Source: 5-day price movement for 3 major markets, Kitco

Stocks start 2023 on a positive note as hopes grow of slowing inflation

Stocks had a difficult year in 2022, with all three major averages experiencing their worst performance since 2008 and ending a three-year streak of gains. The Dow was the least affected of the three indexes, declining approximately 8.8%. The S&P 500 fell 19.4% and is over 20% below its all-time high, while the Nasdaq saw a significant drop of 33.1%. Inflation and aggressive interest rate increases from the Federal Reserve had a negative impact on both growth and technology stocks and affected investor confidence throughout the year.

However, in the first week of January 2023, U.S. stocks experienced a significant rally following the release of employment data for December, which showed a slowdown in wage growth. Investors viewed this as a potential indication that Federal Reserve officials may reduce the frequency of their interest rate increases. As a result, the S&P 500 rose 2.3%, the Dow Jones Industrial Average gained 700 points (2.1%), and the Nasdaq Composite saw a 2.6% increase. Before this rally on Friday, all three major averages were on track to end the week with losses.

Despite the short rally, Economists predict the global economy will grow just 2.4% next year, the lowest in three decades besides the disastrous 2009 and 2020. In fact, economists at both Citi and Abrdn forecast the UK and Europe will likely enter the new year in a recession, with the US following in the second half of 2023.

So, what does 2023 look like for investors?

Topic #1: Unpacking the Federal Reserve’s meeting minutes

In the past week, the Fed’s meeting minutes from their Dec 13-14 policy meeting was released on wednesday. “Participants generally observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time,” the meeting summary stated. In essence, this meeting primarily reaffirmed their current stance of continuing to control the cost of credit (interest rates) to control inflation as policymakers were worried that pace of price increases were expected to run faster than anticipated. The minutes also reflected that no FOMC members expect rate cuts in 2023, despite market pricing

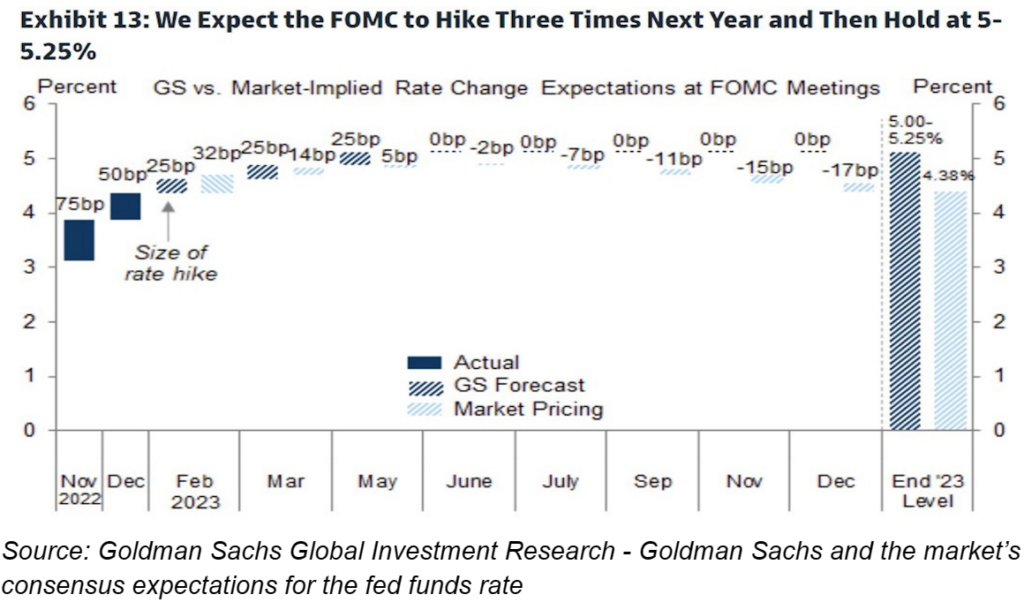

Does Goldman share the view that interest rates have peaked?

