Real Estate Investment Trusts (REITs) are a popular passive income option for many Singaporeans. In our land-scarce nation, we all know real estate prices trend upwards over time. REITs provide investors of all stripes a great way to add this exposure to their portfolios while offering relatively high dividend yields.

Table of Content

- What About Physical Properties?

- Why REITs Are A Hassle-Free Alternative

- What A REIT Portfolio Is And What It Is Not

- Singapore REITs, US REITs, And SGX APAC REIT ETFs

- How To Build A Diversified REIT Portfolio Singapore Investors Can Maintain

- A Simple Starter Portfolio Framework (Illustrative)

- How To Start Investing In REITs

- Quick Takeaways

- Syfe REIT+: In collaboration with SGX

- Frequently Asked Questions (FAQs)

- Resources & Further Reading

What About Physical Properties?

While owning private property may be a common aspiration for many Singaporeans, there is a lot more to being a landlord than just collecting rent.

Firstly, you need to have enough money upfront to pay the down payment on your property. For a condo unit that’s meant to be your second property, your minimum cash down payment is a whopping 25% (depending on loan-to-value limits, existing loans, and prevailing rules).

Moreover, the rental income you earn is not exactly passive. After finding the right tenants, it takes time, money, and effort to manage and maintain your property for the long term.

Rental income from your property is subject to income tax as well. That’s on top of the property tax you have to pay, which is calculated based on the Annual Value of your property.

Why REITs Are A Hassle-Free Alternative

Compared with physical properties, REITs provide all the benefits of property ownership without the headache and hassle.

A Real Estate Investment Trust (REIT) is a listed vehicle that owns income-generating real estate and distributes income to investors. You don’t need a large capital to start investing in REITs. You also get to collect passive income without doing much at all since REITs are professionally managed. The REIT manager and property manager will work together to implement asset enhancement initiatives and optimise rental yields.

Last but not least, dividends paid out by REITs are tax-free. If you receive $10,000 as dividends from your REITs portfolio, you get to keep every cent.

What A REIT Portfolio Is And What It Is Not

REIT portfolios can include properties such as retail, offices, industrials, and healthcare properties. A REIT portfolio Singapore investors build differs from owning one or two REITs in one key way – It is designed as a repeatable income system, with clear diversification and risk controls.

What a REIT portfolio is

A REIT portfolio Singapore strategy typically means you are intentionally managing:

- Income sustainability (how resilient distributions are across cycles)

- Diversification (sector, tenant, and—where relevant—currency and geographic exposure)

- Financing resilience (leverage, interest coverage, and refinancing concentration)

- Reinvestment rules (income mode vs compounding mode)

- Behaviour risk (how you respond during drawdowns)

A helpful way to think about this is: A REIT portfolio is not just about “which REITs”, but also about how you size, diversify, and maintain the allocation so it remains investable in different rate and property cycles.

What a REIT portfolio is not

A REIT portfolio Singapore strategy is not:

- An emergency fund replacement (unit prices can be volatile)

- A guaranteed-income product (distributions can be reduced)

- A “set-and-forget forever” allocation (periodic checks matter)

Singapore REITs, US REITs, And SGX APAC REIT ETFs

For Singaporean investors building a REIT portfolio plan, the practical “global” question is usually about implementation: how do you diversify beyond one market without turning it into a complex overseas portfolio?

Within the scope of this guide, two controlled options are most common:

- US REITs (for those comfortable with USD exposure), and/or

- SGX-listed REIT ETFs that provide Asia-Pacific exposure through a single SGX-listed instrument

Option A: Singapore-listed REITs (S-REITs)

Singapore-listed REITs are commonly grouped into sectors such as office, retail, industrial/logistics, healthcare, hospitality, data centre, and diversified. Many S-REITs also hold properties outside Singapore, which can diversify income sources while still keeping the investment in an SGX-listed structure.

If you want a detailed S-REIT deep dive, you can read our full guide here: How to Invest in Singapore REITs: Everything You Need to Know

Option B: US REITs (USD exposure)

US REITs can provide broader sector exposure (including more specialised REIT segments). One structural feature is worth noting for portfolio planning: to qualify as a REIT in the US, the REIT must distribute at least 90% of taxable income.

What this can mean in practice:

- US REITs can add diversification and sector breadth.

