Singapore’s real estate investment trusts (S-REITs) extended their strong rally into the fourth quarter of 2025, delivering superior returns amid an improving macro backdrop.

After a robust Q3, S-REITs entered Q4 with positive momentum supported by healthy fundamentals and easing interest rate pressures. By mid-December, S-REITs were on track for their best annual performance since 2019, with full-year total returns of nearly 16% (including dividends).

This marked a significant rebound from the sluggish performance of 2023, and notably outpaced many global REIT markets, and far surpassed USA REITs (FTSE Nareit All REITs Index) which saw a 1.7% total return.

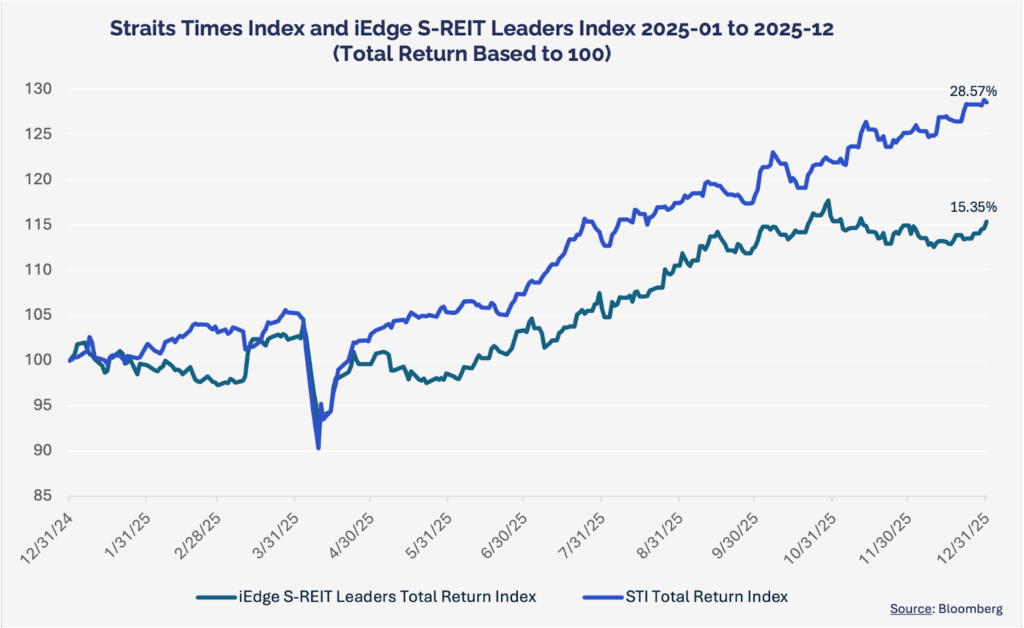

The Straits Times Index (STI) still led with a 28.6% total return in 2025, boosted by bank stocks, but S-REITs’ double-digit gains reinforced their appeal as high-yielding instruments in a stabilising rate environment.

Driving Factors Behind S-REITs’ Q4 performance

Several factors underpinned S-REITs’ Q4 performance.

Interest rate outlook turned supportive

The US Federal Reserve implemented three 25 bps rate cuts in 2025 (starting with a cut in September), and market consensus expects further easing in 2026. This shift alleviated a major headwind for global REIT operations, valuations and financing costs.

Singapore’s local rates and bond yields likewise stabilised or fell, increasing the yield spread advantage of S-REITs and drawing income-seeking investors back into the sector. Average market cap weighted S-REIT dividend yields hover around 5.7%, maintaining a healthy ~4% premium over 10-year Singapore government bond yields. With Singapore T-bill yields declining to ~1.7-1.8% by late 2025 (from ~3% at the start of the year), the relative attractiveness of S-REIT payouts increased markedly.

S-REIT operational fundamentals remained solid

Operational fundamentals for S-REITs stayed strong in Q4. Companies reporting Q3 results saw overall occupancy rates stay high (generally 95%–99% for prime assets across retail, office, and logistics) and rental reversions were positive, meaning many landlords could renew leases at higher rents.

