The first half of 2025 marked a turning point in global markets. After years of US equity dominance, international markets surged ahead, reflecting deeper structural shifts. As we look toward the second half, we believe the investment portfolios will be shaped by four key themes.

- Theme 1: Global Rotation & Weakening USD

We expect the USD to continue weakening in the H2 2025, as rate differentials narrow. Historically, this is a backdrop that favours EM outperformance. We’re also positive on select US sectors, particularly Tech, Industrials, and Financials, which can benefit from robust AI investment and Trump administration’s pro-business policies. - Theme 2: Growth Slowing, Not Crashing

Global growth is cooling, not collapsing. While the US decelerates, private investment remains strong and Asia shows resilience. This can drive more investor flows into emerging markets. - Theme 3: Disinflation Supports Policy Shift

Services inflation is easing, setting the stage for a more flexible Fed. While rate cuts may not be immediate, a pivot could come sooner than expected. - Theme 4: Repositioning for Income & Resilience

Income is back in focus. We favour high-quality bonds, Singapore REITs, and private credit, areas offering attractive yields and stability in a lower-rate environment.

Let’s dive into our detailed 2H 2025 market outlook and explore the key macro drivers and asset class convictions shaping the investment landscape.

Table of Contents:

- H1 2025 Review: Non-US Assets Led the Way

- Global Growth – Softening in H2, but Avoiding a Recession

- Cooling Services Inflation Signals Lower Stagflation Risk

- Fed Policy Outlook: Caution Now, Flexibility Later

- Asset Class Convictions in H2 2025

- Charts That Caught Our Eye

- Conclusion: Positioning for a New Market Cycle

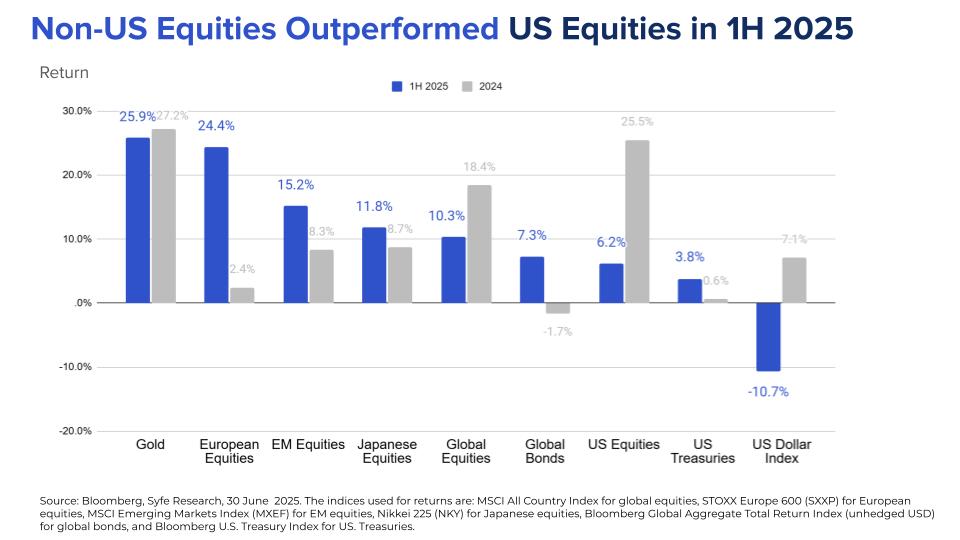

H1 2025 Review: Non-US Assets Led the Way

The first half of 2025 marked a significant shift in global markets. After years of US dominance, international assets outperformed US assets by a notable margin. European equities and emerging market(EM) equities delivered strong returns of 24.4% and 15.2% respectively (in USD terms), compared to just 6.2% for US equities. A key driver was the sharp decline in the US dollar, which provided a meaningful tailwind for risk assets abroad.

Meanwhile, US equities faced challenges, struggling to gain traction amid relatively expensive valuations and rising concerns over tariffs and policy uncertainty. The US fixed income market followed a similar trend. The US 10-year Treasury yields remained range-bound, as investors are closely watching the sustainability of US fiscal policy before making their next move. Gold, benefited from a weaker USD and strong demand for safe-haven assets, continued to deliver strong returns.

