Thought Of The Week

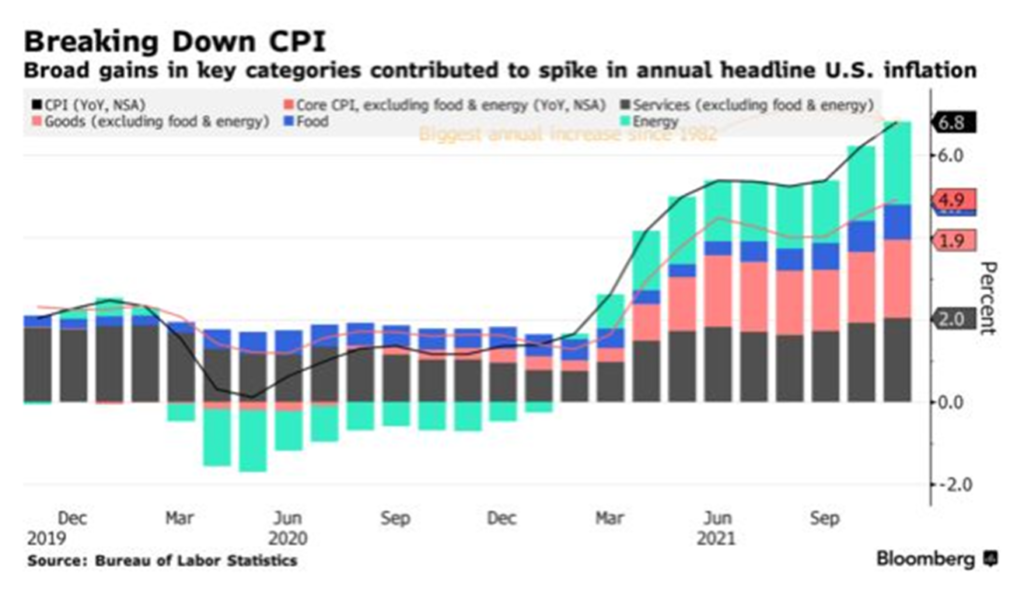

U.S CPI

The consumer price index climbed 6.8% year-over-year in November, broadly in line with market expectations this time instead of surprising to the upside in prior months. Price increases have since broadened out to other categories including gasoline, shelter and food from the initial concentration in economy’s reopening categories. With persistent supply chain challenges and labour constraints keeping prices high in the near term, the path of inflation will depend on corporate pricing power. If corporates do not have pricing power, high inflation is unlikely to last.

U.S. stocks rose to a record this week as the inflation data has been priced in and reinforced market expectations that Federal Reserve will not further accelerate its pace of tapering and interest rate increases. Yield on the U.S. 10-year Treasury fell to 1.49% as traders trimmed bets on the pace of Fed tightening. Investors are bracing for the last Federal Reserve meeting of the year on 14-15 Dec for clues regarding its positioning into 2022 after an upsurge of volatility in recent weeks.

Evergrande Defaults

After months of struggling to make payments and investors believing that it is too big to fail, China Evergrande Group has officially defaulted. While Evergrande bondholders face deep haircuts, there were few signs of financial contagion and market panic as the Chinese government has been making efforts to cushion the blow. Some of the measures include cutting reserve requirement, appointing officials to oversee Evergrande’s restructuring process and managing yuan strength. By doing so, more money can be released into the economy which could help to revive a softening property market that saw home prices fall for the first time in six years in September. Commercial banks are also ordered to hold more of their foreign currencies in reserve to curb yuan’s gains which have been largely fuelled by strong exports and foreign direct investments.

Although China’s reluctance to bail out the developer sends a clear signal it will not tolerate massive debt build-ups which may threaten financial stability, they have acted to limit the fallout from Evergrande’s crisis and ringfence the risks.

Chart Of The Week

Important Information and Disclosure

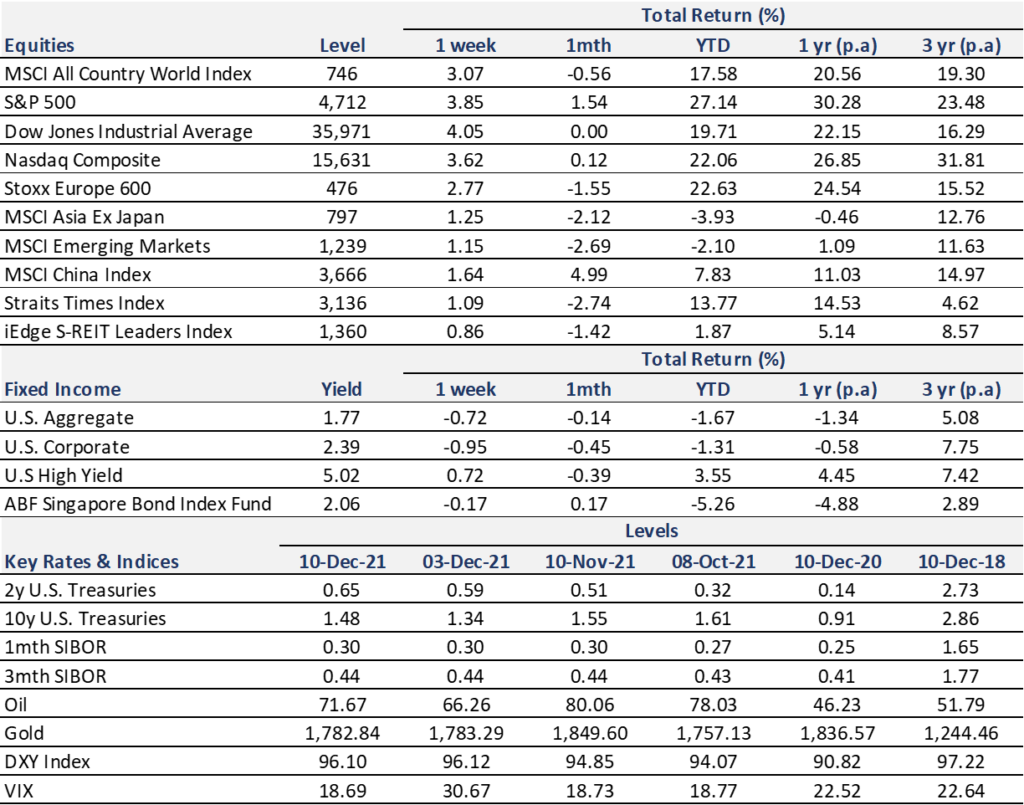

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.