While Singapore grapples with rising living expenses, global instability, and rapid technological shifts, Singapore Budget 2024 came at a crucial time. On February 16th, Deputy Prime Minister and Finance Minister Lawrence Wong announced the government’s fiscal planning for the year ahead. Seeking a balance between addressing present challenges and engineering tomorrow’s sustainable, innovation-led society, the Budget’s theme “Building our shared future together” takes on even greater significance.

So, what’s in it for you? Here are our top 3 takeaways from Budget 2024 and how they might affect your personal finances.

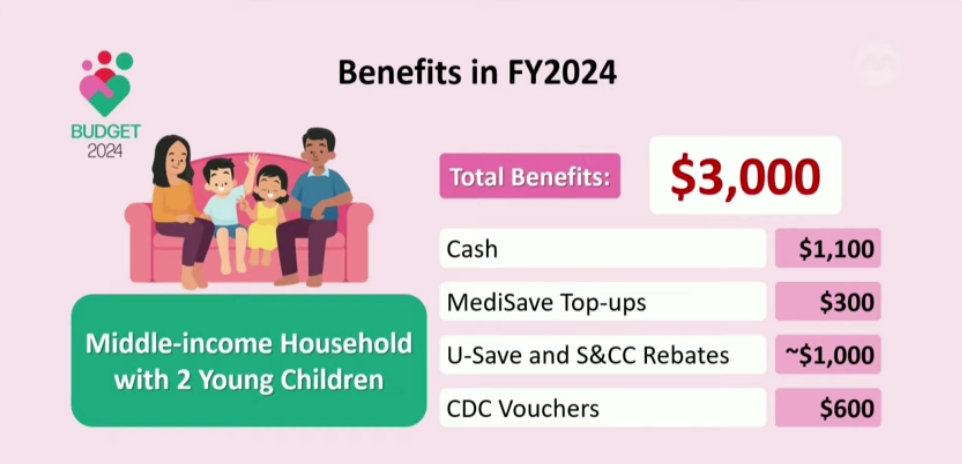

1. More vouchers, cash payouts, and rebates for individuals and households

To help Singaporeans dealing with the rising prices, temporary relief measures are one of the key pillars of this year’s budget. All Singaporean households will get S$600 in CDC vouchers, half of which will be given out in June this year and other half in January 2025. Eligible HDB households will receive S$550 to S$950 in U-save rebates depending on the size of their flat, and will also get services and conservancy rebates to offset two to four month’s charges.

On top of that, Singaporeans aged 21 and above in 2024, who do not have one property and with an accessible income of up to S$100,000 will receive a cash payment of between S$200 to S$400. There are other rebates and credits as well, such as personal income tax rebate capped at S$200, National Service LifeSG credits of S$200, CPF Medisave top-ups for all Singaporeans, and bonuses in CPF special account(SA) for Singaporeans born in 1973 or earlier.

Implications for you:

All these benefits could add up to a significant amount of savings for the year. For instance, a middle-income family with 2 young children may see benefits totalling up to S$3,000. That said, these measures are designed to provide only a short-term buffer.

- It’s important for you to carefully plan your household budget, taking into account the rising costs.

- Utilise the CDC vouchers and rebates for essential expenses and opt for more affordable alternatives when possible to maximise these benefits.

- Furthermore, consider putting the extra funds from cash payouts and rebates into investments. With compound interest, a modest initial investment, like S$20,000 with a 10% annualised return over 30 years, could grow into S$348,988.

2. Changes to CPF

There are some significant changes to the CPF accounts announced in the Budget 2024:

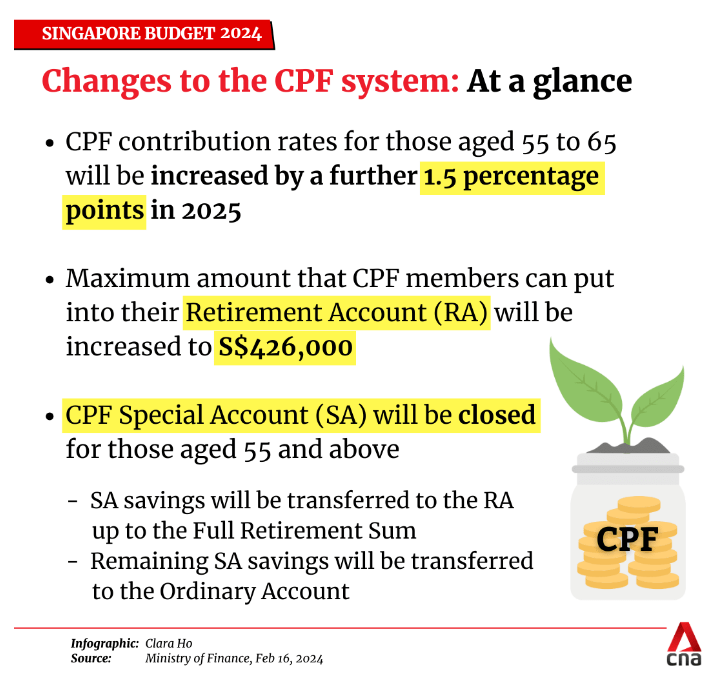

- CPF contribution rates for those aged 55 to 65 will be increased by 1.5% in 2025. Currently, the contribution rate for those aged above 55 to 60 stands at 31% of monthly wages.