On the retail side, shopper traffic and tenant sales improved on the back of rising tourism and domestic consumption, enabling retail REITs to secure mid-to-high single-digit rent uplifts on renewals. CapitaLand Integrated Commercial Trust’s suburban malls, for example, enjoyed a 7.8% positive rental reversion in 2025, with healthy tenant retention of 80%. Meanwhile, hospitality assets benefited from a surge in travel, and hotel and serviced residence REITs reported higher occupancies and room rates as tourist arrivals climbed and corporate travel normalised.

These encouraging fundamentals bolstered confidence that REIT distributions will remain resilient, or resume growth after the dip in 2023. Indeed, distributions per unit (DPU) have started to turn the corner. After widespread DPU declines in 2023-24, most REITs returned to positive DPU growth in 2H 2025 as financing costs peaked and revenue streams strengthened.

Valuation and Inflows

Another supportive factor was valuation and inflows. Despite the price recovery, S-REIT valuations still looked attractive relative to history. As of end 2025, the sector traded at a weight average of 0.98x price-to-book on average (still below the historical ~1.0x-1.1x norm), with many REITs still at sizable NAV discounts. This, coupled with the wider yield spreads, enticed investors positioning for further upside. Notably, retail investors were net buyers of S-REITs throughout 2025, adding nearly S$1 billion of net retail inflows even as institutions were net sellers. In Q4, this trend persisted, as yield-hungry local investors continued rotating into REITs, providing steady demand. The top flows were to Mapletree Industrial Trust (ME8U), Mapletree Logistics Trust (M44U), NTT DC REIT (NTDU), CapitaLand Ascendas REIT (A17U), and CapitaLand Ascott Trust (HMN), according to SGX data.

The S-REIT rally was broad-based, and by end-Q4, all but five S-REITs were in positive territory for the second half, and over 50% of REITs saw double-digit percentage gains in H2. While large-cap, high-quality names led the charge, even some previously laggard mid/small-cap REITs (particularly those with high yields) bounced off multi-year lows as sentiment improved.

Looking ahead, S-REITs enter 2026 on a strong footing. The combination of high-yield income and potential capital gains positions them attractively amid expectations of further monetary easing. The sector’s 2025 rebound demonstrated its leverage to falling interest rates, and this is a theme likely to persist into Q1 2026. Investors are now increasingly confident that the worst of the rate-driven valuation compression is over. Further SORA drops (or even continued current rate stability) could be a major catalyst for S-REITs in 2026, especially those that were hardest-hit by high interest costs. With global inflation softening and central banks adopting a more dovish stance, the macro winds remain in S-REITs’ favour going into 2026.

Singapore’s Safe Haven Asset Class Shines

The closing quarter of 2025 provided a supportive macro backdrop for S-REITs. Globally, inflation moderated and central banks either began cutting rates or adopted a more dovish tone, reducing the threat of further rate hikes (except for Japan).

In Singapore, economic indicators were favourable, as GDP growth remained positive (albeit modest), unemployment stayed low, and consumer spending was healthy, all of which underpinned tenant sales and rent payments. Notably, tourism saw a strong uptick and international visitor arrivals and spending in Q4 approached or exceeded pre-pandemic levels, boosting retail REITs (e.g. higher mall footfall and luxury sales) and hospitality REITs (higher hotel occupancy and room rates).

Singapore’s interest rate environment eased alongside the USA. The 3-month SORA and SIBOR rates levelled off after peaking mid-year, and the Singapore 10-year bond yield declined in Q4, reflecting improved investor sentiment. This easing of financing costs came just in time as many REITs had already termed out debt at fixed rates, but the prospect of refinancing in a lower rate setting boosted confidence in their mid-term DPU growth.

| Index | Q1 2025 Total Return | Q2 2025 Total Return | Q3 2025 Total Return | Q4 2025 Total Return | 2025 Total Return |

| iEdge S-REIT Leaders Index | 2.3% | 1.0% | 9.0% | 2.4% | 15.3% |

| Straits Times Index (STI) | 5.3% | 1.9% | 10.2% | 8.7% | 28.6% |

Source: Bloomberg

From a policy perspective, the Singapore government and regulators introduced initiatives in 2025 to bolster the REIT market’s vitality. In Budget 2025, authorities extended key tax concessions for S-REITs and REIT ETFs to 31 Dec 2030, removing near-term uncertainty around these incentives. The extension preserves the tax transparency treatment of S-REITs (no double taxation on REIT income) and keeps in place the 10% concessionary withholding tax for foreign investors in REITs, reaffirming Singapore’s commitment to remain a competitive REIT listing hub.

