As parents, we all want the best for our children, and one of the greatest gifts we can provide to them is financial security. According to an NUS research, the estimated cost to raise a child in Singapore can be anywhere between $280,000-$560,000.

With higher cost of living and inflation on the rise, parents not only need to be on top of child-related expenses, but also education costs. It is thus important for you to start investing early to harness the power of compounding and give your children a head start in life.

In this article, we guide you through the process of securing their future by making decisions that align with your children’s needs.

Setting and Prioritising Financial Goals

The first step to take is to prioritise your own financial stability and long-term goals. You need to ensure that you have enough resources to support your own needs, such as emergencies and retirement, while not having to rely on your kids for your golden years.

After which, you can begin planning how much it will cost you to invest into your children’s future. These cost estimates may vary depending on the goals and desired lifestyle you have for your child.

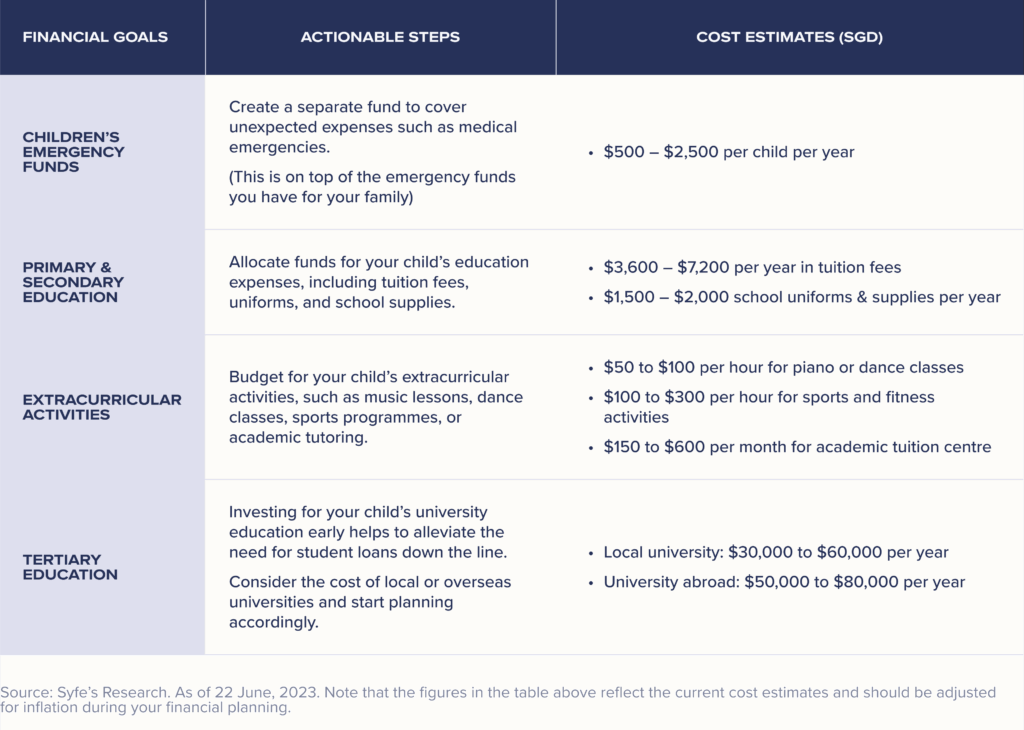

Here are some goal examples you can set for your children.

Matching Goals with Investment Portfolios

After deciding on your goals and how much money you will need, you’ll need to figure out the right time horizon and investment options for your children’s financial goals.

Every kid has different needs, so when you’re selecting portfolios, take into consideration how soon you will need the money (time horizon) and how much risk you are comfortable with.

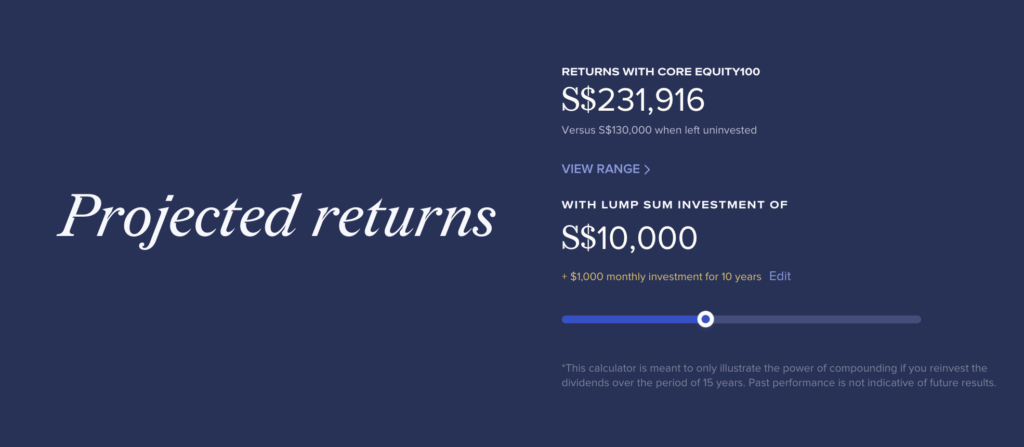

For instance, if your child is currently 5 years old, you still have over 10 years to accumulate funds before they embark on their university journey. If you plan to send them off to a university abroad in Australia, tuition alone would cost you around $200k per degree.

If you start with investing $10,000 into Core Equity100 portfolio today and contribute $1,000 every month for 10 years, you can reach your goal almost twice as fast compared to just saving alone.

However, if your child is already a teenager, you only have approximately 5 years left to plan.

