Financial markets can be complex. Investors face an influx of news and fluctuating prices every day, making it difficult to sift through information and stay unemotional to make sound investment decisions.

If you’re just starting out with investing and are unsure about how the market is likely to move, the investment strategy known as dollar-cost averaging (DCA) can help you begin your investment journey and build wealth over time.

What Is Dollar-Cost Averaging?

Dollar-cost averaging is an investment strategy that helps you cushion the impact of market fluctuations through regular investments, regardless of market conditions.

By consistently investing a fixed sum of money over a period of time, you end up buying more shares when prices are low and fewer shares when prices are high.

Over the long term, the cost of all your investments purchased are averaged out. The benefits of both averaged returns and compounded growth can be achieved over longer periods. This mitigates the impact of short-term market fluctuations on your portfolio and eliminates some of the risky guesswork involved in trying to time the market.

How Does Dollar-Cost Averaging Work?

Two types of dollar-cost averaging exist, but both cater to the same strategy of consistent investment.

- Automatic Investment Plan – Setting up an automatic contribution each month into your investment fund. This would help to develop the habit of saving and investing regularly, eliminate the manual labour of maximising returns and grow your wealth over time.

- Lump Sum – When investors have a huge sum of money, such as from an inheritance or bonuses, the amount is divided and invested equally over a period of time instead of all at once.

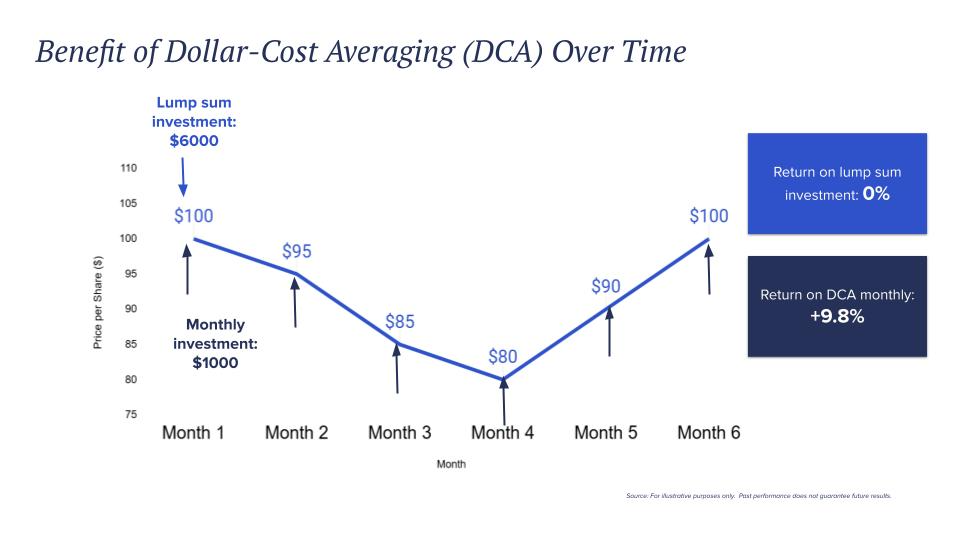

Let’s look at an example using dollar-cost averaging:

An investor has $2,000 to invest in Stock A. He plans to make five monthly payments of $400 each, buying shares at both highs and lows. He will buy some shares at $10 per share and some at $5 per share. Over the course of five months, the average cost would be $7.7 per share.

However, if he had invested the entire lump sum at the beginning, the average cost would be $10 per share.

By investing regularly, market timing becomes less important, as the cost of all your investments is averaged out.

Why Dollar-Cost Averaging Makes Sense

- Overcome the fear of investing

Dollar-cost averaging strategy mitigates the fear of investing. Market volatility can be very daunting, especially when handling large amounts of cash. Dollar-cost averaging can alleviate worries and offer a better alternative than leaving the money in the bank.

- Minimise psychological biases

With dollar-cost averaging, you’re investing consistently regardless of market conditions, emotions have to be removed from the equation. This allows you to be less susceptible to the investing biases or temporary bullish periods.