Moreover, the scope of qualifying income for tax transparency was broadened, for example, ancillary co-working and co-location rental income counted as qualifying from mid-2025. These refinements encourage S-REITs to diversify offerings (like flexible office space) without tax leakage.

Beyond taxation, the Monetary Authority of Singapore (MAS) and SGX rolled out market-friendly measures, and a new SGX “dual listing” framework with Nasdaq was announced, aiming to attract high-growth companies (and possibly foreign REIT listings) by enabling a concurrent SGX-Nasdaq listing process. Additionally, SGX reduced the minimum board lot size from 100 to 10 units for high-priced securities, improving retail accessibility to blue-chip stocks and REITs.

These initiatives, alongside MAS’ S$5 billion Equity Market Development Programme (EQDP) grants to defray REIT IPO costs and to fund and expand research coverage, form a broader push to revitalise Singapore’s equity market, and the strategy appears to have already borne fruit with two new REIT IPOs in 2025.

Q4 Dashboard: What Moved the Tape

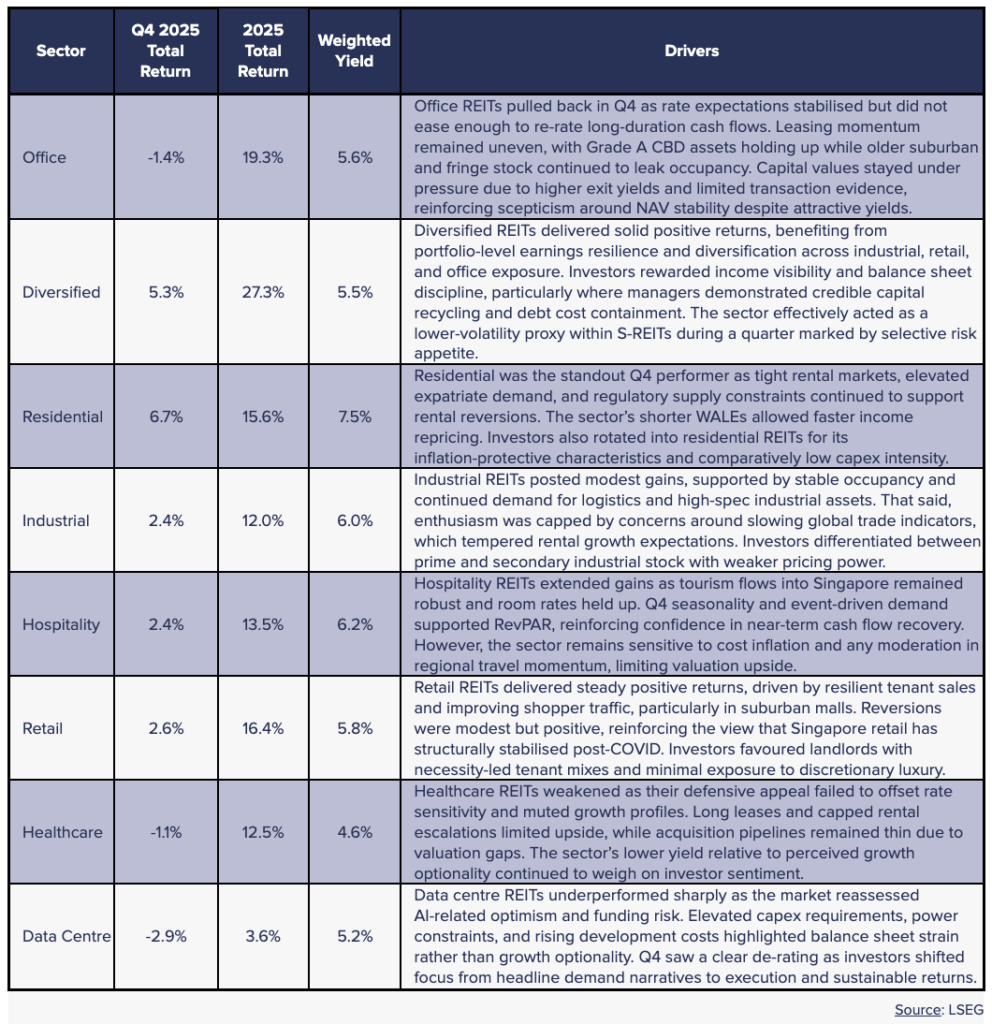

Most REIT sub-sectors in Singapore ended Q4 with a market capitalisation weighted positive total return, but Office, Healthcare, and Data Centres experienced a down quarter.