- Income is typically USD-linked, and SGD returns will reflect both REIT performance and USD/SGD movement.

A controlled approach is to size US REIT exposure modestly unless you explicitly want USD income.

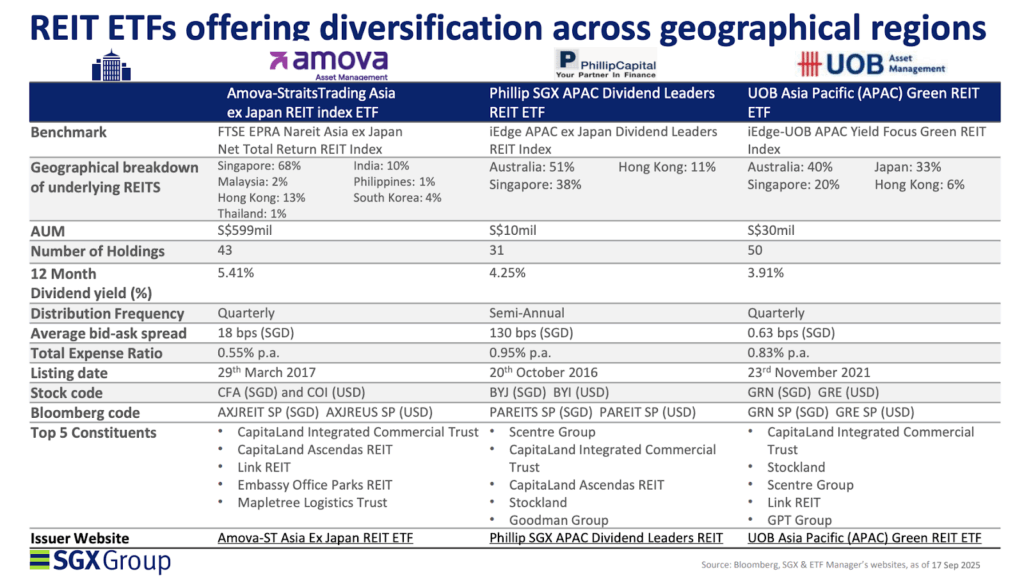

Option C: SGX-listed APAC REIT ETFs (Broader regional exposure, one ticket)

For investors who want geographic diversification without managing multiple overseas positions, SGX-listed REIT ETFs can be a practical “single instrument” solution.

Three examples are:

- Amova-StraitsTrading Asia ex Japan REIT Index ETF: Provides exposure to a basket of Asia-Pacific REITs excluding Japan, tracking the FTSE EPRA Nareit Asia ex Japan Net Total Return Index.

- Phillip SGX APAC Dividend Leaders REIT ETF: Tracks the iEdge APAC ex-Japan Dividend Leaders REIT Index.

- UOB APAC Green REIT ETF: Linked to the iEdge-UOB APAC Yield Focus Green REIT Index concept.

Portfolio insight: An APAC REIT ETF can support a diversified REIT portfolio approach by spreading exposure across multiple REIT markets in the region through one SGX-listed holding. The trade-off is that you accept the index composition and weights.

How To Build A Diversified REIT Portfolio Singapore Investors Can Maintain

A diversified REIT portfolio strategy should be designed to be maintainable, not only theoretically optimal.

Step 1: Define the role of REITs in your plan

Be explicit about which outcome you prioritise:

- Income-first: distributions are meant to be spent

- Income + compounding: most distributions are reinvested

- Diversification: REITs complement equities and bonds, not replace them

This one decision determines allocation size, risk tolerance, and how defensive your REIT sleeve should be.

Step 2: Set a realistic REIT allocation range

There is no universal “best” REIT allocation. A practical range is one you can hold through volatility:

- Conservative investors: 5%–15% in REITs

- Moderate investors: 10%–25%

- Income-focused investors: 15%–35% (with stronger diversification and buffers)

Portfolio insight: If you increase REIT allocation to raise income, also strengthen guardrails, especially concentration limits and a defined review cadence.

Step 3: Diversify across sectors (Avoid “false diversification”)

Sector diversification reduces the risk that one property type dominates outcomes. A simple rule for individual REIT selection:

- Aim for 4–6 sector exposures

- Avoid clustering in sectors driven by the same macro factor (for example, multiple holdings that are effectively the same interest-rate or refinancing bet)

If you are investing through a broad REIT ETF, sector diversification is often handled by the index—your job becomes deciding how much REIT exposure you want, not micro-selecting each sector.

