (as of Feb 28, 2022). For Syfe REIT+, which tracks the iEdge S-REIT Leaders Index made up of the 20 largest and most liquid S-REITs, the average dividend yield is 5.5%.

High dividend yield (5-year average of 5%) makes S-REITs attractive to retail and institutional investors seeking an income solution, as compared to government bond yields (1.9%, with duration risk but almost no credit risk) and fixed deposit rates (1%, low risk but with lock-ins and limits). Even compared to the Straits Times Index (STI), which is closer in risk profile to S-REITs, the 12-month average dividend yield of S-REITs is twice that of STI (6.3% vs 3.0%).

Diversification Matters

As the old saying goes, don’t put all your eggs in one basket. A diversified REIT portfolio with exposure to Industrial, Retail, Office, Hospitality, Healthcare and Diversified REITs will be more resilient. Syfe REIT+ holds 20 of the largest Singapore REITs such as CapitaLand Integrated Commercial Trust, Mapletree Commercial Trust, Ascendas REIT and more.

By investing in Syfe REIT+, you automatically own all of these REITs. Plus, the portfolio is designed to let you invest in Singapore REITs with a flexible monthly investment plan.

Simply create a Syfe account, decide your preferred investment amount, and set up a recurring transfer through your bank. There’s no lock-in period so you can withdraw your investments anytime.

You must be logged in to post a comment.