Source: LSEG

Outlook for Q1 2026

Q1 2026 is poised to extend the S-REIT recovery, though perhaps at a moderated pace as markets digest 2025’s gains. The consensus view is that the USA’s Federal Reserve could deliver two more 25 bps cuts in 2026, and other central banks (ECB, BOE, etc.) are similarly potentially tilting toward easing. This should translate into lower borrowing costs for REITs over time, Fitch Ratings projects S-REITs’ average interest cost (3.5% as of Q3 2025) will fall further in line with USA rate reductions in 2026. If bond yields continue to pull back in Q1 on confirmed rate cuts, we could see another leg of price rally for S-REIT heavyweights, as their valuations re-rate upwards with a lower cost of debt as a key tailwind.

That said, the Q1 rally might be more selective. Much of 2025’s easiest gains have been realised, so investors are likely to differentiate more based on quality and growth prospects. Large-cap REITs with strong sponsors and prime assets, which dominate indices and products like Syfe’s REIT+, should continue to attract inflows given their stability.

Sectors with clear growth drivers could lead in Q1. For example, the outlook for retail REITs is favourable due to their continued rent reversions and limited new mall supply, supporting earnings growth. Logistics and data centre REITs may also stay in vogue as structural demand (e-commerce, cloud/AI infrastructure) fuels rental resilience; these segments are seeing cap rates compress as investors bid up prime properties.

Notably, overseas-focused REITs that lagged (due to forex and higher foreign rates) might play catch-up if rate cuts materialise abroad. European and US-focused S-REITs, which suffered outsized declines in 2025, could revive in 2026 as conditions normalise.

Risks to Watch in Q1 2026

This includes any renewed global growth concerns, geopolitical impacts, or black swan events that could stoke volatility. While Singapore’s economy remains on a stable growth path (with modest GDP expansion and robust employment supporting property markets), an external slowdown or geopolitical flare-up could temper investor risk appetite.

Additionally, S-REITs’ operating metrics bear monitoring e.g., office REITs could face pressure if new supply or tech sector downsizing hits rents, and hospitality REITs might see seasonally softer Q1 tourism after the holiday peak.

However, the overall sector outlook is positive, with supportive fiscal and monetary conditions in Singapore, paired with the S-REITs’ proven resilience and income appeal, suggest that Q1 2026 will likely bring continued steady performance. Barring shocks, we expect S-REITs to deliver mid to high single-digit total returns in 2026, which would represent a solid outcome following 2025’s rebound. Investors can therefore approach the new year with cautious optimism that S-REITs will continue to shine amid converging tailwinds.