Step 4: Add geographic diversification through controlled channels

Within this guide’s scope, two controlled approaches are commonly used:

- A modest US REIT sleeve (if you want USD-linked exposure), and/or

- A SGX APAC REIT ETF (for broader regional exposure via a single SGX-listed product)

A practical structure for many investors:

- 60%–80% of the REIT sleeve in Singapore-listed REIT exposure

- 20%–40% of the REIT sleeve in either US REITs or an SGX-listed APAC REIT ETF (based on currency preference and simplicity needs)

Step 5: Control concentration at the holding level

Concentration is often the hidden reason a “best REIT portfolio” plan disappoints.

Portfolio guardrails that meaningfully reduce risk:

- No single REIT > 15%–20% of your REIT sleeve

- No single sector > 35%–40% of your REIT sleeve (unless deliberate)

- If using US REITs: keep sizing modest unless you specifically want USD income

Step 6: Use a lightweight review cadence

A REIT portfolio plan does not require daily monitoring, but it does benefit from periodic checks:

- Quarterly: occupancy trends, refinancing commentary, major leasing updates

- Annually: rebalance to target weights, reassess concentration

- Event-driven: review after major acquisitions, divestments, or equity fundraising

A Simple Starter Portfolio Framework (Illustrative)

Use the framework below as a practical starting point. The right allocation depends on your risk tolerance, time horizon, and financial needs, so treat the ranges as flexible.

Starter portfolio framework: Growth core + REIT income sleeve

Objective: Keep a diversified growth core, while adding REITs as a dedicated income and real-asset sleeve.

- 10%–20%: REIT sleeve (diversified; can include Singapore-listed REIT exposure and/or a measured allocation to US REITs or an SGX-listed APAC REIT ETF)

- 60%–80%: Diversified equities / broad funds (long-term growth engine)

- 10%–30%: Bonds / cash management (stability buffer and liquidity)

How to adjust over time

As priorities shift, you can adjust without redesigning the portfolio:

- If you want more stable income, gradually increase the bonds/cash buffer and keep the REIT sleeve quality-focused.

- If you want higher long-term growth, tilt more toward equities and keep REITs as a smaller complement.

If you want more geographic diversification, add it in a controlled way (either a modest US REIT sleeve or a single SGX-listed APAC REIT ETF), while keeping concentration limits intact.

How To Start Investing In REITs

FoTo start investing in REITs, there are three main ways to do so in Singapore.

- Buy individual REITs through your broker

- Invest in REIT exchange traded funds (ETFs)

- Invest in a managed REIT portfolio via Syfe REIT+.

The first option provides you more control over sector exposure and quality. However, it involves paying expensive brokerage fees (up to $25 minimum commission, varying by broker) each time you make a buy or sell transaction. If you want to build a diversified REIT portfolio, you may be better off choosing the second or third option.

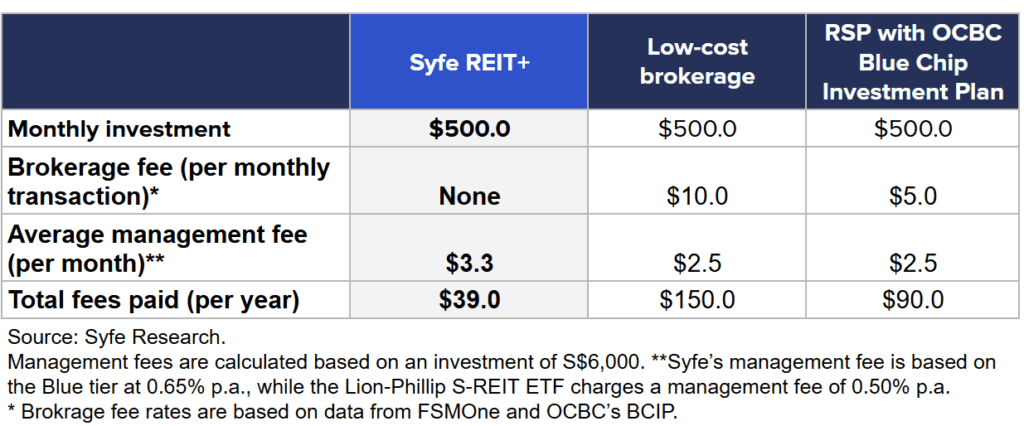

Between REIT ETFs and Syfe REIT+, many investors find that REIT+ offers better portfolio efficiency at a lower cost. With REIT+, your funds are used to purchase the 20 underlying REITs held by the portfolio. With a REIT ETF, your funds are used to purchase that particular ETF, which itself is a product that is traded on the SGX.

