Thought Of The Week

Jackson Hole Symposium, Powell Primed for Second Term

Federal Reserve Chair Jerome Powell said the central bank could begin reducing its monthly bond purchases this year although it will not be in a hurry to begin raising interest rates during the annual Jackson Hole symposium held between 26-28 August. Powell highlighted that tapering should not be interpreted as a direct sign for the timing of rate hike as that would be subjected to different conditions – 1) Maximum employment 2) Inflation has reached 2% and is on track to moderately exceed 2% for some time.

Since the messages was in line with market expectations with Powell sticking to the same script during its Fed meeting, investors took the news of the coming taper in their stride, avoiding any hint of the so-called 2013 “tantrum” when the Fed took markets by surprise when it unexpectedly announced the start to pare back asset purchases. The S&P 500 rose during the much-anticipated address to stand more than 0.6% higher while 10y Treasury yields nudged slightly lower to around 1.33%.

Meanwhile, Treasury Secretary Janet Yellen endorsed Powell for a second term as Fed Chair whose current term will end in February 2022. Her support offered an enormous boost to Powell’s chances given her credibility and reputation as a central banker for two decades. Other contenders include Lael Brainard who has the support of progressive Democrats. Wall Street is banking on another four years for Powell since it would lend continuity and reduce uncertainty about the path for monetary policy amid inflation and the delta variant risks. As the Fed chief in 2022 will have to lead the actual drafting for tightening instead of simply overseeing a pre-set course, any surprise pick may spur volatility in markets.

China’s Common Prosperity Over Profits

As China continues to push for “common prosperity” and encourages those who get rich first to help those left behind in order to close the country’s wealth gap, Chinese officials have also clarified that this is aimed at creating a bigger consumption market instead of “killing the rich to help the poor” on Thursday. However, investors believe that these reforms aimed at reducing cost-of-living pressures may come at the expense of profitability since businesses will need to revisit their strategies such as premiumization that ride on China’s growing income. In addition, the unspoken rule of charity giving to comply with Xi Jinping’s idea of “social hand” have seen high-profile companies and wealthy celebrities making major philanthropic donations where total amounts have soared to a record $5 billion this year.

It is likely that regulatory fog will continue to cast a shadow over Chinese equities especially for ‘new economy’ industries in the short-term as investors await clearer policy signals from the Chinese government. Overall, there is a lot for Xi to account if he wants to stay for a third term (which is unprecedented in recent history) when the Chinese Communist Party (CCP) hold its 20th National Party Congress in October 2022. Otherwise, he could face the threat of dismissal by internal CCP factions and his political power neutered.

Chart Of The Week

Important Information and Disclosure

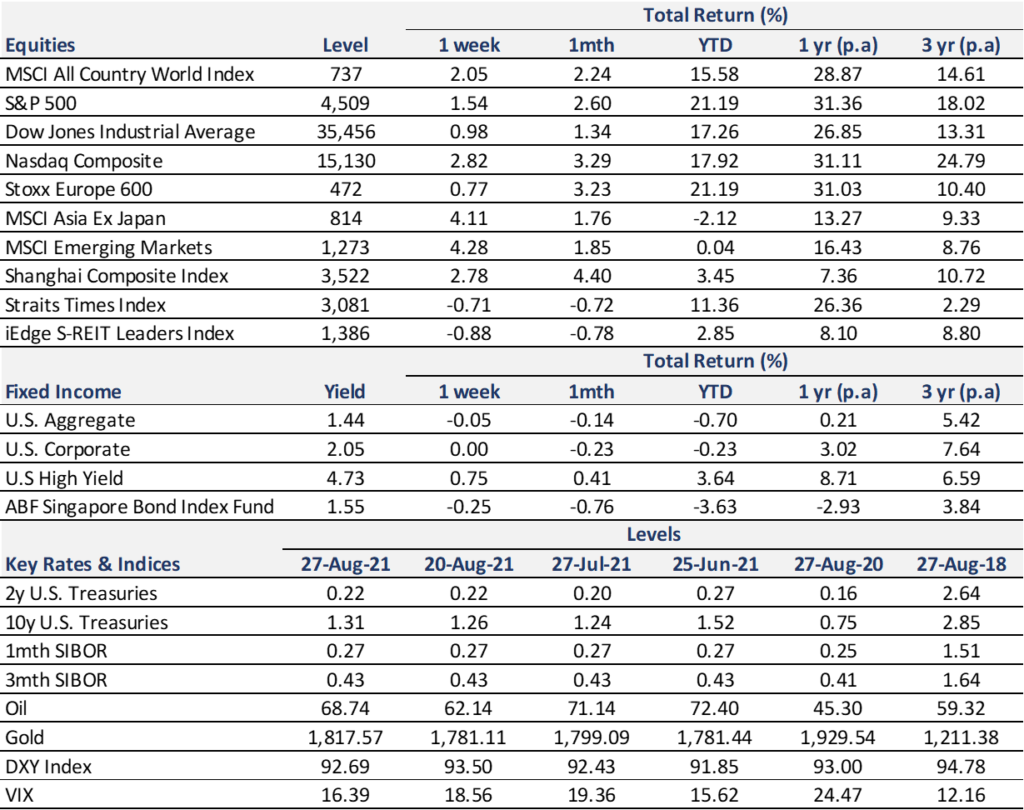

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.