Thought Of The Week

Fed Hawkishness, Higher GDP Forecasts

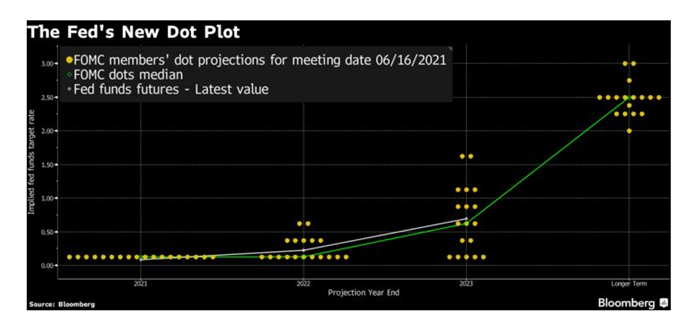

Markets were focused on the Federal Open Market Committee’s (FOMC) June Meeting this week. While no one was expecting a change in interest rates, it was interesting to look out for any changes in the dot plot which could signal a shift in the future inflation expectations. Afterall, many economic indicators have shown that the recovery has strengthened significantly from its last meeting due to the speed of vaccinations and strong policy support. The quarterly projections showed 7 out of 18 Fed officials favouring a hike in 2022 (vs 4 in March) and 13 favouring at least one hike by the end of 2023 (vs 7 in March). It was a hawkish surprise to markets as stocks declined after the two-day meeting concluded on Thursday.

The Fed officials also seemed to have considerable confidence in the economic recovery and signalled that they have started “talking-about-talking-about” joining Team Taper though it was not imminent. It raised its GDP growth forecast from 6.5% to 7% for 2021 and maintained its estimate at 3.3% for 2022. Markets continued to be surprised by the Fed on Friday after St. Louis Fed President, James Bullard, reiterated his hawkishness during a CNBC interview where he cited that interest rates would need to start rising next year because of how quickly the economy is growing. The S&P 500 fell 1.3% after his comments and closed the week 1.9 % lower. VIX index jumped to 20.70 while gold fell below $1,800 an ounce as dollar touched a two-month high.

Shining Spots Remain in Asia and China

Asia equities have lagged the global equity benchmark for the first half of the year as stronger USD and regulatory risks posed headwind to the region. For the past 15 months, the liquidity unleashed by the central banks abroad had found their way to the mainland which Chinese officials have repeatedly encouraged a correction to contain the asset bubbles. Such interventions have intensified in recent weeks which include curbing commodities exposure for state firms, forcing banks to hold more foreign currencies to rein in the surging yuan and censoring searches for crypto exchanges to crackdown on speculative bubbles.

However, bright spots are reappearing after the recent sell-off as valuations become more attractive compared to the developed markets. In addition, the rebound in USD is likely to be short-lived despite the hawkish Fed which would allow Asia and China to play some catch-up. While the rally is unlikely to be toppled, investors should expect continued bouts of volatility in the short-term and keep their focus on maintaining a well-diversified portfolio and avoid trying to time the market.

Chart Of The Week

Important Information and Disclosure

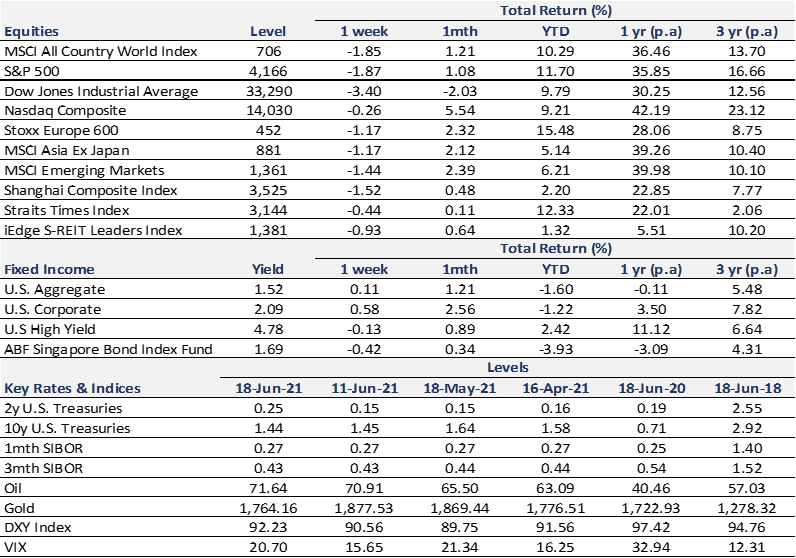

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.