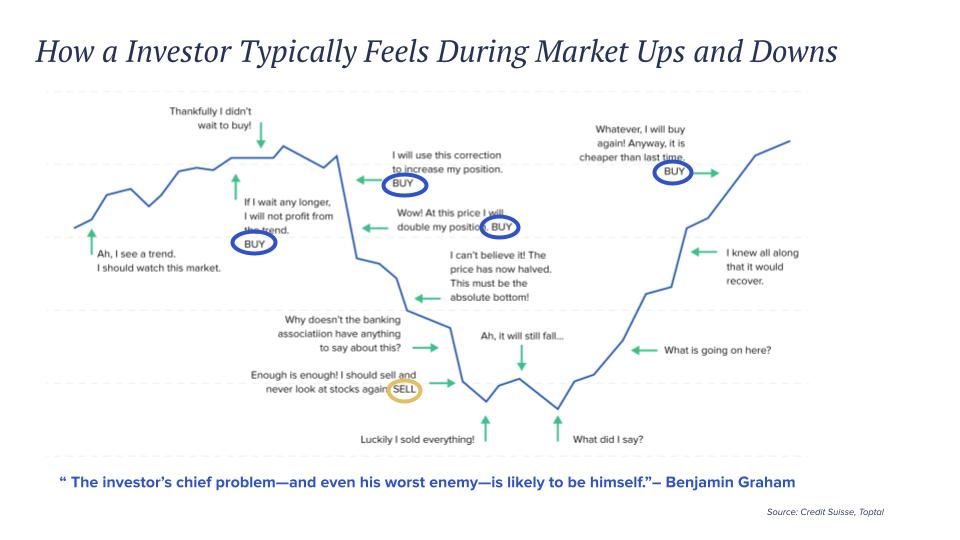

For instance, most people prefer avoiding losses more than they like winning—a behaviour formally known as loss aversion. When the market plummets, some investors may panic and sell their investments at the market bottom.

This is especially true if these investors had allocated a lump sum into the market. If you’re dollar-cost averaging, you’ll instead be purchasing your investments at an attractively low price, recognising that market downturns are more of an opportunity than a threat.

- Avoid timing the market wrongly

The risk of mistiming the market can also be avoided with dollar-cost averaging. Market timing involves entering and exiting investment positions based on human and technical analysis of the market.

While timing the market can result in above-average returns if executed correctly, it can also lead to significant losses. Over the long run, consistent market prediction is nearly impossible and mistiming would be inevitable.

Thus, instead of digging your own grave with the possibilities of mistiming, dollar-cost averaging will provide you with investment opportunities of lower risks.

Potential Drawbacks To Note

Despite many benefits, there are still some potential drawbacks for dollar-cost averaging strategy.

- Missed opportunity

One scenario where dollar-cost averaging may not be ideal is when markets are in a strong uptrend. Dollar-cost averaging into an investment that continues to rise each month will prevent you from maximising your gains. If you have the means, this is one situation where a lump sum investment would be better.

However, if you remain nervous about investing all your money at once, dollar-cost averaging is still a reliable strategy to get some money in the markets and take advantage of the market growth.

- Dollar-cost averaging into bad investments

Dollar-cost averaging can be counterproductive if you invest in a stock without proper research. If you keep dollar-cost averaging into a poor investment, you may end up with large losses.

One way to mitigate this risk is to use broad-based exchange-traded funds or diversified portfolios instead of single stocks. Such investments tend to rise over time.

How To Start Dollar-Cost Averaging

You can easily start dollar-cost averaging by auto-investing with Syfe.

A simple and cost-effective way would be to dollar-cost average into Syfe’s Core or REIT+ portfolios. Our flagship Core Portfolios comprise various ETFs diversified across multiple asset classes, sectors and geographies, while our REIT+ portfolios offer pure exposure to Singapore REITs.

Our new auto-invest with eGIRO feature draws funds directly from your selected bank account so you won’t miss an investment. For automatic, consistent investing, auto-invest helps you stick to your dollar-cost averaging strategy.

Dollar-cost averaging is ultimately a logical, non-emotional approach to investing. It may seem boring, investing the same amount consistently every month, but it is this boredom that makes dollar-cost averaging such a successful investing strategy.

Ready to put dollar-cost averaging into action? Start auto-investing with eGIRO today.

Read More:

How and Where to Invest Your First $100K in Singapore – Your Step-by-Step Guide

The Best Passive Income Investments in Singapore

You must be logged in to post a comment.