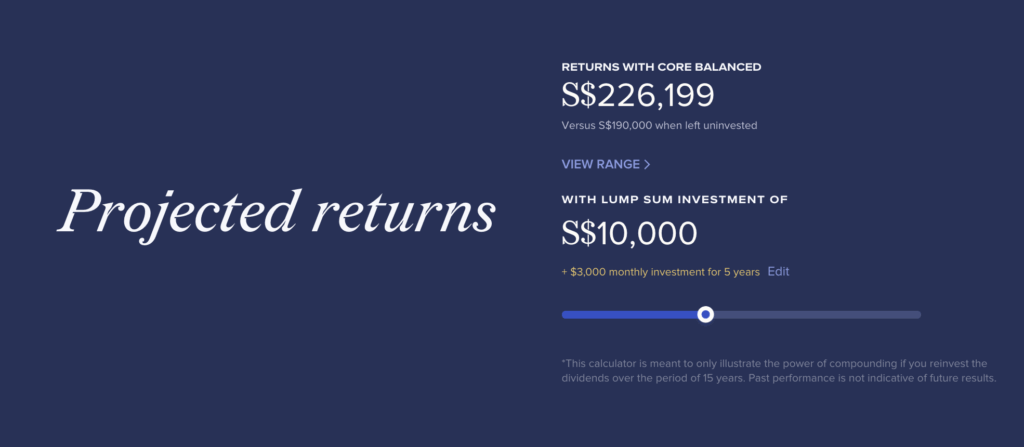

In this case, it would be more suitable for you to select a portfolio with a mid-term horizon and invest a larger sum monthly, considering the shorter time-frame available for investment growth.

For example, starting off with $10,000 in Core Balanced, and adding $3,000 every month, you’ll reach your $200k goal in 5 years.

Getting Started with Syfe for Kids

You can now join forces with your children and embark on their financial journey together with Syfe for Kids. Set investment portfolios for your child, invest on autopilot and watch their money grow overtime.

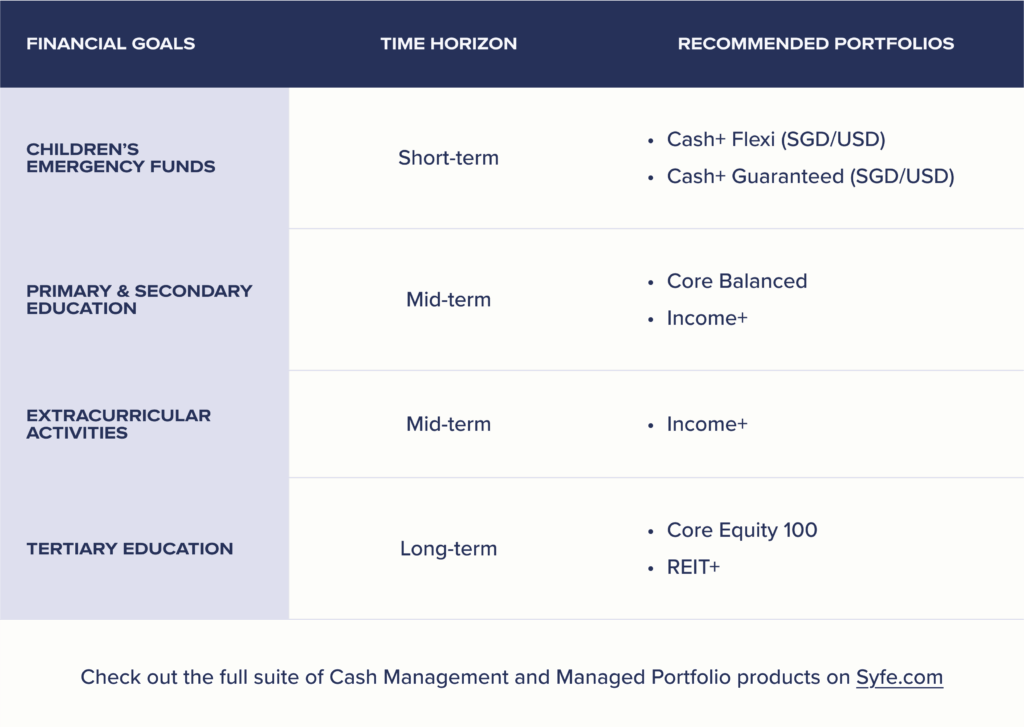

Here are some examples of how you can use Syfe portfolios to meet your children’s goals:

For short-term goals like emergency funds, you can consider a lower-risk cash management solution like Cash+ for its liquidity.

You can consider Core Balanced or Income+ for medium-term goals (4 to 8 years) such as your child’s extracurricular activities. Income+ pays out on a monthly basis so this could be used to payout your child’s allowance.

When it comes to long-term goals (more than 8 to 10 years time horizon) such as university education, it’s worth considering investments that have the potential for higher returns, such as Core Equity100 or REIT+.

Ready to begin with Syfe? Here’s how it works:

- Download the Syfe app.

- Register for an account and complete the Know-Your-Customer (KYC) steps.

- Select which portfolio you’d like to invest in.

- Fund & set regular deposit schedules to automate your investments.

- Adjust the plan as you go. Pause, withdraw, reallocate as much as you like!

What’s more, you can now tag your Syfe portfolio to your child. Once you have created your portfolio, simply:

- Press the three dots beside the portfolio name.

- Select “Tag Portfolio to Child”.

- Add your child’s photo and input their name.

Investing for your children’s future is not only crucial for their well-being but also sets an excellent example of responsible money management. Kickstart their wealth-building adventure while also providing them with hands-on education in long-term financial planning today.

Mummys Market New Client Exclusive

Are you a Mummys Market member and new to Syfe? Enjoy 6 months of fee waivers when you sign up for Syfe’s Managed Portfolios or Cash Management solutions, with promo code SYFEMM2025. Click here for full details.

You must be logged in to post a comment.