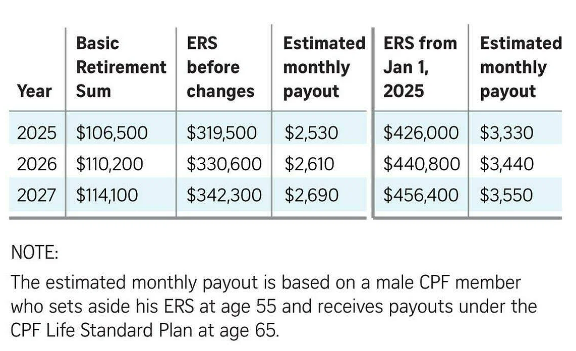

- The CPF Enhanced Retirement Sum (ERS) will increase from three to four times the Basic Retirement Sum in 2025. The ERS, the maximum amount people can contribute to their CPF Retirement Account (RA) for higher payouts, is currently S$308,700 for 2024 but will rise to S$426,000 from 2025.

- CPF SA will be closed for those aged 55 and above. SA savings will be transferred to RA to the Full Retirement Sum (FRS). Remaining SA savings will be transferred to the Ordinary Account.

Implications for you:

- Close the loophole for “CPF shielding”. In the past, some CPF members aged 55 and above used the “CPF shielding” hacks to take advantage of the high interest of 4% in the SA, while being able to withdraw the money from the SA at any time. SA closure at age 55 will close this loophole.

- Higher potential payout from CPF. Having more money in a CPF RA can translate to higher monthly payout. A CPF member at age 55 with an ERS of S$426,000 could receive monthly payouts of S$3,330, compared to S$2,530 for a member with the current ERS of S$319,500. Many of us tend to overlook our CPF in our financial planning, yet CPF can be a useful tool. For instance, topping up your SA can earn an interest of 4% per annum while enjoying tax relief of up to S$8,000 each year. It is advisable to include CPF as part of your financial planning.

- Do not depend on CPF alone for retirement. One drawback is that CPF accounts have many restrictions. You can only withdraw money from age 55, and the rules can change. There is also a cap on how much you can put into your SA/RA account. The Supplementary Retirement Scheme (SRS), a voluntary savings scheme, can be used to complement your CPF savings while enjoying tax benefits. If you are looking to build passive income, Syfe Income+ could be suitable. The portfolios invest in globally diversified bonds and offer a monthly payout of 4.0% to 6.0% p.a.

3. SkillsFuture Level-Up Programme

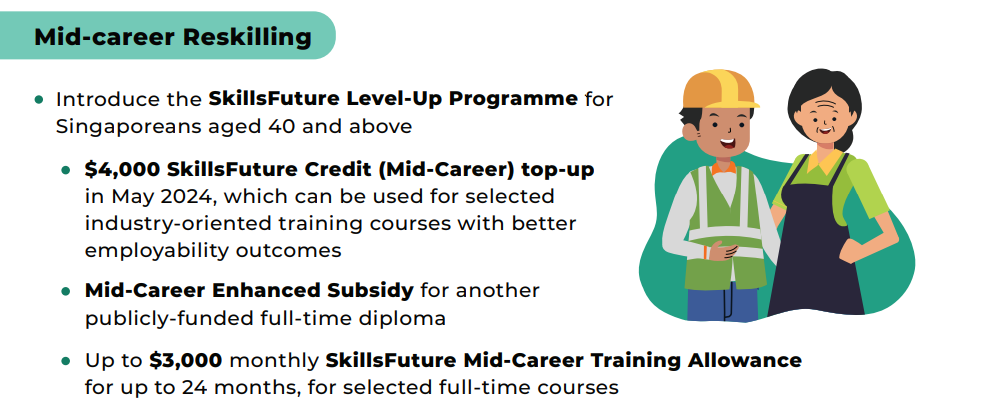

For Singaporeans who are aged 40 and above, these benefits are for you! The SkillsFuture Level-up Programme offers support for those aged 40 and above to upskill and reskill.

The programme includes a S$4,000 SkillsFuture Credit, in addition to the existing S$500 credit. The top-up will be given out in May this year. The credits can only be used for training with “better employability outcomes”, including part-time and full-time diplomas, post-diplomas, undergraduate programs, and courses for the Progressive Wage Model sectors. Those younger than that will get the top-up credit when they turn 40.

For those aged 40 and above who wish to pursue another full-time diploma at polytechnics, ITE, or arts institutions starting from the academic year of 2025, the government will provide a monthly training allowance. It will be equivalent to 50% of one’s average income over the latest 12-month period, capped at S$3,000 per month. Everyone can receive up to 24 months of such training allowance throughout their lifetime.

Implications for you:

The best investment you can make is an investment in yourself…The more you learn, the more you’ll earn. – Warren Buffett

- Enhance Career Mobility and Security. Upskilling and reskilling with SkillsFuture Credit and the training allowance are all about keeping up with the ever-changing job market, especially for those of us hitting our mid-career stride. This strategy could open doors to higher-paying jobs or exciting new fields, boosting both our wallets and job satisfaction in the long run.

- Reduce financial burdens to pursue a full-time study. The training allowance—getting 50% of your average income (up to S$3,000 a month) is a game-changer for anyone who plans to dive back into full-time study. This provides a financial safety net, helping cover living costs so you can focus on learning, not earning.

- Plan carefully. Dive deep into your research to find courses that not only fuel your passion but also offer promising future opportunities. Make the most out of the credits and allowance available to you, maximizing their potential to your advantage.

From expanding social support to equipping citizens with in-demand skills to powering companies and industries into the next decade, the Budget 2024 has mapped out careful allocation of resources aimed to future-proof this island nation. In light of these changes, it’s an optimal time to refine your financial goals, reassess your retirement readiness, and adjust your priorities to ensure your financial roadmap is future-proof too.

Read More:

Syfe Investment Outlook 2024 – Your New Playbook as the Fed Pivots

How To Earn $1,000 In Passive Income Each Month: A Singaporean’s Guide

You must be logged in to post a comment.