Thought Of The Week

U.S Jobless Claims, ECB Meeting, Flat Markets

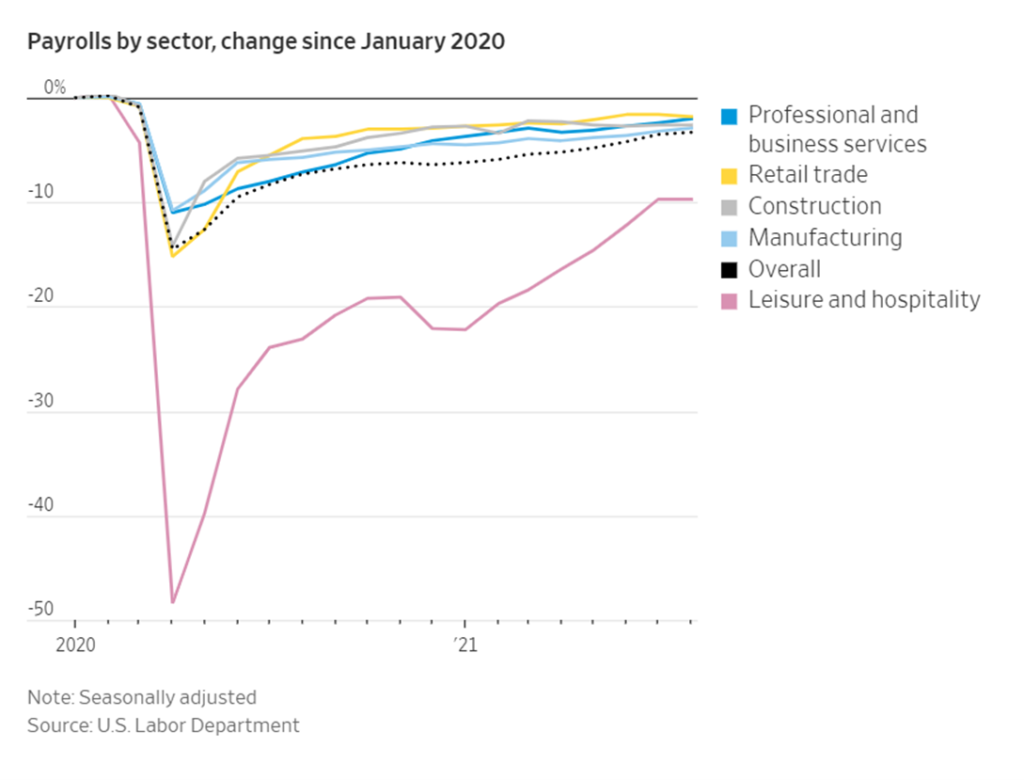

Initial unemployment claims, a proxy for layoffs, moved lower to 310,000 from 345,000 the prior week as the labour market continues toward a full recovery. Claims have trended lower since mid-July, a sign that employers are holding on to workers despite a rise in the Delta variant cases and weaker-than-expected August job report released last Friday. 235,000 jobs were added last month, falling far short of economists’ estimates for 720,000 with gains coming from leisure and hospitality while retailers cut jobs. With the aid programs ending on 6 September and people returning to workforce, it is better to grasp the real situation of the job market in November (Oct NFP) and December (Nov NFP).

Meanwhile, ECB President Christine Lagarde said that it would conduct bond purchases under its emergency program at a “moderately lower pace” over the next three months but added that did not herald a winding down in stimulus with the delta strain still posing risks. Investors took the ECB’s move in stride with European stocks making modest gains after the monetary policy decision. The eurozone economy has expanded strongly in recent months, driven by higher household spending as social restrictions aimed at containing the virus were rolled back.

Markets are relatively neutral this week as investors continue to evaluate the spread of the coronavirus and the increasingly adversarial relationship between President Joe Biden and China’s Xi Jinping.

Global Supply Chain Imbalance

Supply chain disruption has been making headlines since the pandemic struck and rising Delta variant cases are adding fresh uncertainty. Although some products have seen reduced supply, global manufacturing output is near an all-time high. On the supply side, blockages caused by the pandemic are forcing businesses to invest in new production facilities while pent up consumer spending on goods instead of services is leading an extraordinary level of goods demand.

U.S consumer spending on durable goods (excluding cars) is about 25% above trend, resulting in a supply-demand imbalance rather than a supply crisis. However, global companies are rushing to spend new plants and machinery. According to Morgan Stanley, global investment will reach 121% of pre-recession levels by end of 2022 which will support long term growth as productivity improves. As savings are used up and people shift back to spending on services, it will be important to distinguish the investments that will benefit from supply chain diversification and automation from those that may not be as productive as it looks.

Chart Of The Week

Important Information and Disclosure

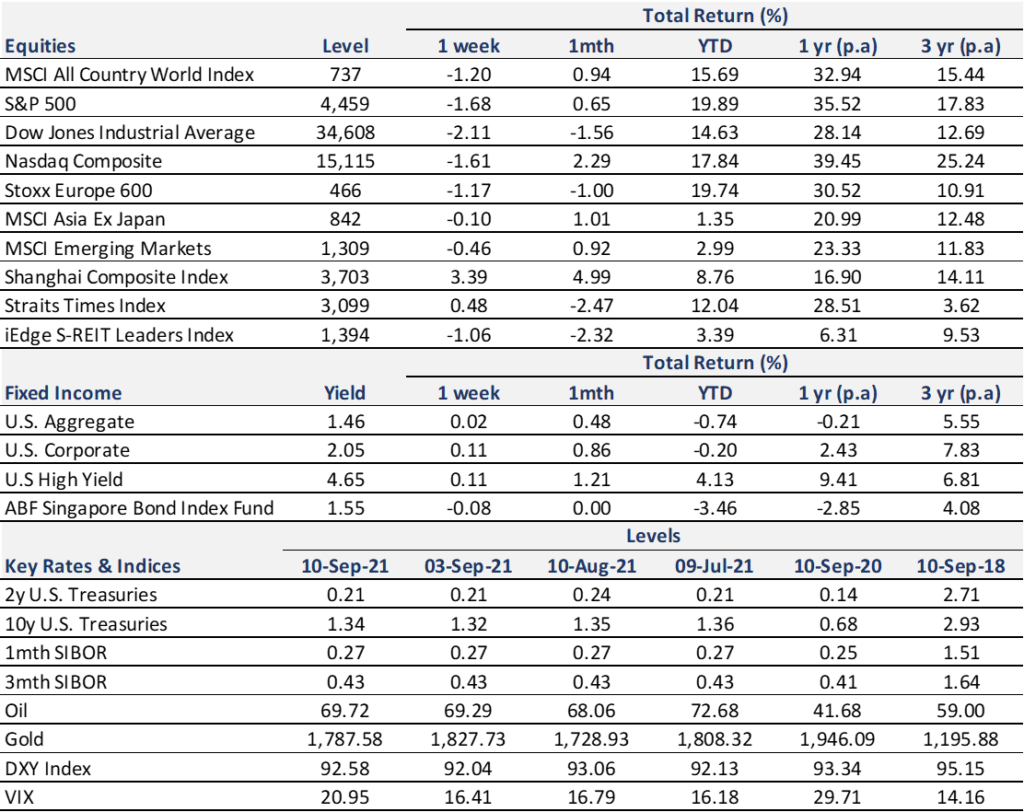

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.