In summary, H1 2025 demonstrated the importance of global diversification, as international markets showed resilience despite headwinds. Looking ahead to H2 2025, the key question is whether this leadership shift will continue or if US markets will regain momentum. We remain cautiously optimistic, with a clear focus on diversification as a strategic advantage.

Global Growth – Softening in H2, but Avoiding a Recession

Soft Spots Emerging in H1 2025

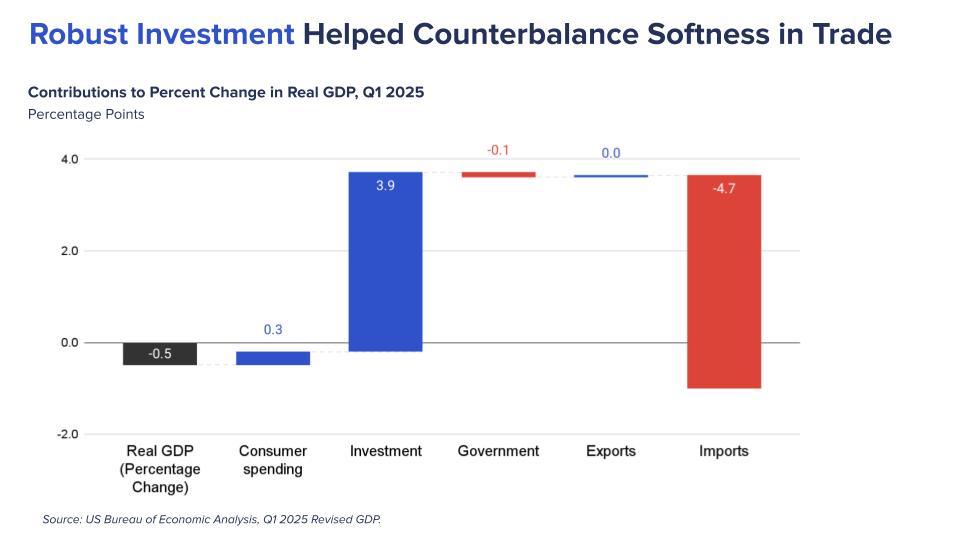

The first half of 2025 painted a mixed picture for the US economy. On the surface, the -0.5% contraction in Q1 GDP seemed worrying. But a closer look reveals that the weakness was largely driven by a surge in imports, as businesses rushed to stock up ahead of anticipated tariffs. Stripping that out, underlying activity looked more resilient, particularly private investment, which stood out as a bright spot by contributing a solid 3.9 percentage points to GDP growth.

That said, there were clear signs that the economy is slowing down. Consumer spending fell by 0.1% in May, the second drop this year, driven by a 0.8% plunge in goods spending as higher prices and uncertainty began to weigh on household demand.

Labour market momentum also softened. In 2024, private-sector hiring averaged a healthy 140,000 new jobs per month, according to ADP. But that pace slowed sharply in Q2 2025, with hiring dropping to just 60,000 in April and 37,000 in May. The sharp deceleration likely reflects growing caution among employers as they navigate elevated tariffs and shifting policy signals.

What to Watch in H2 2025: Tariffs, Tax Cuts & Tech

As we enter the second half of 2025, global growth will be shaped by three key factors: trade tariffs, tax cuts, and tech investments.

Trade Tariffs: Staying Elevated

Global growth is cooling in H2 2025, with trade tariffs remaining a key drag. Despite ongoing negotiations, tariffs are expected to stay around the mid-10% range as the Trump administration uses them to raise revenue and boost domestic manufacturing. As a result, global GDP growth is forecast to slow to 2.8% in 2025 from 3.2% in 2024, with US growth falling to 1.8% in 2025 from 2.8% in 2024.

Tax Cuts: One Big Beautiful Bill (OBBBA)

The OBBBA aims to extend tax cuts and promote deregulation to support long-term growth. While most effects will materialise in 2026, its expected passage by July could boost business confidence and near-term investment.

Tech Investments: AI as a Growth Driver

AI continues to be a bright spot. Strong investment in tech, especially AI, has helped offset some of the slowdown. This trend, which fuelled upside surprises in 2023 and 2024, remains a key growth driver heading into H2 2025.

In summary, while we expect a short-term slowdown in growth due to the impact of ongoing tariffs, the overall economic outlook remains supported by tax cuts, deregulation, and strong tech investments, particularly in AI. The risk of a severe downturn remains low.