Naturally, it is difficult to predict with certainty what the Federal Reserve will do with regards to interest rates in 2023, as it depends on a variety of factors such as the state of the economy and the level of inflation. According to Goldman Sachs, their analysts expect inflation to decline, but they are unsure if it is sufficient to warrant the Fed to start reducing interest rates.

In fact, Goldman Sachs predicts that the Fed will increase the federal funds rate three more times, in increments of 0.25 percentage points, in February, March, and May, and then maintain this rate, followed by some rate cuts to 4.4% by the end of 2023. Deviation from this may happen if something unexpected occurs, such as a significant economic recession leading to an increase in unemployment. Ultimately, the Fed will make its decision based on its assessment of the economic situation at the time and its mandate to maintain price stability and full employment.

Topic #2: Likelihood of a US recession

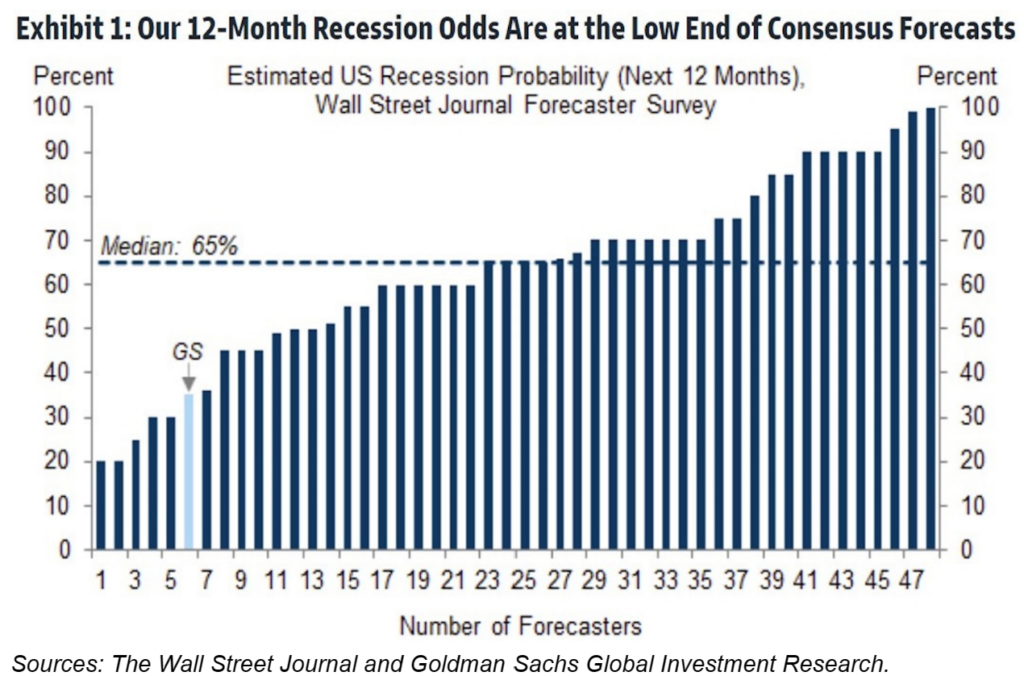

Following the release of the Fed’s meeting minutes, this Wall Street Journal 12-month recession odds consensus puts the probability of a US recession in the next 12 months at a hefty 65%, while Goldman sees it at just 35%. Like Goldman, some investors are hoping for a soft-landing – the one in which those interest rate hikes from the Federal Reserve manage to slow the economy just enough to bring down inflation, but not so much that it pushes the whole thing into a recession.

Why do some investors believe that a soft-landing is possible?

Firstly, some investors believe that a recession is not necessary to address rising inflation, and that a prolonged period of slower economic growth will be sufficient to address imbalances in the demand and supply of goods and services, including the mismatch in the labor market that has contributed to rising prices.

Secondly, they also expect a shorter lag time, or delay between interest rate hikes and their impact on economic growth, and anticipate that the negative effects of these hikes will dissipate over 2023, resulting in a more resilient outlook for economic growth. This is expected to occur as the combined effects of monetary and fiscal policy tightening, which took place primarily in the first half of 2022, begin to fade as the year progresses.