Cost-wise, here’s an example of how much it will cost to invest $500 each month in Syfe REIT+ as compared to the Lion-Phillip S-REIT ETF, purchased either through a broker or a Regular Savings Plan (RSP).

If you’re looking for an efficient yet low-cost REIT portfolio, you’ll likely find that Syfe REIT+ stacks up better than REIT ETFs.

Quick Takeaways

- A REIT portfolio Singapore strategy works best as a system: diversification, sizing rules, and maintenance discipline, not just high yields.

- For geographic diversification, a controlled approach is typically either a modest US REIT sleeve (USD exposure) or an SGX-listed APAC REIT ETF (one-ticket regional basket).

- A diversified REIT portfolio approach often starts with 4–6 sector exposures and clear concentration caps (especially if selecting individual REITs).

When comparing investment methods, consider not only fees but also diversification efficiency (how easily you can spread exposure across REITs).

Syfe REIT+: In Collaboration With SGX

Syfe REIT+ is the first portfolio built in collaboration with SGX to offer the iEdge S-REIT Leaders Index to retail investors. Since you cannot invest directly in an index, portfolios like REIT+ provide an indirect investment option.

With REIT+, you get the opportunity to invest in the 20 largest and most tradeable Singapore REITs like Ascendas REIT, Capitaland Integrated Commercial Trust and Mapletree Logistics Trust and more.

Additionally, REIT+ allows you to build up your REIT holdings through regular contributions. Because there is no minimum investment amount and no brokerage fee for each transaction, you can choose to invest any amount you prefer, at any time you want.

REITs can be especially appealing for investors seeking stable dividend income and a unique diversifier to stocks and bonds. Ready to invest in them?

Frequently Asked Questions (FAQs)

1) How many holdings do I need for a diversified REIT portfolio?

If you are selecting individual REITs, 5–8 holdings is often a practical range to diversify across sectors without becoming difficult to monitor. If you prefer simplicity, a REIT ETF can provide broad exposure through a single holding.

2) Should I reinvest my REIT distributions or take them as cash?

It depends on your goal. If you are building wealth over time, reinvesting distributions can help compound returns and grow your REIT position steadily. If your priority is monthly or quarterly cashflow, you may prefer to take distributions as income—but it is usually still sensible to keep some flexibility (for example, reinvest part of it, or retain a small buffer) so you are not forced to sell units during market downturns.

3) Are REIT distributions tax-free in Singapore?

It depends on the type of distribution and the type of investor. Some S-REIT distributions can be made gross to individual investors, but distributions are not universally “tax-free” in all cases and can include taxable components depending on circumstances. A practical rule is to rely on the tax breakdown shown in official statements and the applicable IRAS guidance.

4) How can I add geographic diversification without buying many overseas REITs?

Two controlled approaches are common: a modest US REIT sleeve (if you want USD-linked exposure), or a single SGX-listed APAC REIT ETF that provides regional diversification through one SGX-listed holding.

5) How often should I review my REIT portfolio?

A practical cadence is quarterly checks (to spot material changes in leasing, refinancing, or capital actions) and an annual rebalance (to bring allocations back to your target ranges). Outside that, review as needed when there is a significant event—such as a large acquisition, divestment, or equity fundraising.

Resources & Further Reading

- REITs vs Rental Properties: Which Is Better?

- How to Invest in Singapore REITs: Everything You Need to Know

- Is It Time to Shift from Singapore Banks to S-REITs?

- Syfe REIT+ vs REIT ETFs: What’s The Difference?

- What’s Driving the Growth in Singapore Retail REITs in 2025

- Singapore Office REITs: Why Prime Office Assets Remain a Compelling Investment in 2025

- Singapore Industrial REITs Outlook 2025: Market Trends, Performance, and What Investors Should Know

- Why Healthcare S-REITs Are a Hidden Gem for Defensive Investors

You must be logged in to post a comment.