REITs to Watch

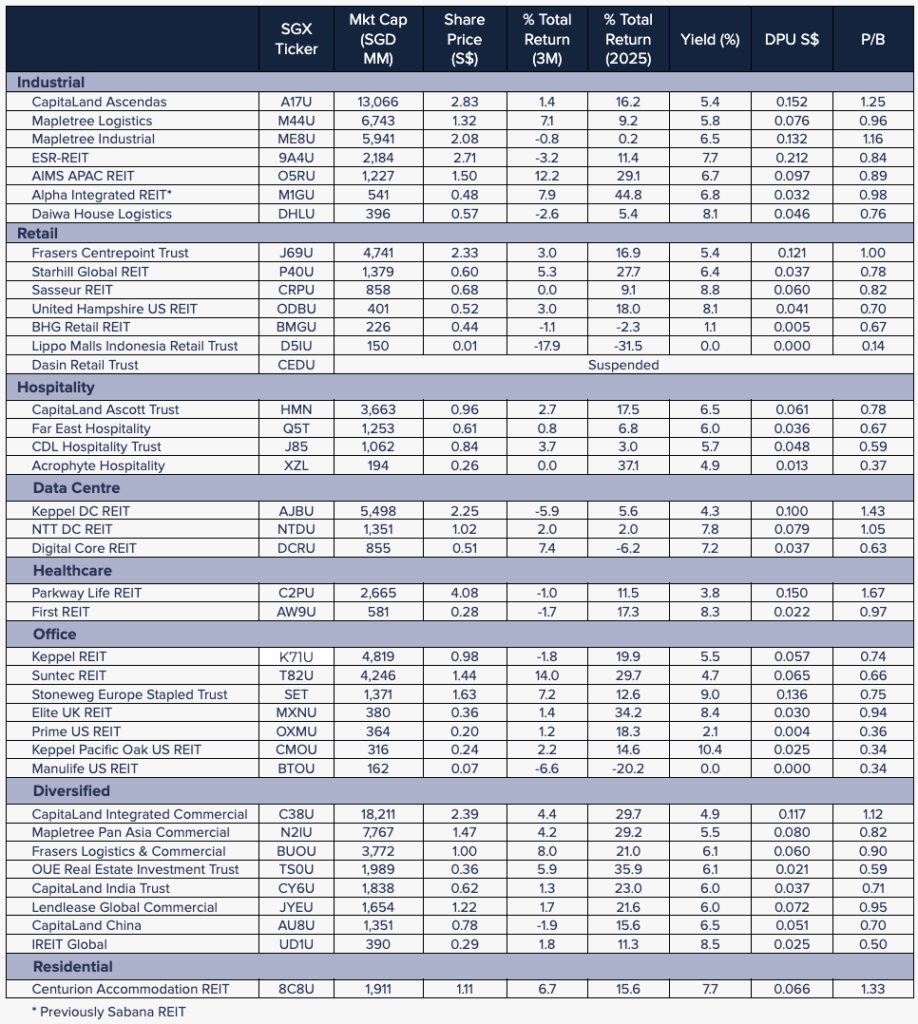

Beyond the heavyweights, several small and mid-cap S-REITs stood out in Q4 2025 for their performance and attractive yields. Below are five such REITs (in no particular order) that warrant attention, given their recent developments and outlook:

Stoneweg (SET) Q4 Price +7.2%, Yield 9.0%

Stoneweg Europe Stapled Trust’s business update for Q3 2025 showed distributable income rising 17% quarter-on-quarter to about EUR20.9m, supported by rising rents and a one-off income item. The trust has been active on portfolio rebalancing, divesting selected properties in Italy while funding growth via a EUR300m green bond issue. Operational performance is driven by diversified European logistics and industrial assets, though macro uncertainty in Europe and interest rate risk remain headwinds.

Management continues to prune non-core assets while scaling through selective acquisitions. Balance sheet discipline has been maintained despite growth, aided by diversified funding including green bonds. Income quality is improving as the portfolio tilts toward higher-spec assets. It is one to watch for earnings momentum, though European macro and execution risk remain key sensitivities.

First-REIT (AW9U) Q4 Price -3.5%, Yield 8.3%.

First REIT posted a Q3 2025 distribution per unit of 0.52 Singapore cents, bringing 9M DPU to 1.65 cents, down about 7.3% year-on-year. The decline is chiefly due to currency translation losses from weakening Indonesian rupiah and Japanese yen, coupled with a larger unit base from fee issuances. Rental income in local currencies grew modestly across Indonesia and Singapore, but overall revenue and NPI slipped slightly year-on-year. The trust’s balance sheet remains serviceable with gearing in the low-40s and no immediate refinancing pressure, though FX volatility and rental arrears at an Indonesian tenant (PT Metropolis Propertindo Utama) present execution risk.

First REIT’s Q3 2025 results showed stable underlying operations but declining distributions due to currency weakness and a higher unit base. Core healthcare assets continue to perform in local currency terms, supporting long-term defensive characteristics. Gearing remains manageable, with no near-term refinancing stress. The valuation already reflects significant pessimism around foreign exchange risk. It is a REIT to watch for any recovery driven by currency stabilisation or improved hedging outcomes.

Digital Core REIT (SGX: DCRU) Q4 Price +7.4%, Yield 7.2%.