Ultimately, finding the sweet spot with monetary policy (i.e interest rate changes) to bring about this outcome is no easy feat and uncertainty about how sticky inflation could end up being is still top of mind.

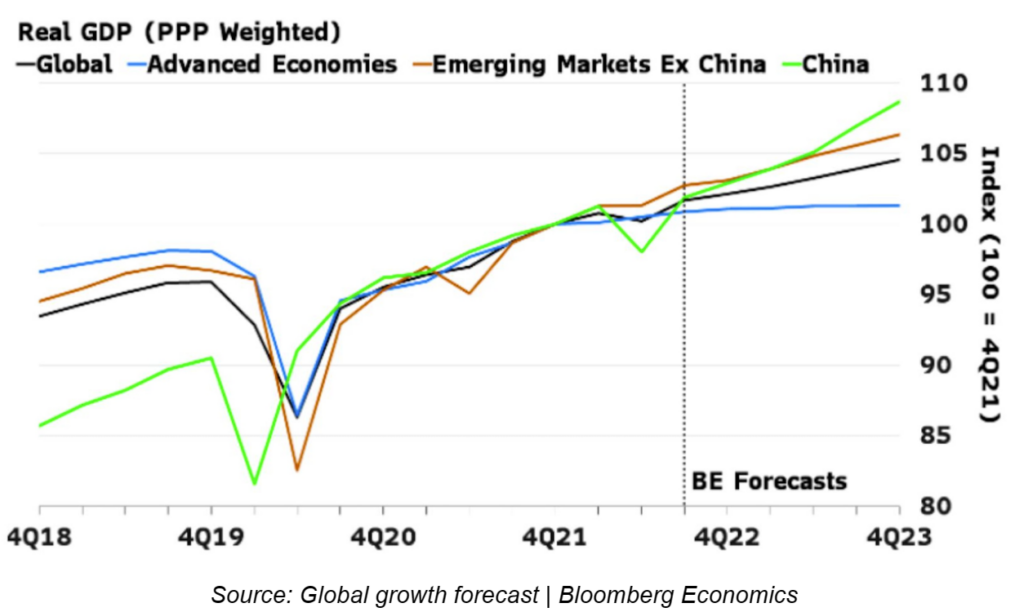

Topic #3: China unleashed

Can China dodge the recession bullet?

Evidently, the KraneShares CSI China Internet ETF (KWEB) is up 15.39% and CSI 300 is up 2.76% respectively in the past week. Moreover, Ant Group has received approval from the China Banking and Insurance Regulatory Commission to increase the registered capital for its consumer unit to CNY 18.5 billion ($2.8 billion), up from CNY 8 billion. This news follows Ant’s efforts to restructure its business after the suspension of its initial public offering in late 2020.

Does this mean that things may be turning around for the world’s second largest economy?

As discussed in last week’s market update, China is relaxing its uncompromising zero-Covid stance. Economic growth in China is expected to be over 5% next year, potentially due to the release of pent-up consumer demand and the impact of the government’s business-supportive policy plans.

Ultimately, whether China dodges the recession bullet depends on the reaction to economy-boosting rate cuts to the mix and the rate at which they are able to bounce back from the aftershocks of lockdown-induced supply, war-induced energy shortages and other central banks’ relentless rate hikes.

Does your investment portfolio reflect this bullish perspective or are you less optimistic?

| Index | Level | 1 Week | 1 Month | From Jan 1 2023 |

| S&P 500 (US Stocks) | 3,895 | 1.72% | -0.99% | 1.86% |

| Nasdaq 100 (US Tech Stocks) | 11,040 | 1.89% | -3.98% | 1.64% |

| CSI-300 (Chinese Stocks) | 3,980 | 2.76% | 0.57% | 2.39% |

| Bitcoin (in USD) | 16,946 | 1.68% | 0.62% | 2.05% |

Source: Google Finance, as of 7th January, 2023.

You must be logged in to post a comment.