The Week Ahead

- Europe CPI (Apr)

- FOMC Meeting Minutes

Thought Of The Week

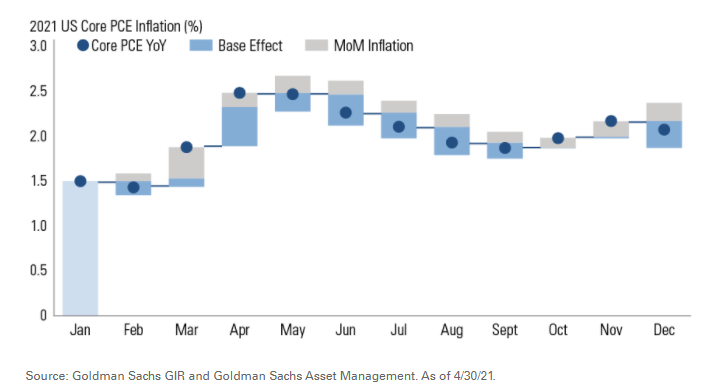

Inflation Angst and U.S Retail Sales

Financial markets tumbled the most in two months on Wednesday after the release of April’s Consumer Price Index (CPI) which saw inflation accelerating faster than expected. Excluding volatile food and energy prices, the core CPI rose 3% year-on-year compared to market estimate of 2.3%. Price surges have resulted as the U.S economy recover amid supply bottlenecks caused by shortages, shipping challenges and a soaring demand for commodities.

In addition, the higher headline CPI rate may also be distorted due to base effects since inflation was very low at this time last year. However, the stalling April retail sales data released on Friday provided some solace to investors who have become increasingly sensitive to inflation risks even though there is still pent-up capacity in many sectors. Concerns that policymakers will have to pull back their easy monetary stance and the massive barriers obstructing President Joe Biden’s ambitious $4 trillion package capped the volatile week. Gold climbed to its highest in more than three months while equities struggled due to inflationary fears.

Musk’s Change of Coins

An outspoken supporter of cryptocurrencies with cult-like following on social media, Tesla’s CEO Elon Musk holds immense sway with his market-moving tweets. This week, his antics sent cryptocurrencies on a wild ride again by implying that Tesla may be selling its $1.5 billion stake in Bitcoin. This comes after the announcement last week that it will be no longer be accepting Bitcoin for payments, citing environmental concerns about energy use to process transactions. The saga caused the token to shave $20,000 off the record set in April. Meanwhile, Musk sent Dogecoin skyrocketing after he claimed that it beats Bitcoin “hands down” and suggested that it could “become currency of Earth” even though he called it a “hustle” several days earlier.

Musk’s irreverent tweets has caused some volatility and negative wealth effect for holders. But more importantly, it is a good reminder that if one person can dramatically alter its value, perhaps the road to becoming a viable currency is still a long one. Afterall, one can only be considered as a currency if it fulfils the 3 criteria 1) Be a fixed unit of account 2) Function as a medium of exchange 3) Be a store of value.

Chart Of The Week

Important Information and Disclosure

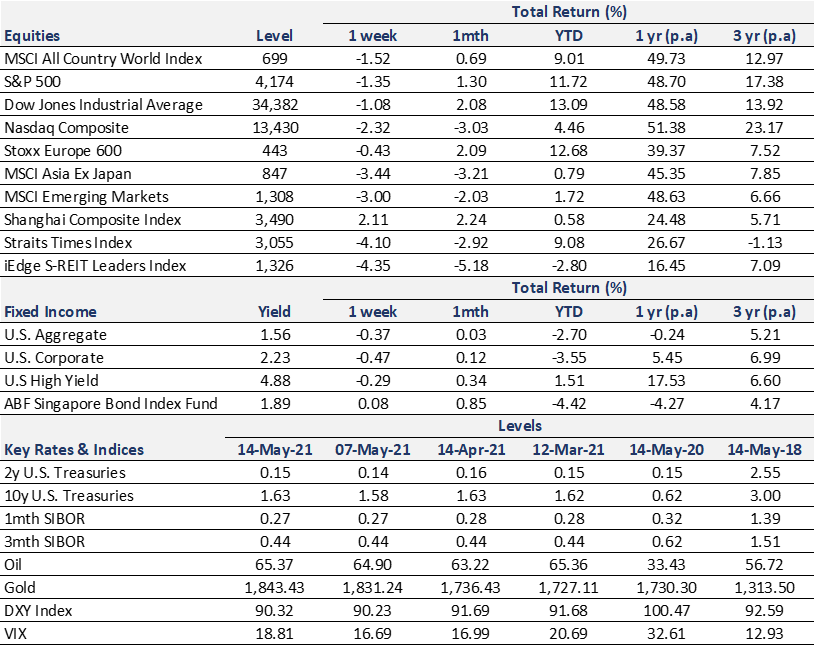

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.