Digital Core REIT’s Q3 FY2025 distributable income came in at US$35.2m, up 1.9% year-on-year, with gross revenue and net property income rising sharply driven by portfolio scale. Occupancy held high at 98%, reflecting resilient demand for mission-critical data centre space amid continued AI-driven workload growth. The company currently has 11 data centres (100% freehold), based in the USA (43%), Germany (33%), Japan (13%), and Canada (11%). Operational momentum is solid and the company expects AI demand to sustainably contribute to digital spending. Demand remains strong in key markets and datacenterHawk research shows 0.3% colocation vacancies in the globe’s most important data centre market of Northern Virginia. datacenterHawk saw average wholesale kW per month prices up to US$225 in 2025 from 2024’s US$210, and average hyperscale kW prices per month of US$130 up from US$110 in 2024.

Digital Core REIT’s debt is 86% fixed, with a weighted maturity of 4 years, an average cost of 3.5%, and an aggregate leverage of 38.5%.

The company repurchased 1.8 million units at an average price of S$0.565, which was 0.1% accretive to DPU.

Revenue and net property income trends remain positive despite higher funding costs earlier in the cycle. Asset quality and tenant profile underpin cash flow resilience. Interest rate pressures are easing, improving forward distribution visibility. It is one to watch as data centre fundamentals normalise after sector de-rating.

Suntec REIT (SGX: T82U) Q4 Price +12.5%, Yield 4.7%

Suntec REIT is increasingly shaping up as a stabilisation-and-recovery story rather than a structural laggard. After several years of pressure from weak office demand, elevated vacancy, and capital management overhangs, Q3 results provided clearer evidence that the worst of the operational reset may be behind it. Leasing momentum in the Singapore office portfolio has begun to stabilise, with occupancies no longer deteriorating materially and incentives showing early signs of peaking.

At the same time, Suntec’s retail assets (24% of income) continued to perform steadily, supported by resilient footfall and tenant demand in prime mixed-use locations. This retail contribution has played an important role in smoothing earnings volatility while the office portfolio (71% of income) works through its recovery phase. The integrated nature of Suntec’s assets remains a differentiator, providing diversified income streams within a single platform rather than reliance on a pure office rebound.

From a financial perspective, Suntec has been disciplined in prioritising balance sheet stability and portfolio optimisation over aggressive growth. Asset enhancement initiatives and selective divestments have helped improve portfolio quality and reduce execution risk. Rental reversions have substantially improved with Singapore at 8.5% for office and 8.6% for retail. And Australia markedly up at 11.9% While rental growth remains modest, the trust’s distributions are increasingly underpinned by operational normalisation rather than temporary measures.

Valuation continues to reflect scepticism around the office sector, but this also creates optionality. Any sustained improvement in Singapore office demand, combined with greater interest rate visibility, would meaningfully support sentiment. Q4 operations did not mark a full turnaround, but it reinforced that Suntec is transitioning from repair to stabilisation, making it a credible watchlist name for investors looking ahead to further office recovery into 2026.

Elite UK REIT (SGX: MXNU) Q4 Price +1.4%, Yield 8.4%.

Elite UK REIT is a defensive income story that has quietly proven its resilience through one of the most challenging periods for UK office real estate in decades. While sentiment toward the sector has remained weak, Elite’s differentiated positioning, with a portfolio predominantly leased to UK government and public-sector tenants, has continued to underpin defensive cash flows and high income visibility. Long-dated leases and mission-critical occupancy have insulated the trust from the leasing stress and tenant churn affecting much of the broader office market.

Q3 results reinforced the durability of Elite’s operating fundamentals. Portfolio occupancy remained stable, and distributions continued to be supported by predictable rental income rather than short-term market recovery assumptions. In an environment where investors have become increasingly selective about income quality, Elite stands out for the reliability of its cash flows rather than growth. This has allowed the trust to sustain an attractive distribution yield of 8.4%, despite persistent valuation pressure across UK office assets. Its interest coverage ratio also improved to 2.7x in September 2025 from 2.5x at end-2024, with no refinancing due until 2027

While asset values remain sensitive to interest rate expectations, this sensitivity also creates optionality. Any stabilisation or easing in UK rates would directly support valuation recovery without requiring material operational change. Importantly, Elite’s risk profile is driven more by macro conditions than by asset-level weakness, which distinguishes it from more challenged office REITs.