Cooling Services Inflation Signals Lower Stagflation Risk

While stagflation remains a popular narrative in markets, we believe the risk is lower than widely assumed.

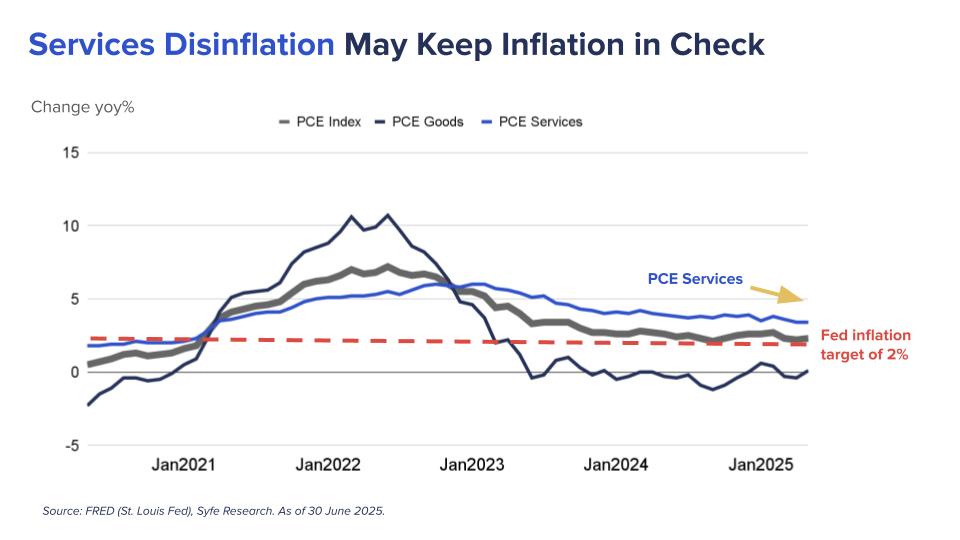

The May Personal Consumption Expenditures (PCE) report, the first to reflect the impact of the new tariffs, showed core PCE inflation rising 2.7% year-on-year, slightly above expectations and broadly consistent with the Fed’s path toward disinflation.

There were signs that tariffs are starting to filter through into prices. Durable goods inflation remained firm, especially in categories like household appliances and electronics. But the broader impact was contained.

More importantly, PCE services inflation continued to ease. In May, the PCE Services rose 3.4% year-on-year, near its lowest level since early 2023. A key driver of this slowdown was softer housing-related inflation, which accounts for a large portion of the PCE basket.

If this disinflation trend in service persists, it could help offset upward pressure from goods inflation, keeping core PCE on a stable path into the second half of 2025.

Fed Policy Outlook: Caution Now, Flexibility Later

We anticipate that the Fed will approach rate cuts cautiously in the second half of 2025, but there’s a growing likelihood of faster cuts in 2026. We are beginning to observe signs of weakness in consumer spending and the labor market. If inflation remains contained as anticipated, the Fed may accelerate its pivot toward rate cuts in 2026, similar to the shift in focus from inflation to growth seen in late 2024.

Another critical factor to watch is Chair Powell’s term and the potential succession process. As Chair Powell’s term nears its end in May 2026, President Trump may try to influence the process by nominating a “shadow” successor to weaken Powell’s authority in advance. Although this would not have formal legal power, it could introduce political uncertainty and raise concerns about the Fed’s independence, adding complexity to the policy landscape.

We expect the Fed to maintain its easing trajectory, but the pace could quicken in response to deepening economic weakness and political noise around the succession process.

Asset Class Convictions in H2 2025

| Currency | The USD is expected to gradually weaken in H2 2025 due to narrowing rate differentials and policy preference for a softer dollar. |

| Equities | For US equities, we prefer sectors that stand to benefit from both Trump administration policies and the ongoing rise of AI – namely Financials, Industrials, and Tech. At the same time, a weaker dollar opens up new opportunities outside the US, and we remain positive on EM equities. Among EM countries, we prefer economies with large and resilient domestic markets. As such, we are constructive on India, with its strong structural growth, and on China, where attractive valuations and policy support offer a potential tailwind. |

