Thought Of The Week

U.S Inflation Report, G7 Meeting

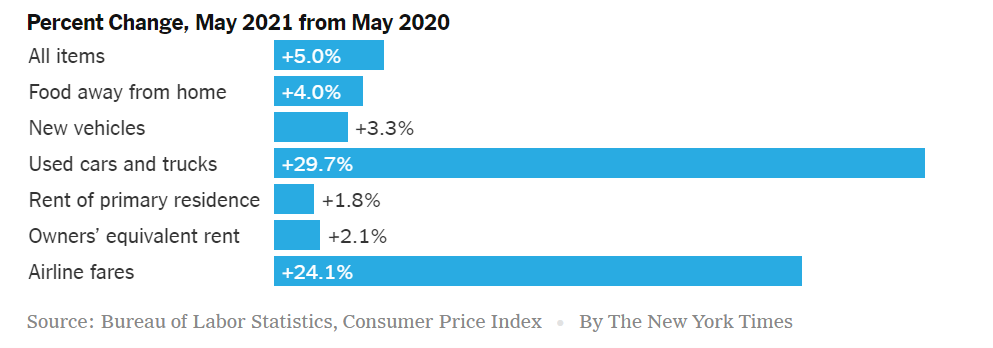

Rising inflationary pressures have curbed equities advance in the past weeks as markets debated over whether this is transitory, as economists and central bankers say, or something more lasting. This week, markets seem to trust the former despite a hotter-than-expected inflation report released on Thursday. The consumer price index climbed 0.6% MoM and was higher by 5% YoY. S&P 500 advanced to a fresh record on the news while 10-year Treasury slipped back below 1.5% (not a typical move from a market worried about inflation).

Perhaps markets found sufficient comfort that the gains were largely due to categories associated with a broader reopening of the economy such as used cars and trucks, and airfares fares which accounted for more than 50% of U.S CPI increase while there were fewer and fewer items rising by more than 2% in price. As noted by Morgan Stanley, the “transitory factors did a lot of the heavy lifting driving the May upside” and investors should watch out for more persistent components like rents that will set a firmer foundation for the inflation data as the transitory factors begin to fall out of the figures. Meanwhile, the G7 leaders kicked off a three-day summit in England. Market-moving pronouncements are unlikely but will involve discussions on global economic recovery from the pandemic, strengthening democracies and sustainability.

ECB Meeting

The European Central Bank renewed its pledge to keep asset purchases at a “significantly higher” pace compared to the start of the year even though the outlook on the euro-zone economy has improved. With more social and travel restrictions being lifted, the Eurozone consumer price inflation is likely to peak later this year which may translate to higher rates and tighten financing conditions if the bond-buying pace slows prematurely. With the renewed commitment, economists expect ECB to continue its bond purchases at roughly $19 billion euros a week before reducing its pace in September. The ECB’s emergency program is currently set to run through March 2022, and most economists do not expect it to be extended. Alongside the decision on crisis purchases, officials left interest rates, long-term loans to banks, and an older bond-buying program unchanged.

The FOMO Economy and ETF

Be it meme stocks, cryptocurrencies or options trading, you hear everyone making money except you. Feeling the fear of missing out (FOMO), you decide to get in on the action in hopes of quitting your 9 to 5 job. After a year of lockdowns and flushed with pent up savings, people are recklessly throwing their darts at the financial dartboard, hoping that at least one will hit the bullseye.

The current wave of FOMO has become so widespread to the extent that a new ETF was launched under the fund’s ticker symbol FOMO. According to the fund’s creator and Tuttle Capital CEO, Matthew Tuttle, the ETF aims to provide investors exposure to meme assets and other trending investments on social media, and “rebalances weekly so it can stay in harmony with market trends, and it weights holdings appropriately.” Only time will tell if FOMO makes a good investment, but for now it gets the prize as the best-named ETF.

Chart Of The Week

Important Information and Disclosure

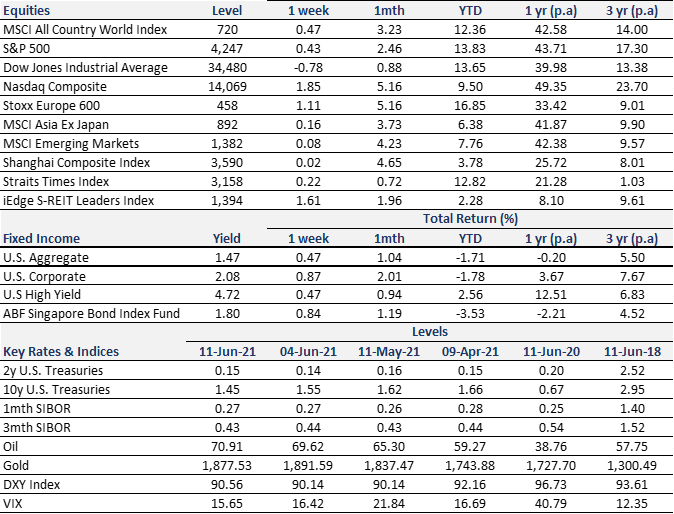

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.