Elite UK REIT remains a compelling watchlist name for income-focused investors seeking offshore diversification and defensiveness. The quarter did not deliver a catalyst-driven re-rating, but it confirmed that the trust’s conservative positioning and high-quality tenant base continue to deliver reliable income, positioning it well should macro conditions turn more supportive into 2026.

Honourable Mentions

Other notable mid-cap S-REITs include AIMS APAC REIT (O5RU), a high-yield industrial player known for savvy management and a 6.7% yield (it delivered stable Q3 results and is expanding in Australia). Frasers Logistics and Commercial Trust (BUOU), a well-diversified industrial/commercial REIT with pan-Asia/Europe exposure trading at an attractive 6.1% yield after de-risking its portfolio. Sasseur REIT (CRPU), which owns outlet malls in China and could see a boost if Chinese consumer spending rebounds in 2026 (it offers an 8.8% yield and had improving Q3 sales at its malls). Finally, Far East Hospitality Trust (Q5T) deserves a nod, as Singapore’s pure-play hotel REIT, it rode the tourism wave in 2025 and offers 6.00% yield and might benefit from consolidation in the hospitality sector. Each of these has unique catalysts (be it potential acquisitions, recoveries, or sponsor activities) and delivered noteworthy performances in the past quarter.

Access the full report here.

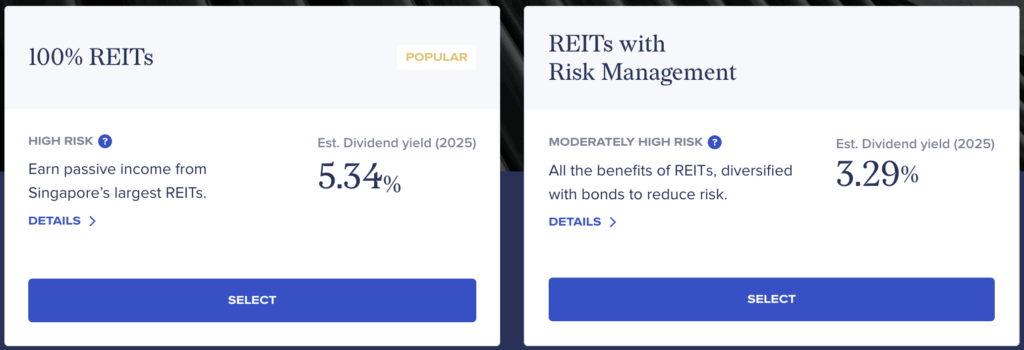

Syfe’s REIT+ Portfolio: The Smart Way to Own S-REITs

REIT+ is a managed portfolio that closely tracks the iEdge S-REIT Leaders Index, essentially representing the top Singapore REITs by market cap and liquidity.

In Q4 2025, the REIT+ portfolio continued to perform robustly, aligning with the broader S-REIT market’s strength and delivered +2.0%. It outperformed its benchmark and ended 2025 on a strong note, delivering consistent dividends and capital appreciation in line with the S-REIT market recovery.

The portfolio’s diversified exposure to Singapore’s largest REITs provided both steady dividend income (with a 5.3% yield) and participation in the capital gains of the sector’s rally. The heavy weighting towards high-quality, large-cap REITs (sponsored by the likes of CapitaLand, Mapletree, and Keppel) lent the portfolio resilience amid any small-cap volatility. By end-2025, all constituents in the REIT+ basket had positive total returns for the year, and the portfolio as a whole notched a 16.6% total return outperforming the benchmark iEdge S-REIT Leaders Index.

Entering 2026, the S-REIT outlook remains positive, and REIT+ is positioned to continue benefiting from the sector’s uptrend. Its focus on large-cap REITs means it continues to offer a convenient, diversified ride on the S-REIT rally, delivering reliable income even if market conditions turn choppy.

The REIT+ portfolio strategy, sticking to quality REITs and reinvesting in the index, has proven its worth in 2025’s rebound, and should continue to deliver steady dividends and participation in S-REITs’ growth in Q1 2026 and beyond.

You must be logged in to post a comment.