The original version of this article first appeared in The Business Times.

In early May, tech giants lost more than $1 trillion in value with Apple’s market capitalisation reduced by over $200 billion. Cryptocurrencies have also experienced a major meltdown with Bitcoin free-falling below $30,000 and other top tokens falling to new lows. The crypto world is still reeling from the rapid collapse of the TerraUSD stablecoin (UST) which has majorly shaken the confidence of even staunch crypto loyalists.

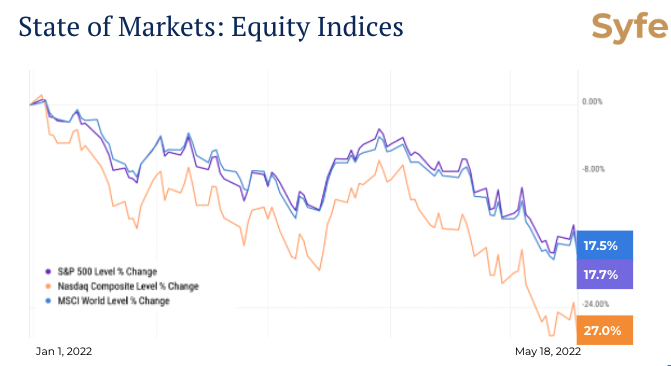

The stock market has been off to a difficult start this year. Major equity indices have been swinging between gains and losses as investors come to grips with rising inflation, higher interest rates, geopolitical turmoil, supply chain issues, and COVID-19 lockdowns in China. The S&P 500 is now squarely in correction territory and Nasdaq-100 being in a bear market with an almost 30% fall from peak.

Amidst the turmoil in current markets, we are also entering a period where inflation in the US is at a 40-year high, and inflation in Singapore accelerating to 5.4%, the highest levels in the last decade. Given this series of developments across global markets and at home, what should investors do to navigate these unpredictable times?

Take the long view

The market boom experienced during the last two years has made many investors huge paper gains. Everyone and anyone can be an expert when the markets are experiencing a bull run, but what happens when the music stops?

I would encourage those who are serious about investing to use this time to pause, take stock and go back to the fundamental basics of investing. Growing one’s wealth is not a short-term endeavor and patience is key. As the “Oracle of Omaha” Warren Buffet said, “If you aren’t thinking about owning a stock for 10 years, don’t even think about owning it for 10 minutes.” While I know this period hasn’t been easy, history tells us that long-term investors will prevail.

Grab the only free lunch left in the world – diversification

Essentially, diversification is not putting all your eggs in one basket. The concept is simple. If your portfolio contained just one stock, your portfolio value is entirely dependent on the performance of that one stock. But if you invest in many different stocks, you’re reducing the risk of any one of them delivering disappointing returns.

A diversified portfolio should be made up of assets that have no or low correlation. For instance, stocks and bonds are known to have a low correlation. When stock prices go up, bond values tend to go down. Ultimately, a well-diversified portfolio is one that has a meaningful allocation to multiple asset classes, sectors and geographies.

94% of an investors’ returns come from the right asset allocation

Long term studies have proven that asset allocation is by far the most important driver of long term returns and performance. In fact, only 6.4% of the variation in a portfolio’s returns was determined by market timing and individual stock selection. The other 93.6% is derived from the mix and proportion of various asset classes constituting the portfolio, also known as asset allocation.

Traditionally, asset allocation is thought of in terms of capital. If you have $100000 and you allocate $60000 to equities and $40000 to bonds, you’ll have a classic 60/40 portfolio. Through periodic rebalancing, you’ll then strive to maintain this allocation of 60% equities and 40% bonds.

At Syfe, we allocate portfolio weights using a process known as Asset Class Risk Budgeting – a risk-based method of portfolio allocation whereby the overall risk of the portfolio is distributed among various asset classes. Similarly, risk budgeting is thinking about asset allocation in terms of risk instead. With a risk budgeting approach, our investment team optimises the portfolio weights of each asset class to meet the overall risk budget of the portfolio.

