Thought Of The Week

Fed Meeting Minutes, Treasuries Outlook

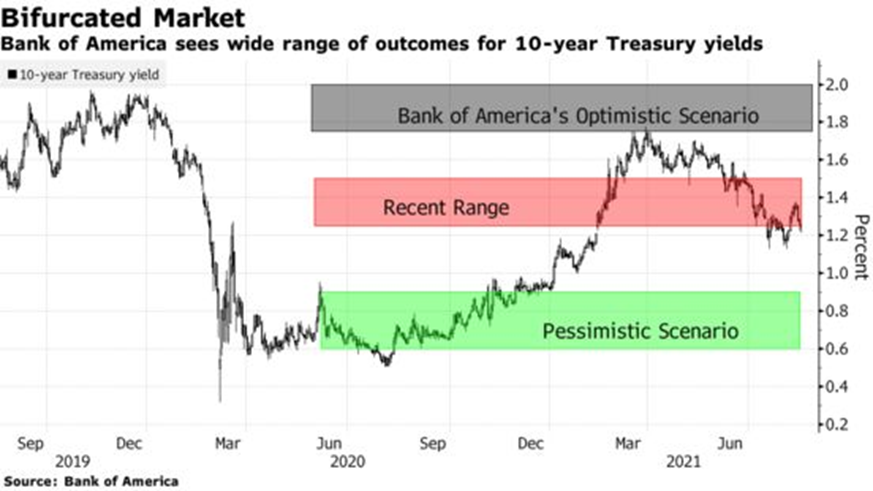

Inflation has risen faster than expected for the past months, but unemployment remains stubbornly high. This puts the Fed’s two jobs—keeping prices stable and maximizing employment—somewhat in conflict. Increasing interest rates to ward off inflation may hinder economic growth, while keeping rates low for too long may risk higher inflation. Minutes from the 27-28 July FOMC meeting have proven the difficulty to navigate this middle path and the FOMC members were not in complete agreement either. While most of the representatives believe that it “could be appropriate to start reducing the pace of asset purchases this year,” others preferred early next year to avoid sending wrong signals to the market. Furthermore, it is also evident that the Delta variant has become another layer of concern for the Fed officials as it was mentioned 6 times in the recent minutes compared to none previously. Given the fluidity on the virus situation, it is not surprising that even Bank of America strategists are forecasting a wide range of outcomes for 10y Treasury yields, either sliding below 1% or surging as high as 2% by the end of the year, indicating how low conviction in the market has gotten.

Hong Kong Enters Technical Bear Market

Asian markets have been hammered this week by China’s regulatory crackdown including tougher rules on the usage of customer data. The Hang Seng Index fell more than 20% from its February peak, entering a technical bear market. The biggest drags on the index include Alibaba, Tencent and Meituan (ATM). While Tencent reported its Q2 earnings that were roughly in line with estimates this week, it was interesting to note that it will be giving another 50 billion yuan, on top of its April pledge of 50 billion yuan, to aid the government’s wealth redistribution efforts to achieve “common prosperity.” The company also stressed its commitment to help small and medium-sized firms grow and curb gaming addiction among minors, an obvious attempt to please the local government. With more regulatory challenges suppressing valuations and elevating risk premiums in the short-term, investors will need to brace themselves for some volatility before the China’s government restores confidence in the stock market.

A Tale of 2 Chinese Issuers

Despite a record 103 billion yuan loss last year, distressed China state-owned asset manager, Huarong said that it would not be restructuring its debt after receiving bail-out from a group of state-owned investors, including Citic Group and China Insurance Investment. This is a sharp contrast to real estate developer China Evergrande, an equally big borrower, who was recently rebuked by regulators to address its debt woes. Analysts were mixed on whether the regulatory statement signifies Beijing’s willingness to provide financial support via state-owned banks and investors. While some see the developer as too big to fail, market hopes for a government bailout have been fading in recent weeks. At best, the regulator’s comments have helped to signal the developer’s intention and buy some time to divest its assets.

Chart Of The Week

Important Information and Disclosure

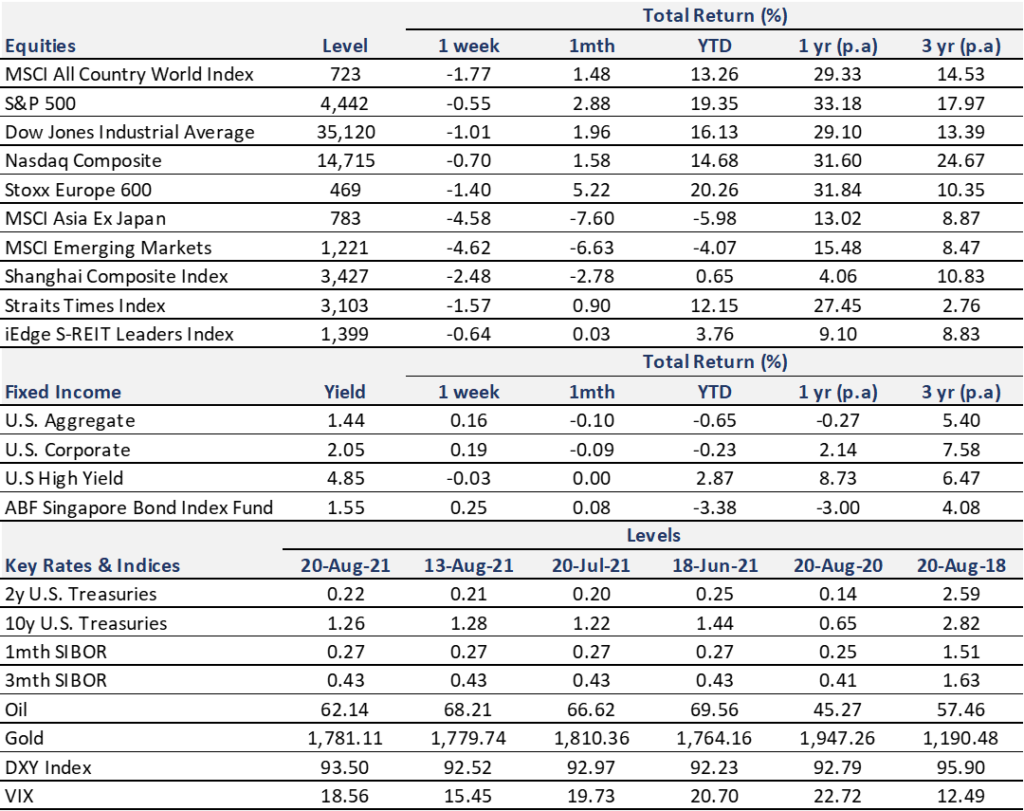

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.