| Bonds | With short-term rates likely falling and long-term yields anchored by fiscal deficits, we favour the belly of the curve (3-7 years). Investment-grade bonds remain attractive, providing a defensive cushion against increasing growth risks.For non-US investors, currency hedging is also critical, and an active strategy allows for more responsive positioning across rates, credit, and FX. |

| Commodities | We maintain a positive view on gold within commodities, driven by a softer dollar and sustained demand from central banks. |

| Real Estate | Singapore REITs offer attractive yields. While local bond yields have fallen, S-REIT prices haven’t fully adjusted. High-quality names still yield around 6% p.a in SGD, and distributions are tax-exempt for both local and foreign investors. |

| Private Markets | Private markets have historically offered strong, less correlated returns compared to public markets.While positive on private credit, we emphasise selectivity. Focus on high-quality, defensive segments like first-lien loans and well-structured senior debt. |

Charts That Caught Our Eye

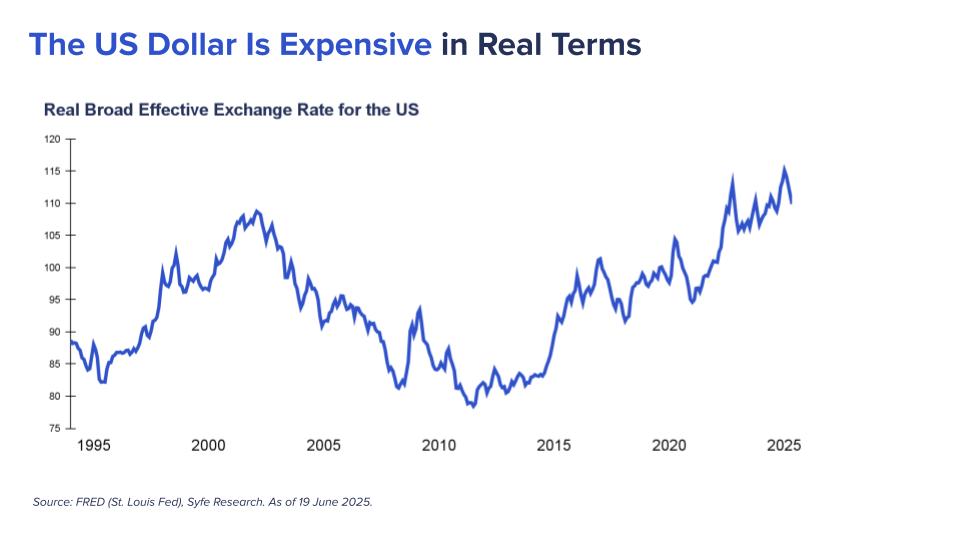

Chart 1: Despite the recent pullback, the US dollar remains relatively expensive.

Key takeaways:

- Pullback does not equal collapse. Despite recent weakness, the US dollar remains expensive on a trade-weighted, real basis. Concerns about the dollar losing its reserve currency status appear overstated, given the absence of a credible alternative.

- Drivers for gradual weakness are emerging. That said, there are reasons to expect a modest decline. Narrowing interest rate differentials, as the Fed cuts while other central banks hold steady, may erode the USD’s yield advantage.

- Policy tilt favours weakness. US policymakers have expressed a preference for a softer dollar to support exports and manufacturing. This could reinforce a gradual depreciation trend.

- Our view: modest decline ahead. Overall, we expect the dollar to decline moderately in H2 2025. Investors should be mindful of currency exposure, especially in globally diversified portfolios.