We have observed that when investors take up portfolios with the appropriate risk levels for themselves based on their life stage, time horizon and risk appetite, they are better able to withstand short-term noises in the market, and are more determined to stay on course for the long-term. The Asset Class Risk Budgeting process maintains the risk that an investor is comfortable with and we stay true to what they have committed to.

Keep more of your return by minimising costs through passive investing

Studies have shown over and over again that actively managed funds, also known as mutual funds or unit trusts, almost always underperform passive investments in the long run. According to the S&P Global’s SPIVA US Scorecard for 2021, more than 85% of actively managed US large-cap funds underperformed the S&P 500 over a ten year period. And while there is no way fund managers can consistently know which stocks will do well, they charge a premium for their supposed stock picking prowess.

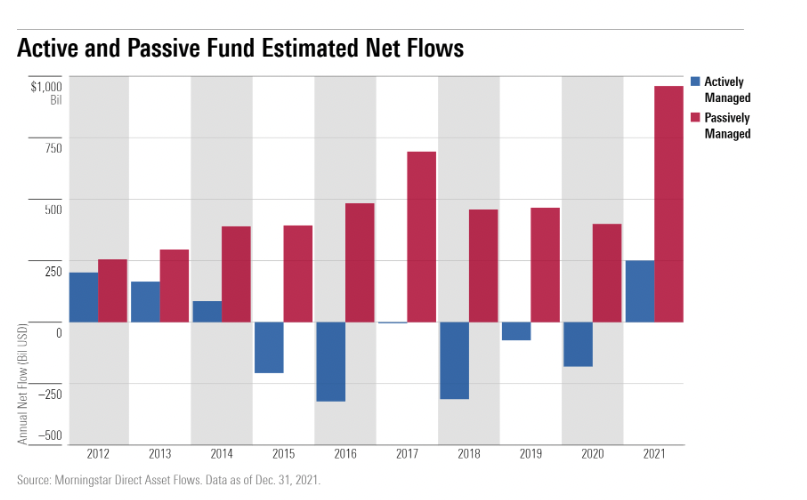

Over the years, investors are increasingly flocking to passive investments to invest at far lower fees. Passive funds have grown in popularity. In 2021, passive funds raked in $958 billion, over $700 billion more than their active counterparts.

Passive investing aims to correct this imbalance which is why Syfe uses exchange-traded funds (ETFs) as building blocks of our portfolios. Instead of paying large amounts of money to fund managers who claim they can pick the right stocks, passive investors simply pay a low fee to buy a broadly diversified basket of stocks that mimics a market index such as the Standard & Poor’s 500 index (S&P 500).

Add defensive plays to your portfolio

Surging prices can be a strain on our wallets. In addition to stocks, bonds and gold, investors should also consider other assets such as REITs which typically outperforms when inflation is moderately high. As prices rise, so do rents. This increases the amount of rental income REITs can earn. Singapore REITs (S-REITs) stand out for their resilience compared to their global counterparts. In the first quarter of 2022, the iEdge S-REIT Leaders Index gained 1.3% while global REITs fell 3.8% and the S&P 500 declined 5.5%.

In periods of high inflation, cash is not always king. With inflation at a 10-year high in Singapore, we lose purchasing power on our savings. Another option that many investors have turned to in this time are cash management solutions, to ride out the volatility. For example, we at Syfe have designed our cash management solutions to be well positioned going into a higher-rate environment. Returns have been positive and stable even as equity and bond markets sold off recently as the Fed embarks on quantitative tightening to rein in inflation. The duration of the Syfe Cash+ is also low (~6m). As these underlying bonds mature, proceeds will be reinvested into higher yielding bonds relatively quickly. Gains will be passed onto the investor in time to come.

Stay the course

The market may rally from this point on, or it may not. What we do know is that, the longer you stay invested, the better your return prospects are. In fact, if you can hold your investments for a 20-year period, you would have historically come out ahead.

Whether there’s rising inflation or low inflation, investors with well-rounded portfolios are likely to stay on course to meet their long-term goals. During times of market volatility, it becomes even more important to pay greater attention to the things one can control: diversification, asset allocation and cost.

The writer is founder and CEO of Syfe.