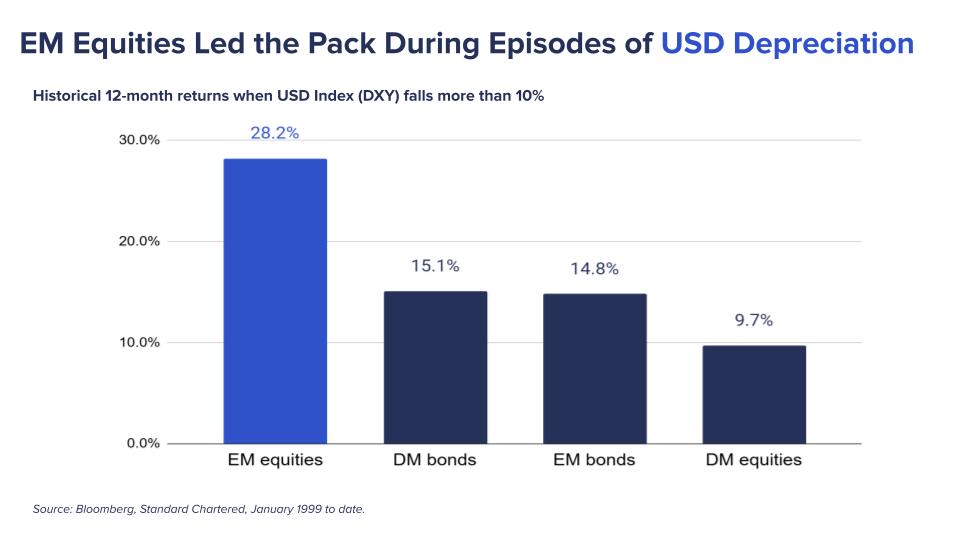

Chart 2: EM equities tend to outperform during periods of US dollar weakness.

Key takeaways:

- EM strength during dollar weakness. EM equities tend to outperform developed markets when the US dollar weakens, benefiting from currency tailwinds and renewed capital flows.

- Rotation trend gaining traction. The recent shift into EM equities marks a reversal of the past few years and may have further room to run.

- Diversification is key. A weakening dollar reinforces the case for broader global equity exposure, especially adding EM, to enhance diversification at this stage of the cycle.

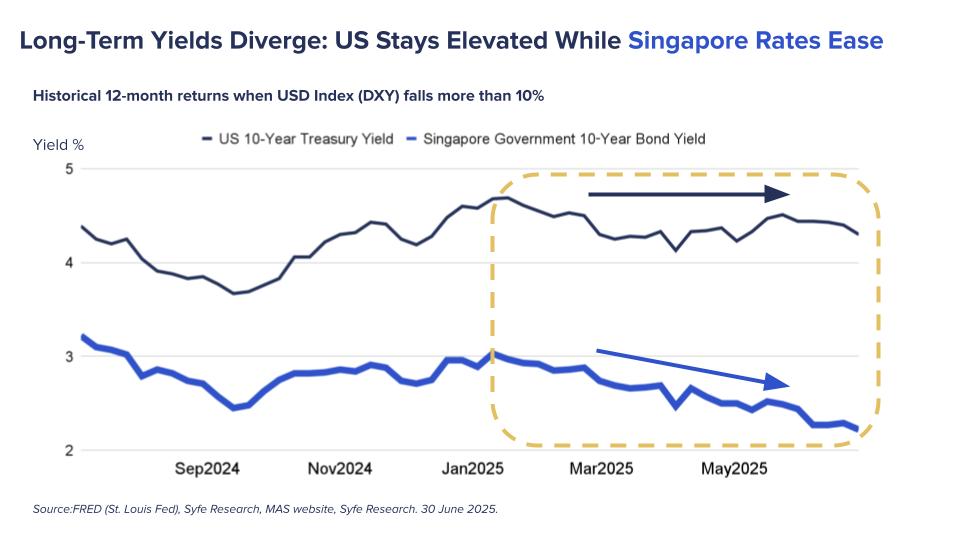

Chart 3: Easing Singapore interest rates could provide support for S-REITs

Key takeaways:

- Diverging Rate Paths. Singapore interest rates typically track US rates closely. However, we’ve started to see a divergence this year, with local rates easing more visibly.

- Positive Momentum for S-REITs. Lower domestic rates can reduce financing costs for REITs—a tailwind that may not be fully priced in yet. Recent earnings already show early signs of this improvement.

- Attractive Yields for Income Investors. With blue chip S-REITs now offering dividend yields of nearly 6.0% p.a., we see compelling value, especially for income-focused investors seeking stable cash flows.

Conclusion: Positioning for a New Market Cycle

The first half of 2025 marked a clear shift in market leadership: from US dominance to broader global strength. As we head into H2, portfolio positioning must adapt to this evolving landscape. We see greater need for diversification, selective risk-taking, and a renewed focus on income. A softer USD, easing inflation, and targeted fiscal support are unlocking opportunities across geographies and asset classes. In this environment, nimble, globally diversified, and income-focused portfolios are best positioned to capture the opportunities ahead.

You must be logged in to post a comment.